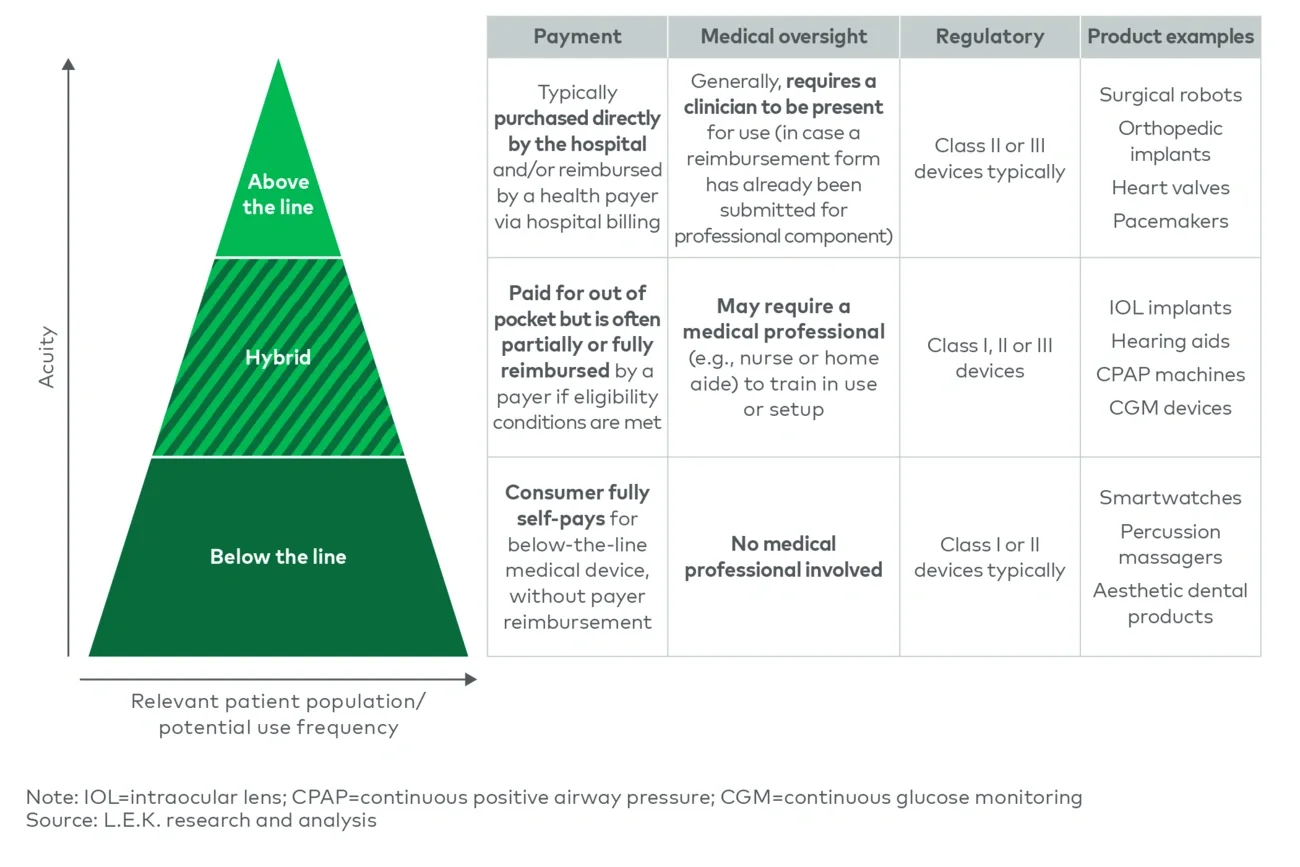

Medical devices that are a better fit for the above-the-line model are typically more complex, are well covered by insurance and require in-person clinician involvement (due to potential for major adverse events or complications). Examples of such devices are pacemakers and orthopedic implants. For these types of products, shifting to a below-the-line model is obviously a nonstarter; physicians are highly involved in product selection, as they are responsible for making sure a procedure is successful. A patient’s influence on a provider’s choice of pacemaker or knee implant is therefore more limited (and appropriately so).

However, there is a broad spectrum of medical devices that are ripe for a below-the-line strategy. They are typically used primarily outside the hospital, require less clinical know-how, involve patient preferences (e.g., comfort and aesthetics) and do not carry major risks of adverse events or complications. In these instances, clinicians shift from key purchasers and decision-makers to influencers helping patients find the best device fit. For instance, patient monitoring and telehealth-enabled products can often be used outside clinical settings and can be incorporated into a patient’s daily life (e.g., smartwatch to capture electrocardiograms and monitor blood oxygen levels) to help them better manage their own health.

Clinicians can help patients understand the benefits and trade-offs of these devices, rather than making the decision and device selection for the patient. Another example of a product that has found success with a below-the-line strategy is Softwave Tissue Regeneration Technologies’ shock wave device, which is used to reduce pain and accelerate healing of musculoskeletal and wound injuries. After years of payer negotiations and clinical evidence generation efforts, the company found more rapid, greater commercial success in bypassing reimbursement altogether and selling directly to self-pay-driven care settings (e.g., chiropractors).

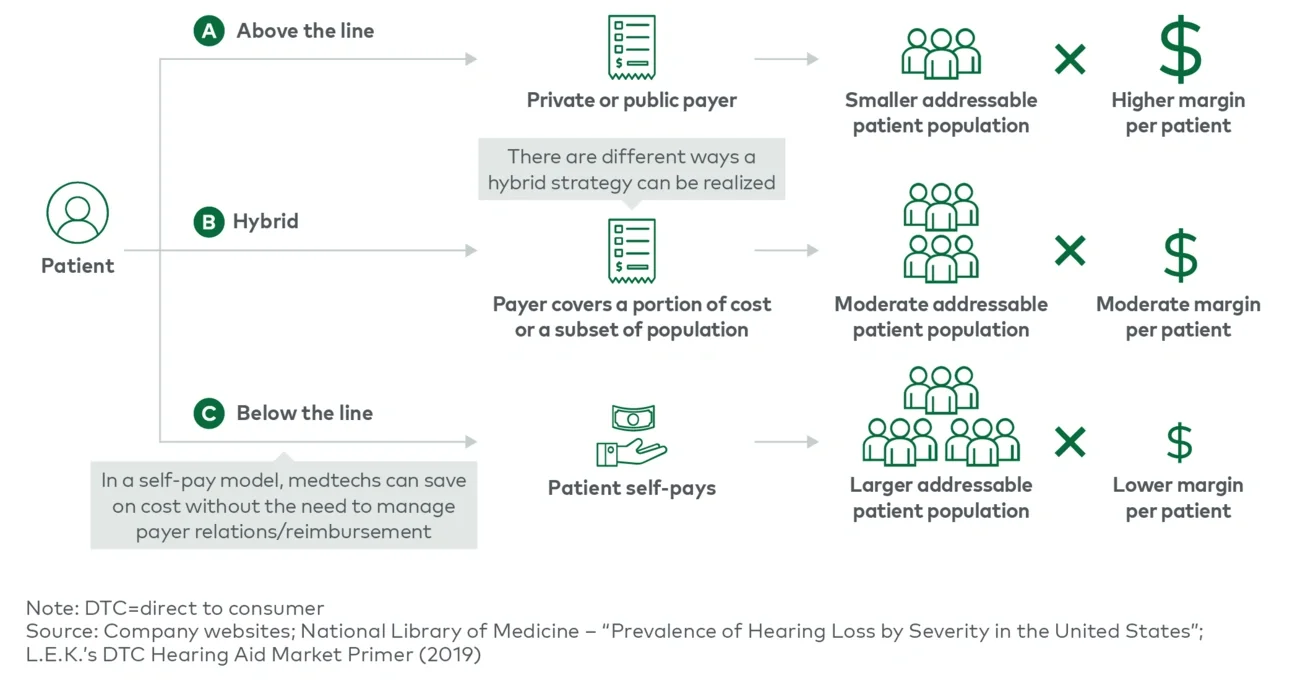

The hybrid model also provides intriguing possibilities and can be approached in a variety of different ways. Medtechs can design the reimbursement strategy so that payers either cover a subset of the market (e.g., hearing aids, sleep apnea equipment) or partially reimburse devices (e.g., intraocular lens implants (IOLs)).

The hearing aid market provides an example of a patient being able to buy a medical device directly if not reimbursed. The market can be segmented into two distinct categories based on severity of the need. Patients with severe hearing loss will require a prescription device and need to work with a hearing specialist or audiologist to prove the device’s necessity and properly fit the device. Some insurers cover or partially cover these devices if proper documentation illustrating the need for the device is shown. Alternatively, a patient with mild-to-moderate hearing loss is unlikely to have the device covered by insurance but can purchase more affordable over-the-counter hearing aids and also avoid the cost of clinician visits (e.g., prescription generation, equipment fitting).

Sleep apnea and continuous positive airway pressure (CPAP) equipment provides another example of a hybrid strategy. While payers typically cover the CPAP machine itself as well as base equipment (mask, tubes, etc.) if a need is proven, a patient who prefers a higher-quality mask or prefers to change the associated tubes more frequently can pay out of pocket. In addition, many patients do not want to jump over the hurdles of proving they need a CPAP machine and, as a result, purchase one directly without reimbursement.

Medtechs can also pursue a partial reimbursement strategy with payers to achieve a hybrid business model. Premium IOLs used to treat cataracts provide an example of this strategy. While a base IOL is typically covered by payers, premium IOLs that not only correct cataracts but also improve vision for near- or farsighted patients, replacing the need for glasses or contacts, typically are not covered as they are vision improving rather than correcting. However, payers will cover the cost of the base IOL, allowing a patient who elects to use a premium IOL to pay only the difference in price rather than the full amount. This reduces the burden on the patient when selecting a premium lens and grows the overall market size.

As the hybrid model continues to gain traction, new ways of pursuing a hybrid business model are likely to continue to arise.

Why are below-the-line and hybrid business models becoming more relevant?

Five critical healthcare macrotrends are helping drive the increasing relevance of below-the-line business models in medtech:

-

Higher patient engagement in healthcare is leading to a greater likelihood of patients being involved in key care decisions, and as a result, patients are now more involved in choosing and paying for their own medical products that they believe best facilitate their health.

-

Increasing prevalence of high-deductible plans is shifting the cost of care to patients, increasing the amount of self-payment, and encouraging more proactive decision-making to reduce downstream costs.

-

A generational shift in patient demographics is increasing the share of patients who are more willing to use alternative payment models and are decreasing their reliance on healthcare plan recommendations and payment models. Patients are also increasingly frustrated with the limitations of the current healthcare system and the difficulty of qualifying for reimbursement, which is leading to increased willingness to search out self-funded care alternatives.

-

Key technology advances in device miniaturization, the democratization of digital and the proliferation of smartphones are creating the requisite infrastructure to bring affordable yet relatively complex devices to market.

-

Growing availability of and access to information online coupled with increasing healthcare transparency better enable patients to shop around for treatment and medical product alternatives, giving them agency over their own healthcare like never before.

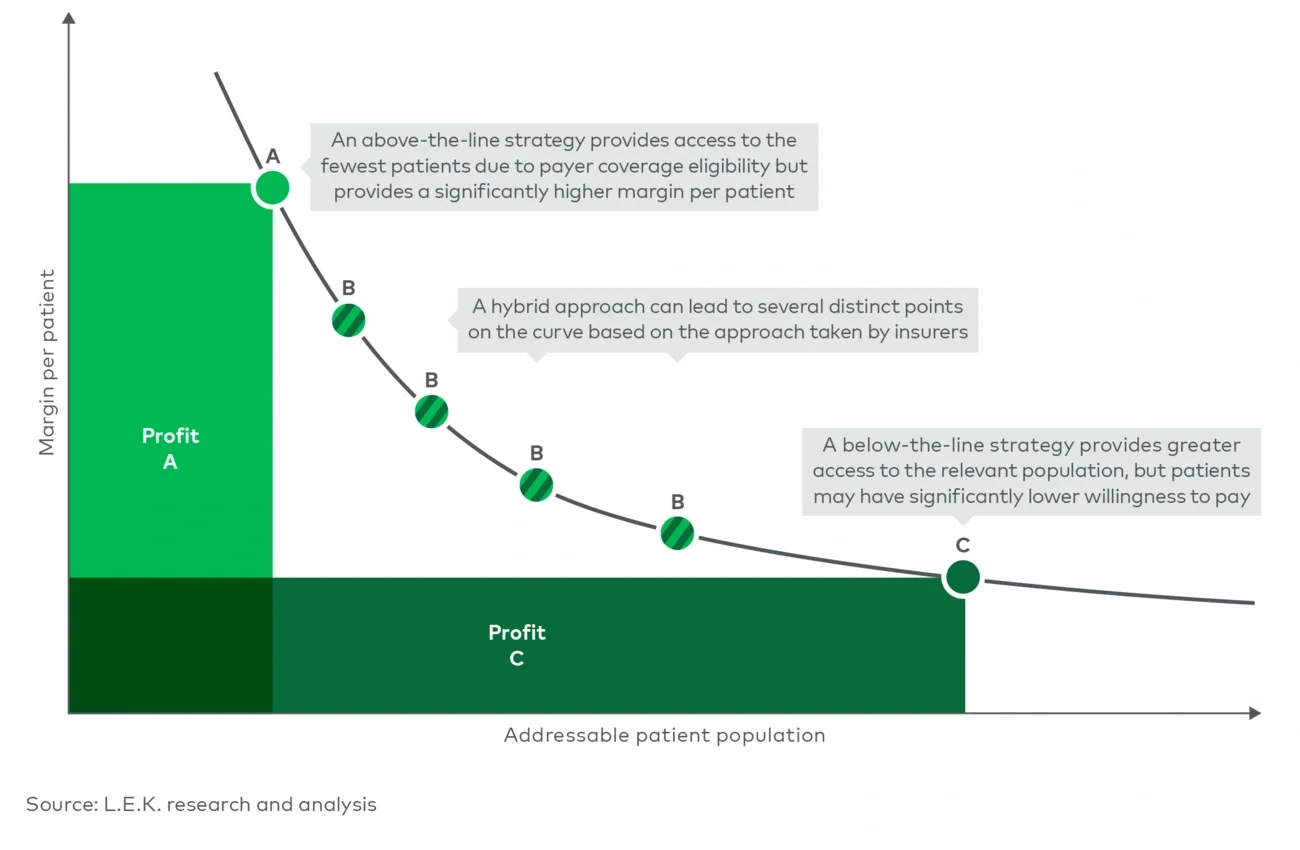

How do below-the-line/hybrid business models impact profitability?

In contrast to the traditional above-the-line business model where medtechs target a smaller addressable patient population with a high profit margin, below-the-line models can potentially lead to higher profit if the volume gain can offset the smaller margin per patient (see Figure 3).