Market challenges and changes such as these point to opportunities for medtech companies to reimagine themselves and suggest several guiding principles for navigating a post-COVID-19 world.

Successful medtechs are using the confluence of events for “rediscovery,” with guiding principles that range from recalibrating customer models to reimagining their business potential, from defining and harnessing digital opportunities to embracing organizational change.

The principles underscore a number of key medtech priorities for 2023, including the following:

-

Know your customers well: Maintain a heightened, segmented perspective within the context of broader, continued health system/provider evolution; in other words, empathize with and thoroughly understand provider challenges

-

Drive (or ride) the digital innovation wave: Medtech companies have to adapt to the prevalence of connected devices, digital ecosystems, commercial and supply chain tools, organizational shifts for digital capability, and the coexistence/cohesion of these innovations

-

Modernize: Pragmatically leverage services and solutions to effectively meet customer needs

-

Improve working capital management: Develop and manage the supply chain/supplier network to ensure resilience

-

Reinvigorate commercial transformation: Attend to large accounts, priority accounts, enterprise/system-level selling, ambulatory surgery centers (ASCs), digital and omnichannel engagement, pricing models, expanded clinical support, and virtual training/education for employees

-

Embrace technology and how it will change both your customers and competitors: Technologies that include advanced visualization, robotic surgery, digital, neurostimulation, interventional and single-use devices/solutions/innovations

-

Focus on corporate development: Ensure a comprehensive alignment of digital service delivery, full continuum, adjacencies, fallen angels and carve-outs

-

Continue to increase leverage of outsourced partners: Maximize use of Chief Medical Officers, regulatory affairs (RA) / quality assurance (QA) and supply chain

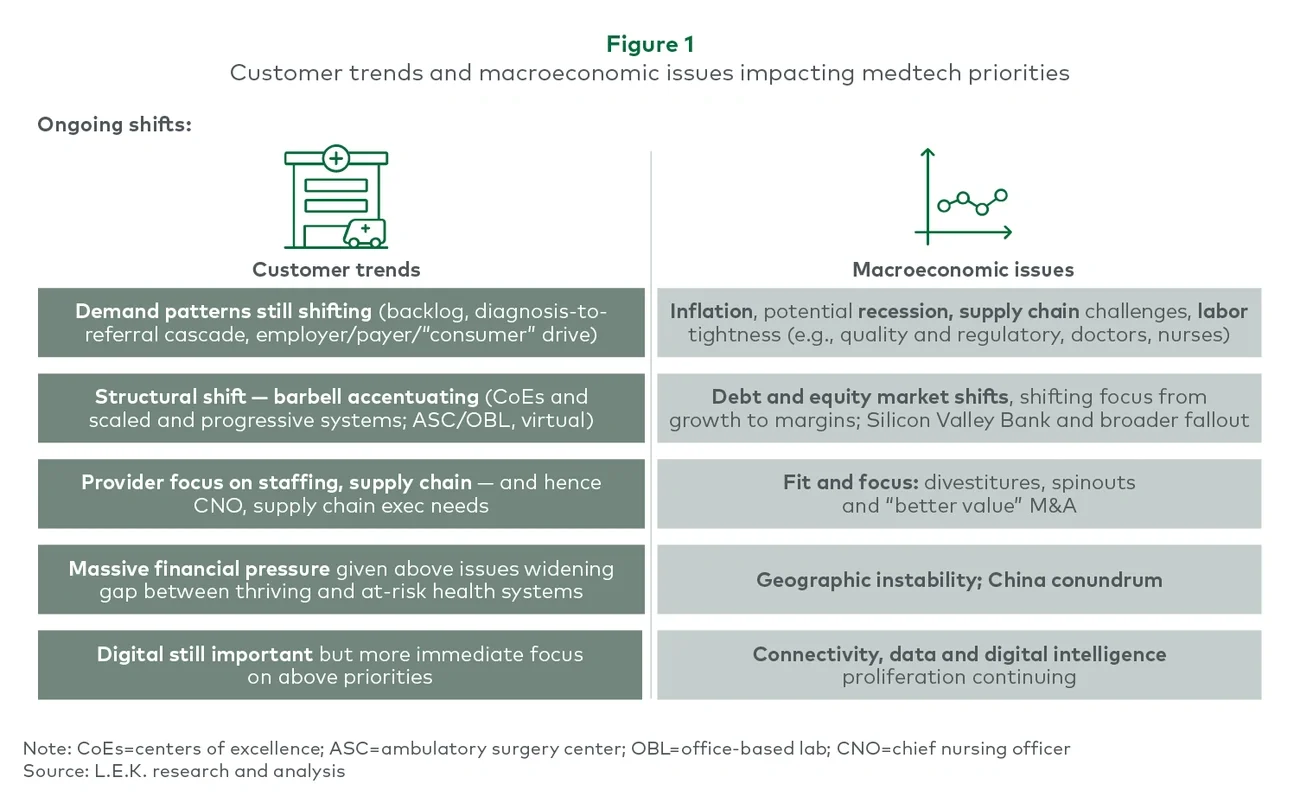

Macro context and implications

There are a host of healthcare provider challenges and a period of evolution that must be considered in the context of medtechs’ rediscovery.

Hospitals are struggling financially as profitable procedures are shifting to outpatient settings and the hospitals are left to manage an extremely broad set of unpredictable, high-acuity and high-cost procedures.

Increasingly, medtech companies must continue to demonstrate the value of their products and services to their customers, particularly at a time when customers have intensified their focus on containing budgets.

