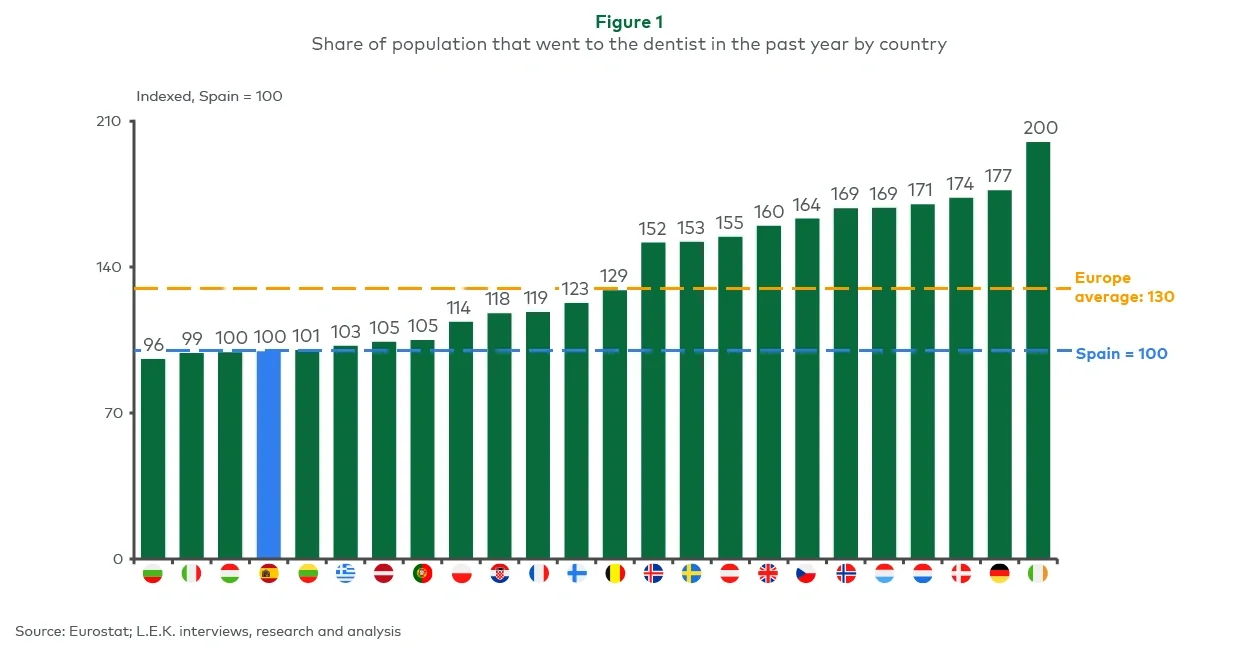

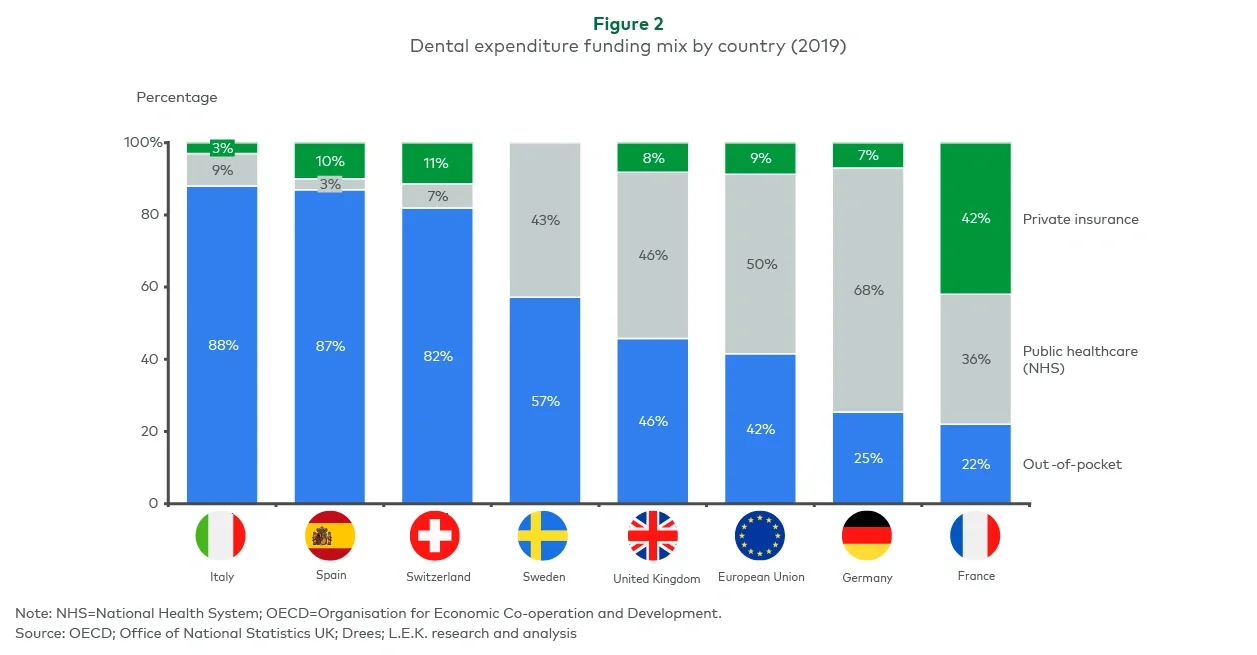

Spain has historically had a poor oral health culture, with only 50% of the population visiting the dentist once a year (lagging most European countries, see Figure 1) and only 45% of the adult population having 21 or more teeth (the minimum viable number to be able to eat properly). People have many reasons for not visiting the dentist, with ‘no perceived need’ being the main reason, followed by cost, whilst for the age 14-25 cohort cost is the main reason. This is not surprising given that only 2% of dental spend is financed by the National Health System (see Figure 2), in stark contrast to countries like Germany where c.65% is publicly financed and consequently the rate of dental visits is substantially higher at upwards of two visits per year.

Digital Transformation and the Advent of the Dental Laboratory Chain in Spain

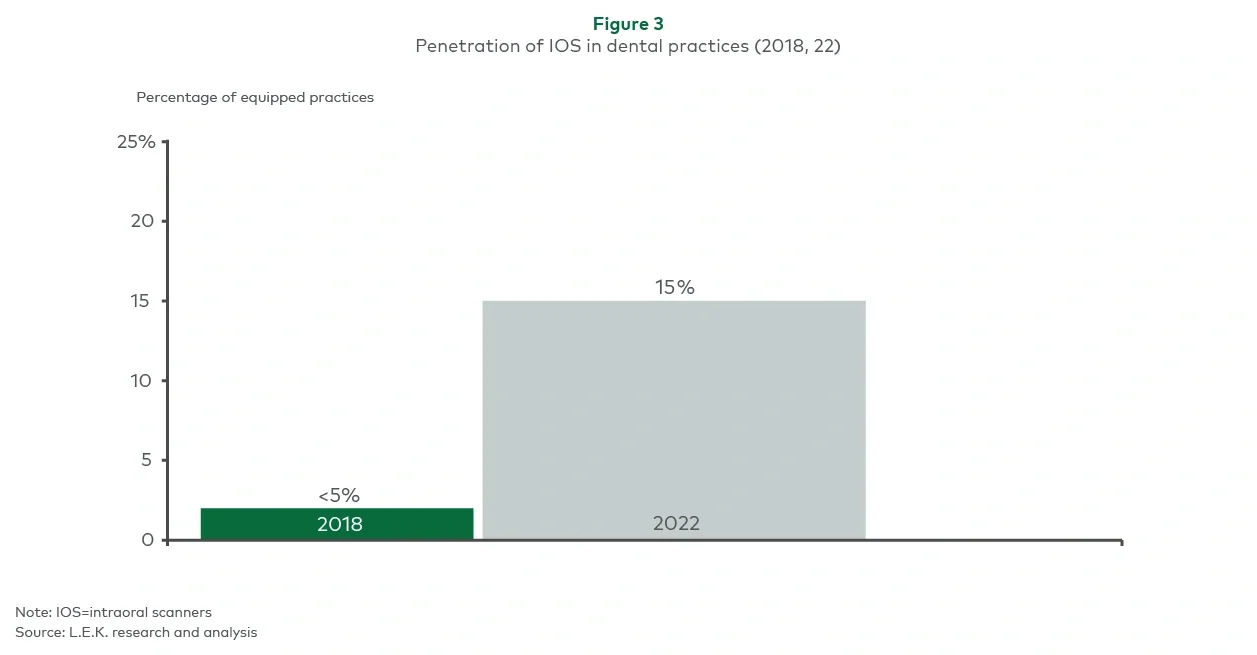

In lengthier treatments such as implants digitalisation is also playing a role, as it reduces the number of visits needed for fittings and adjustments. (see Figure 3 showing degree of digitalisation in clinics and dental laboratories)

However, there is a growing desire for better oral health and aesthetics, demonstrated by the increase in dental visits over the past 10 years, with now only 10% of the population delaying visiting the dentist beyond two years, down from 24% in 2010. Both culture and personal habits are shifting as patients have become better informed by health authorities and advertising of the benefits of improved oral health. Professionalisation of the sector and an increasingly patient-centric approach have also contributed, combining with newer, more modern and more aesthetically pleasing clinics to help mitigate some of the negativity associated with dental visits.

Despite attractive growth and profitability, the dental sector is still very fragmented in Europe, with dental clinic chains having a low market share versus independent dental practices. In Spain dental clinic chains represent around 15% of the dental care market, a figure not dissimilar to that of many European countries, whilst the UK and the US are more consolidated at 30% and 25%, respectively. Yet consolidation makes sense — benefits include increased negotiating power with suppliers of both consumables and equipment, improved branding and an increased return on investment from marketing campaigns, the ability to attract and train the best talent, and the centralisation of shared services and back-office functions, and ultimately increased profitability, when well managed. The advantages are clear, but there is still a long way to go to reach the consolidation seen across other healthcare and social sectors such as hospitals and care homes, where independent players are a dying breed.

Dental laboratories — a key component in odontology

A key component in the dental clinic value chain is the external dental laboratory, responsible for the manufacturing or customisation of products such as crowns, dentures, veneers and bridges which end up in the patients’ mouths affixed to implants or their own teeth, or as removable prostheses. Laboratories are even more fragmented than dental clinics, as historically little value was derived from scale because products were produced manually. Currently there are around 3,800 dental laboratories in Spain and 24,000 dental clinics, meaning an average of one lab for every six dental clinics. The dental laboratory market is estimated at 700 million to 800 million euros annually and represents roughly 10% of dental clinics’ expenditure. This means that on average dental laboratories have revenue of 200,000 euros, with two to four dental technicians. This is a clear example of a very fragmented market, but we are at a watershed moment: the sector is in the process of a major transformation with the advent of digitalisation, which will result in greater consolidation as it now makes sense.

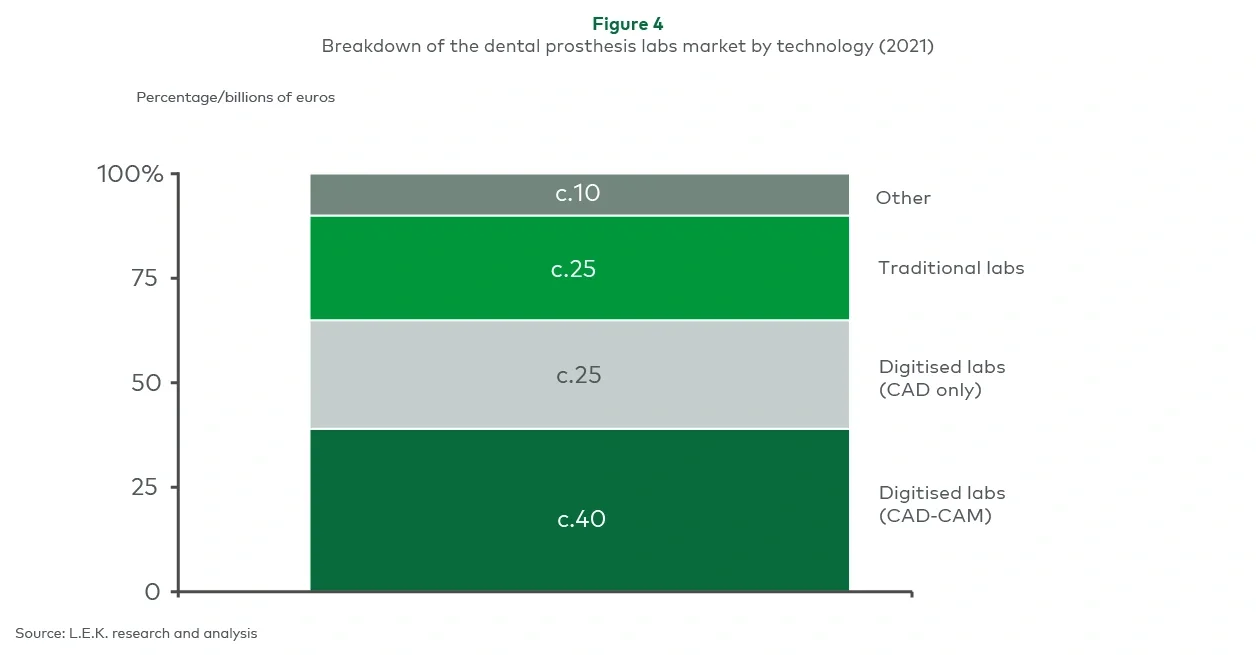

Approximately 25%-30% of dental laboratories still work exclusively analogically, and although 40% of the market has the capacity to undertake a full digital process (computer-aided design plus computer-aided manufacturing, see Figure 4), many will still use analogue processes in parallel. However, traditional laboratories are gradually dying out as they become increasingly uncompetitive; 10% of dental laboratories have closed in the past five years. Clinics increasingly demand more precise prostheses made possible by digitalisation. Digitalisation avoids multiple patient visits for fittings and adjustments — cutting overall visits by an estimated 50% — and consequently reduces expensive chair time and provides a superior patient experience and result.

This begs the question of why transformation is not moving at a faster pace. For the past decade, digitalisation has always been high on the agenda at dental fairs as the next great transformation, yet it is still a work in progress. Certain reasons are clear, such as the necessary investment, the less than perfect early equipment and the lack of qualified technicians, but the most important factor is laboratory and clinic owners, trained in a pre-digitalisation era, who are resistant to change and more so when what they are currently doing works well and has no attached risk. They may recognise the benefits, but that is often not enough. Therefore, this transformation is dependent partially on generational change and the teaching of new methods at university, and that is why it is gradual.

Digitalisation is winning

So, now we are living in a world of two parallel universes: on the one hand, we have 15% of dental clinics with advanced diagnostic imaging and intraoral scanners which produce three-dimensional models, working with laboratories which are 100% digital; on the other hand, we have traditional clinics and laboratories offering the same services as they have for the past 30 years. So far, these models have coexisted, but increasingly digitalisation is winning, resulting in a gradual but unstoppable trend.

Digitalisation is finally transforming the dental sector and making a clear argument for scale, as this is when the true benefits can be realised. Scale enables the creation of new products and even own brand products, enables the use and creation of new materials, provides the ability to train staff and invest in equipment, and powers the streamlining of processes and specialisation, driving efficiency and superior quality. This is an unstoppable train further accelerated by investors driving concentration. As larger dental laboratory groups are created, artisanal laboratories will be relegated to the history books. Given these tailwinds, we expect to see several significant transactions in the dental lab space in the coming months and years.

For more information, please contact healthcare@lekinsights.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting