Private healthcare in European markets continues to undergo significant expansion. Constrained public systems, long waiting lists and a rising appetite for better, faster access are pushing more patients to consider, and actively opt for, privately funded care.

L.E.K. Consulting’s recent multi-country survey of over 3,500 patients across five European markets confirms this trend, with demand growing not only for traditionally private-pay services like dental care, but also for more complex specialities such as cardiology, oncology and orthopaedics.

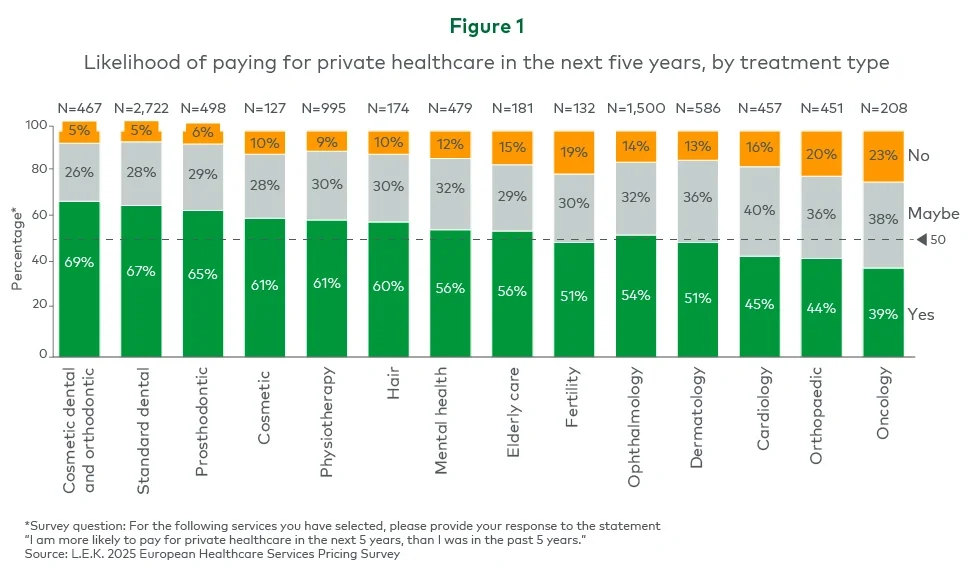

Patients are willing to pay, even for complex specialities

More than half of surveyed patients indicated a greater likelihood of paying for private healthcare in the next five years across 11 out of 14 treatment areas (see Figure 1). Notably, this includes complex and traditionally publicly funded specialities — such as cardiology (45%), orthopaedics (44%) and oncology (39%) — where willingness to pay has historically been lower.

This indicates a fundamental shift in patient expectations and behaviour. Where private care was once limited to non-essential or supplementary services, it’s now increasingly seen as a necessary route to access timely treatment, especially in systems under pressure.

The data shows this trend is most pronounced in Southern and Eastern Europe, where public infrastructure challenges are more acute and out-of-pocket models are already more normalised.