L.E.K.’s proprietary Provider Pulse tool reveals that scaled progressive health systems tend to be thriving, taking an increasing market share from more traditional health systems. This highlights a need for medtechs to develop a comprehensive understanding of their customer base and to adapt commercial engagement models and offerings to meet the varying needs of the provider segments within each category.

Health systems are already feeling the effects of procedures shifting out of hospitals to ASCs and further anticipate that more therapeutic areas (TAs) will follow that shift as more disruptive technologies develop and recent novel procedures prove safe enough for outpatient settings.

Health systems have also put a renewed emphasis on supply chain evolution, providing opportunities for medtechs to assist in the transition from cost center in the health system landscape to strategic enabler.

Labor shortages and tightness in staffing resources throughout the healthcare system have created another area that’s ripe for medtech opportunity. With the advancement of products and services that increase efficiency and automation within health systems, medtechs stand to capture more value than those that do not capitalize on the opportunity to increase efficiency.

Enduring macro challenges

Medtech companies increasingly find themselves operating in a more turbulent market, with the confluence of the release of monthly inflation data, annual reimbursement adjustments that lag chronologically (and are insufficient in absolute terms), and wage pressures — all of which negatively affect health system margins.

With U.S. interest rates expected to remain elevated for some time and deal volume and size in question, medtechs appear to be turning to alternative resources (e.g., cash) to finance investments. With over $100 billion on hand at the top 30 medtech original equipment manufacturers (OEMs), there could be more all-cash deals on the horizon for those with healthy balance sheets.

Market context for the medtech industry

M&A activity and themes

Some large medtechs are leveraging significant levels of cash on hand to facilitate acquisitions (e.g., Johnson & Johnson/Abiomed for about $16.6 billion cash, Thermo Fisher/The Binding Site Group for approximately $2.6 billion cash, BD/Parata Systems for roughly $1.5 billion cash). Meanwhile, acquisitions are becoming broader, including capability expansions, site of care extensions or both (e.g., Stryker/Vocera for around $3.1 billion, Medtronic/Cathworks promotion with right to acquire for up to $585 million).

While some large medtechs are leveraging significant levels of cash on hand to selectively acquire targets, others are taking the opportunity to diligently prune and reposition their portfolios. Executives are looking closely at portfolios to maximize fit and focus on higher-growth businesses, shedding lower-growth and less strategic businesses where there is an active market of buyers for carve-outs, including private equity, as well as strategic buyers.

Device trends and high-growth segments

Novel technology and clinical innovation are still rewarded, while connectedness and demonstrated utility (e.g., clinical, economical, workflow-based) are increasingly important. High-growth categories (>5% annually) tend to be categories that are considered as innovative by market stakeholders, such as transcatheter in cardiovascular (e.g., structural heart, electrophysiology) and neuromodulation. Higher growth medtech segments have multiple subsegments where innovation is driving growth.

Select TAs driving innovation

-

Electrophysiology (e.g., pulse field ablation)

-

Structural heart procedures (e.g., mitral valve repair and replacement)

-

Neuromodulation (e.g., expanding indications, novel nerve locations, closed loops, better outcomes)

-

Robotics (e.g., new TAs, enabling technologies, fewer incisions via a single port)

-

Advanced visualization (e.g., portable ultrasound, intracardiac 3D ultrasound, image-enabled analytics)

Leveraging digital, data and connectivity demonstrates improved utility with device and data connectivity, workflow efficiency, and an increased ability to show ROI through data.

Emerging digital opportunities

COVID-19 accelerated the focus on digital health starting in 2020, and while macroeconomic uncertainty has led to a bumpy 2022-23, digital health will only continue to gain importance and grow. Hospital executives may emphasize other priorities (e.g., staffing) ahead of digital innovation, but they acknowledge that providers will need to leverage external partners on many emerging digital, tech-enabled solutions. According to L.E.K.’s annual hospital study, hospitals are looking to invest in core digital health initiatives that can address ongoing labor shortages and margin pressures.

Medtechs may consider investments in digital health to support goals such as defending the core business, driving disruptive growth into adjacent markets and expanding into whitespace opportunities. Key medtech players (e.g., Abbott, Medtronic, Boston Scientific, Biotronik) have made significant digital health investments intended to support all three business goals. As medtech players that provide digital solutions flourish, it is important for companies to pursue high-value-add digital health initiatives to remain differentiated and competitive.

Evolving organizational focus

As medtechs evolve their organizational focus and capabilities, they often look outside their “four walls” for deep expertise in nonstrategic pockets (in the eyes of the OEM) where there is a healthy and growing ecosystem of outsourced partners. Medtechs are increasingly leveraging outsourced partners for manufacturing where partners are willing to invest in capabilities that OEMs may not have strategic reason to invest in. Medtechs are also experiencing an increased demand for regulatory/RA/QA support, which may be backfilled by outsourced consultancies that maintain capabilities and expertise spanning such functions. Outsourcing partners often are able to provide deep expertise in these niche areas but also are able to amortize resources more fully and broadly across the medtech industry.

For more information, please contact our MedTech leadership team to walk you through a broader set of supporting materials and have a dialogue specific to your organization.

Authors:

- Monish Rajpal, Partner and Managing Director (New York)

- Jonas Funk, Partner and Managing Director (Chicago)

- Ilya Trakhtenberg, Partner and Managing Director (Chicago)

- Sheila Shah, Partner and Managing Director (Chicago)

- Ned Moffat, Engagement Manager (Chicago)

Contributors:

- Dayton Sheppard, Senior Consultant

- Jessica Wu, Consultant

- Andrew Herbst, Senior Associate Consultant

- Momoka Kitara, Senior Associate Consultant

- Liam McAlaine, Associate Consultant

- Geenie Choy, Senior Associate

- Amna Ahmed, Associate