The trend of providing a more complete partnership for care is upping the investment ante for medtech OEMs and stimulating the evolution of the market beyond traditional growth paradigms. The ability to grow is no longer as simple as providing the next iteration of a prior device that marginally improves care. As a result, to compete in therapeutic areas, medtech OEMs are requiring considerably more financial investment than previously needed.

To maintain growth and their competitive advantage, medtechs must look to build a comprehensive therapeutic portfolio through both significant internal organic development and external inorganic investment. As a result of the shifting growth dynamics, the medtech market is expected to be positively impacted through greater dynamism and innovation.

Inorganic, or external, activity is critical to building a complete ecosystem and typically requires significantly more capital than traditional research and development do. Given the evolving needs in medtech, inorganic activity has increased in recent years and is expected to continue to increase in 2023. A number of healthcare macrotrends are providing tailwinds to inorganic activity as they require medtechs to develop capabilities they did not previously need. These macrotrends include the rise of digital, the emergence of alternative care sites with unique needs, increased patient involvement in healthcare decision making, and evolving risk-based models.

Each of these trends requires a shift in the way medtech players currently do business, leading to the need to acquire additional capabilities (digital application design and integration, data security, etc.) outside their current core competencies to unlock additional growth opportunities.

2. Refining focus to prioritize growth segments for shareholder value, allowing medtech manufacturers to reinvigorate and drive innovation

As a result of the increasing requirement for capital advancement, medtech OEMs must focus their efforts on high-growth segments. These segments will differ based on the infrastructure, products and R&D for each player. The need to focus on high-growth segments stems from shareholder and investment needs. Medtech competitors require an influx of cash to fund R&D activities, inorganic investments and business development to maintain and improve their positioning. Historically, medtechs have spent approximately 6% to 12% of total revenue on R&D. The high-capital requirement for growth means that medtech OEMs must deliver attractive returns to continue receiving future investments. To do this, medtechs are striving to increase their overall compound annual growth rates (weighted across their business units) and demonstrate that they can provide a strong return for shareholders.

Medtronic’s decision to spin off its patient monitoring and respiratory interventions business provides a critical example of focusing on growth segments. The spinoff was announced as part of its strategic vision of achieving a 5% organic growth rate (weighted across its business units). To achieve this goal, Medtronic is taking a two-pronged approach and looking to not only expand organic growth in high-growth segments but carefully divest portions of its mature, sleepy business segments to free up capital to continue to drive innovation. This then creates a flywheel with the proceeds and funds that would have been invested in the divested business reinvested in high-growth strategic priorities and often more-innovative business units.

Zimmer Biomet also believed that its dental and spine business units could achieve higher growth under separate leadership and spun the two business units off into ZimVie. Growth in these two business units had stagnated and slowed, requiring a different approach. While Zimmer Biomet’s ROSA robotic platform has demonstrated success for knee and hip implants, its adoption for spine procedures remained low. Separation from this system mandated by a spinoff into ZimVie facilitates the development of a distinct approach to restimulate growth in the spine market and generate strong returns for shareholders.

Similarly, in 2022, Becton Dickinson approved a spinoff of its diabetes care business as part of a larger growth strategy plan, helping sharpen its focus on its core innovation priorities. The separation is expected to be beneficial for Embecta (the diabetes care business) as well, in attracting greater capital investments, recruiting talent and ensuring resources are allocated to its own product pipeline. The spinoff is expected to drive long-term value for shareholders, but it also ultimately benefits global diabetes patients by ensuring continued investment and focus on diabetes care.

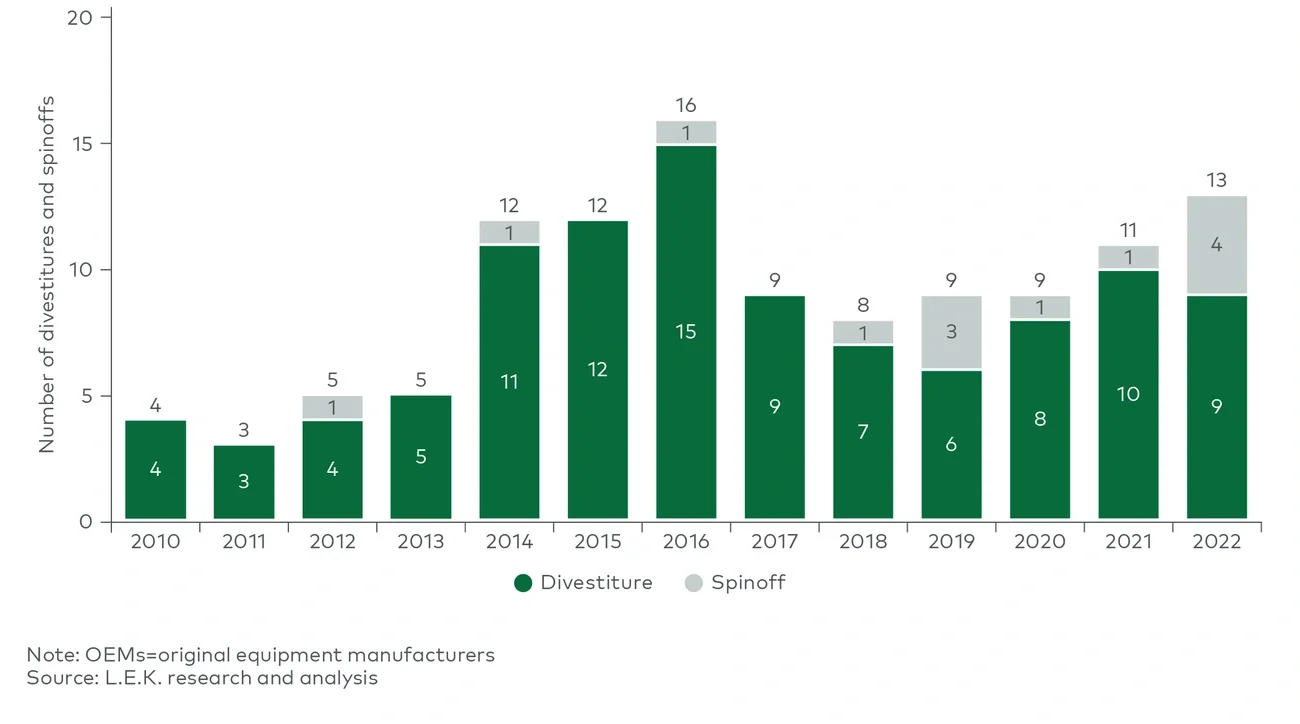

Furthermore, after a period of significant industry consolidation in the 2010s, M&A activity has slowed in recent years. The medtech M&A deal count declined from nearly 300 deals in 2010 to fewer than 100 deals in 2022. During the early 2010s, medtechs focused on revenue growth and economies of scale, but they are now shifting to prioritize profitability — a dynamic that is likely to continue to have a natural pendulum swing.

Since the start of the past decade, low interest rates have driven record-high valuations, resulting in a trend toward larger and fewer M&A transactions. Recently, deteriorating capital markets and rising interest rates have slowed M&A activity further, as buyers and sellers struggle to agree on a fair value. As a result of shifting priorities and macroenvironmental change, divestitures and spinoffs have increasingly gained traction as effective tools for medtechs to refocus on select high-profitability business units and transition out of business units that are not receiving the attention they need to succeed.

The recessionary external stimuli stemming from the COVID-19 pandemic provide tailwinds to divestitures and spinoffs

COVID-19 has also served to accelerate many trends and changes in healthcare, increasing the pressure on medtechs as a result of reductions in related procedures. COVID-19 has contributed to this reduction on multiple fronts: Hospital staffing shortages limited, and continue to limit, the number of procedures feasible; some patients remain hesitant to seek medical aid, particularly for elective procedures; and shifts in the paradigm of care — with a greater focus on preventive care and less-invasive procedures — are reducing the need for complex medical devices. These pressures have led to one of the most, if not the most, challenging quarters in medtech history, during Q3 2022, with many device makers facing declining revenue or, at best, low-single-digit growth.

COVID-19 and the headwinds it has presented have further illustrated to investors and OEM leadership the need for strategic divestiture in medtech. Fighting a battle on multiple fronts can lead to overextended resources without sufficient capital to maintain a strong market position or further it. As many of the trends accelerated by COVID-19 are expected to have a lasting impact in driving innovation and growth in the market (e.g., greater patient engagement, increased digitalization), divestitures will continue to remain a vital part of medtech strategy to meet growth trajectories, continue to drive innovation and appease stakeholders.

What does this mean moving forward?

The medtech industry, without a doubt, is changing. However, most of the changes are expected to positively impact the market over the long term and push medtech OEMs to seek out innovative ways to meet changing needs and drive growth. The investment necessary to steadily grow is accelerating as the complexity of technology increases exponentially and the role medtechs play evolves to a more complete partnership in the healthcare ecosystem.

Medtechs will need to identify and prioritize key areas of growth and effectively allocate capital to achieve growth objectives and deliver strong returns for their shareholders. This will require medtechs to divest sleepy assets that require greater attention and increasingly demand that they leverage spinoffs, as the number of buyers who can justify paying a premium for a complex medical device business unit decreases due to large medtechs streamlining their businesses to refine focus and encourage growth.

As the industry moves forward, there are likely to be multiple implications of these trends. First, medtechs should not shy away from strategic divestiture, including spinoffs that represent an opportunity for them to optimize their capital allocations and continue to drive growth. The evolving environment is mandating the need for change and increasing the requirements to sustain strong organic growth.

As medtechs divest, new players will continue to emerge with a focus on a specific disease ecosystem, increasing the need for the larger players to refine their assets and focus their investments. As medtech companies navigate this trend, the entire medical technology market is expected to positively benefit from more effective capital allocation, stronger returns for shareholders and increased innovation in emerging and high-growth areas.

The authors would like to thank Jenny Mackey, Chris Sparacino and the L.E.K. Healthcare Insights Center for their important contribution to this report.

For more information, please contact healthcare@lekinsights.com.