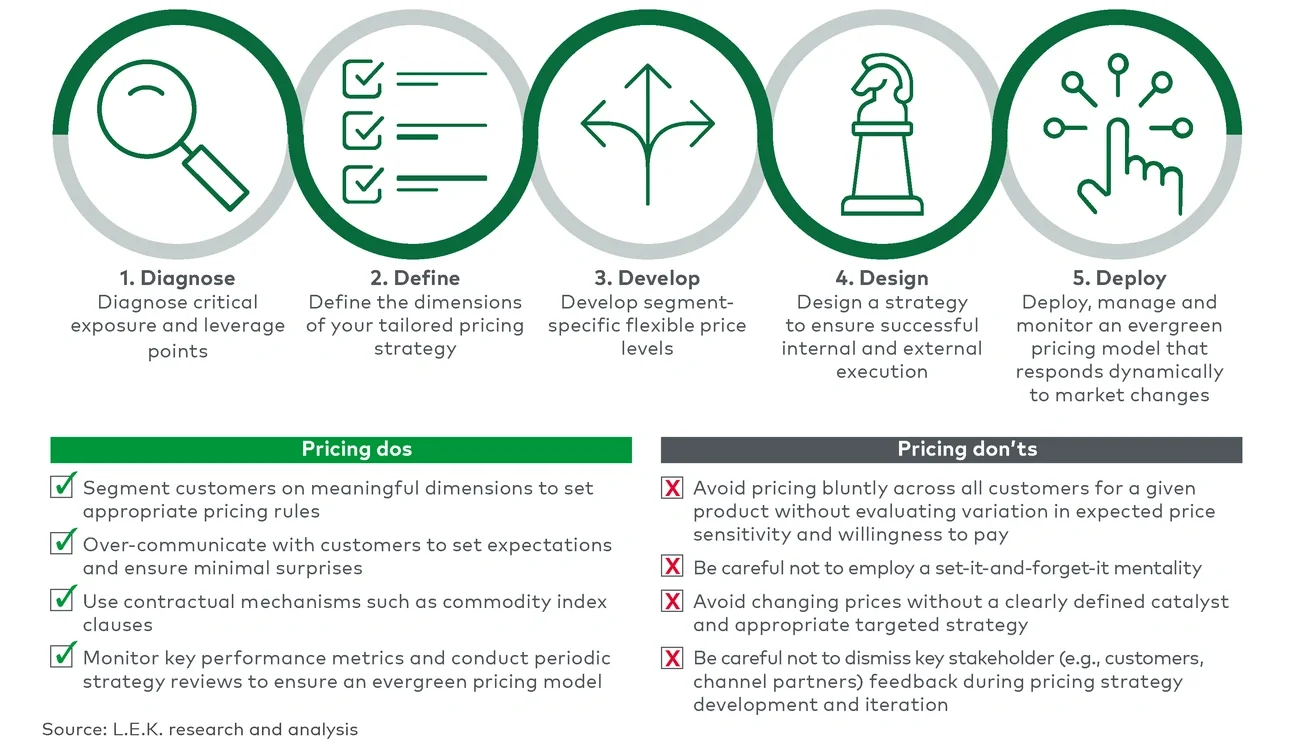

1. Diagnose critical exposure and leverage points

2. Define the dimensions of your tailored pricing strategy

A one-size-fits-all approach to pricing should optimally be avoided. As a result, medtechs need to define the dimensions that reflect customer behavior and the strength of the product value proposition. Potential dimensions include customer segment (e.g., institution type, degree of centralized purchasing), customer relationship strength (e.g., share of wallet, longevity of customer relationship), customer volume/scale, customer GPO affiliation, and product family or packaging type.

3. Develop segment-specific, flexible price levels

Medtechs should develop their pricing strategy through analysis of segment-specific customer pricing elasticity (e.g., by evaluating historical customer behaviors and/or customer surveys) across their portfolios. When determining price levels, reimbursement dynamics are critical to consider; globally, there is significant variation in reimbursement structures for medtech products. In the U.S., for example, coverage of medtech products is part of the procedure reimbursement code, whereas in much of Asia-Pacific, there is virtually no reimbursement for innovative medtech products, with the entirety of the cost borne by the patient. Consequently, it is important for medtechs to evaluate the economic impact of price changes not only on their business, but also on key stakeholders’ businesses (e.g., dealers, end customers) throughout the value chain to ensure the ecosystem is sustainable.

4. Design a strategy to ensure successful internal and external execution

Even with the most analytically rigorous, well-informed strategy, success is predicated on execution. Execution requires effective management of a range of internal and external stakeholders. Internally, medtechs can face barriers to pricing changes as front-line commercial teams often prioritize product sales to meet quotas, without commitment to pricing discipline, making it difficult to build momentum around better management of pricing.

Some medtechs already have effective governance processes in place, but many do not. Several dimensions of governance and organizational design can be important to address including sales team incentives (e.g., incorporating profitability), well-established decision rights and clear pricing alleys for different levels of sales team members. Externally, medtechs need to ensure that any pricing increases have a well-laid-out, proactive communication plan for both customers and any channel partners affected. Commercial teams need to be equipped with the right customer messaging that articulates the pricing changes and reiterates the value proposition offered (including findings from health economic outcomes research (HEOR)). Medtechs can also support their customers by incentivizing volume consolidation (e.g., securing commitments for higher share of wallet where it is achievable) and providing good/better/best product alternatives where relevant.

5. Deploy, manage and monitor an evergreen pricing model

Once deployed, pricing management should be evergreen, as opposed to a one-off event. Medtechs should actively monitor inflation, other macroeconomic factors and the competitive context (including penetration of private label and premium gaps between branded and private-label products), among other metrics. For many medtechs, pricing is not a strong “muscle” but a capability that may require (and merits) meaningful investment.

As medtechs continue to weather the challenges that come with inflationary, supply chain and global pressures impacting the industry, L.E.K. believes adherence to these best practices can inform a resilient, evergreen pricing strategy that puts them on firm footing for “normal” times as well.