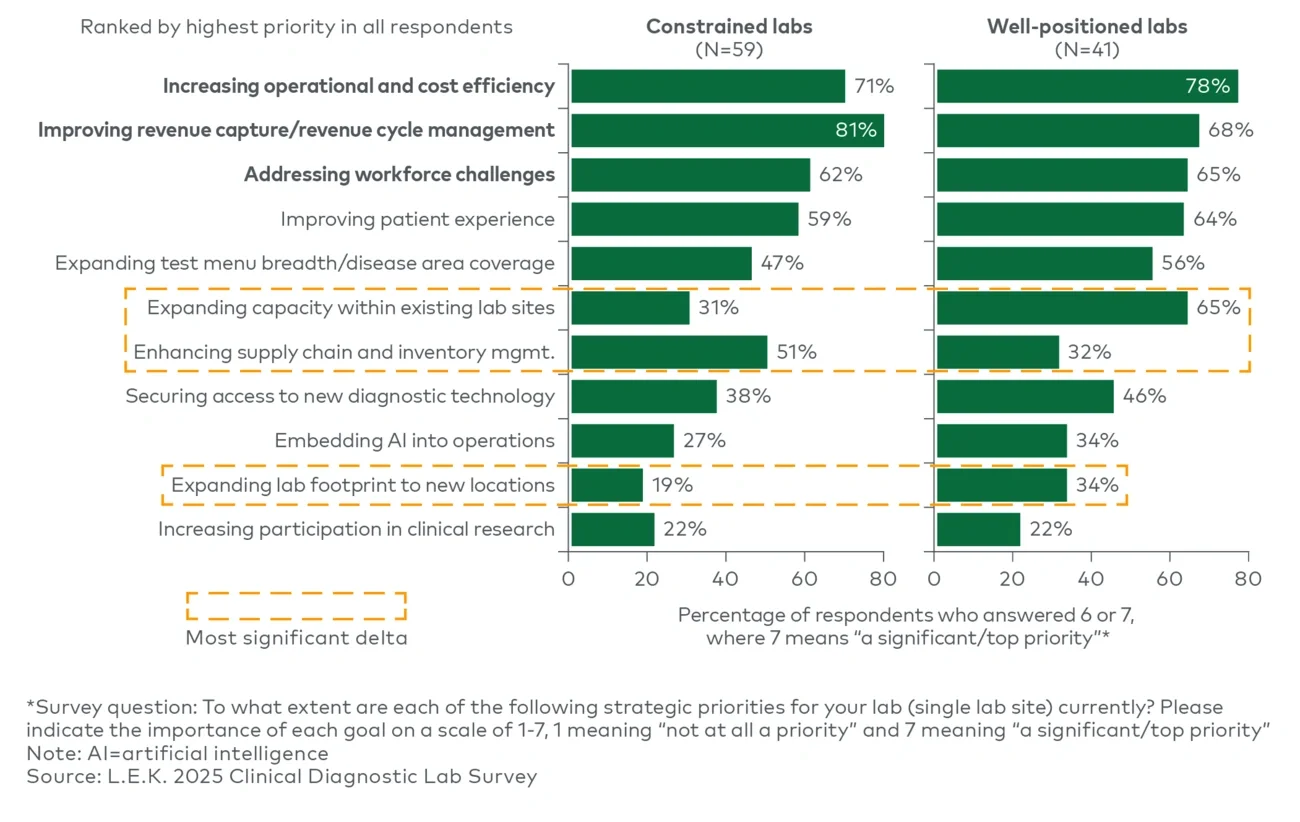

Where priorities diverge are in second-tier actions that signal the ability to invest versus the need to defend. Financially strong labs place materially greater emphasis on expanding capacity and lab footprint as well as securing access to new diagnostic technology, reflecting a posture that extends beyond stabilization into selective growth and modernization. In contrast, constrained labs place materially higher emphasis on supply chain and inventory management (51% vs. 32%), consistent with limited tolerance for shortages, price volatility and backorders that can disrupt service and revenue capture.

Although embedding artificial intelligence (AI) into operations ranks lower among stated strategic priorities, many labs are already deploying it selectively to drive efficiency. About 60% of surveyed labs report at least trialing AI in selected workflows, led by reference labs (approximately 70%) and large community hospitals (roughly 65%), followed by AMCs (about 55%) and small community hospitals (around 45%). AI adoption today is concentrated in analytical workflows/ test interpretation and result reporting and delivery.

Looking ahead, roughly 90% of experts expect broader AI use within three years, with expanding applications including quality control and specimen triage and prioritization. Wider adoption of AI will depend on demonstrating clear operational return on investment (ROI) and directly supporting top lab strategic priorities, particularly efficiency gains and revenue capture.

Notably, the survey also indicates that strategic priorities are broadly consistent across lab settings and lab sizes, underscoring that the emphasis on productivity and efficiency is consistent across labs in AMCs, community hospitals and reference environments.

Implications for in vitro diagnostics manufacturers: How to win in a bifurcated market

As purchasing decisions place greater emphasis on demonstrated ROI and ease of execution, suppliers will increasingly need to meet labs where they are — recognizing that a one-size-fits-all value proposition will not resonate equally with financially strong and financially constrained labs.

The following implications summarize how OEMs and lab suppliers can win in this environment:

- Tailor the value proposition by financial posture. Financially strong labs are more likely to prioritize modernization and selective growth, whereas constrained labs will be more focused on near-term stabilization and resilience; suppliers should segment messaging, offerings and commercial approaches accordingly.

- Lead with quantified operational and economic outcomes. Labs’ “table stakes” increasingly emphasize demonstrable impact over general claims — suppliers should translate solutions (including end-to-end automations) into measurable improvements in key lab outcomes (e.g., throughput, turnaround time, utilization, first-pass yield, labor productivity, revenue capture/denials) and articulate the economic value clearly.

- Reduce adoption friction through execution support. Given staffing constraints and limited tolerance for disruption, implementation capabilities (workflow design, training, information technology/connectivity, change management, service models with guaranteed uptime, remote monitoring) increasingly influence purchase decisions alongside product performance.

Conclusion

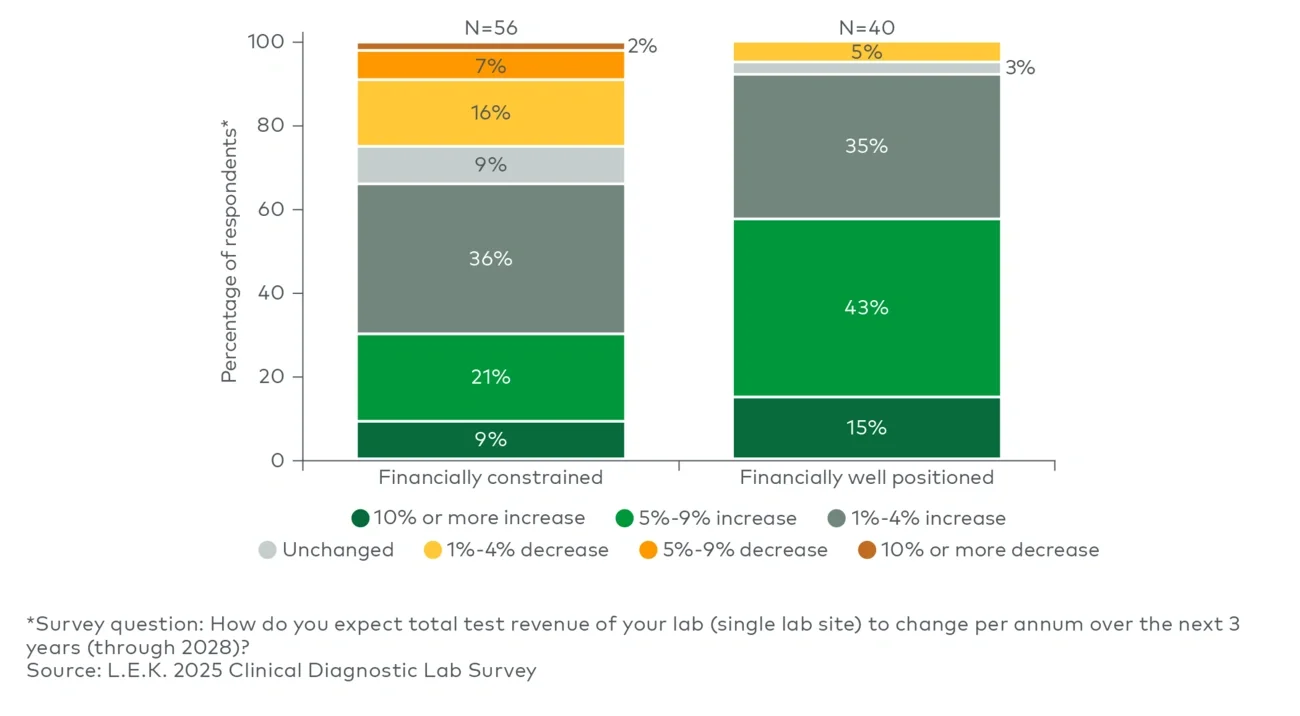

Our 2025 Clinical Diagnostic Lab Survey depicts a sector increasingly split between labs that can invest selectively and those operating under meaningful constraint. Most labs expect revenue growth through 2028, but stronger labs anticipate faster growth, potentially reinforcing divergence. For OEMs and suppliers, success will depend on tailoring value propositions to distinct customer realities, delivering quantified operational and financial outcomes, and providing robust execution support.

In an upcoming edition of Executive Insights, we will explore how test demand is growing across key modalities, how labs are adopting emerging technology platforms including next-generation sequencing and digital pathology, and more.

To discuss these findings and how your organization can position itself for success in this evolving environment, please contact us.

Note: AI was used to support the drafting of this article.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC