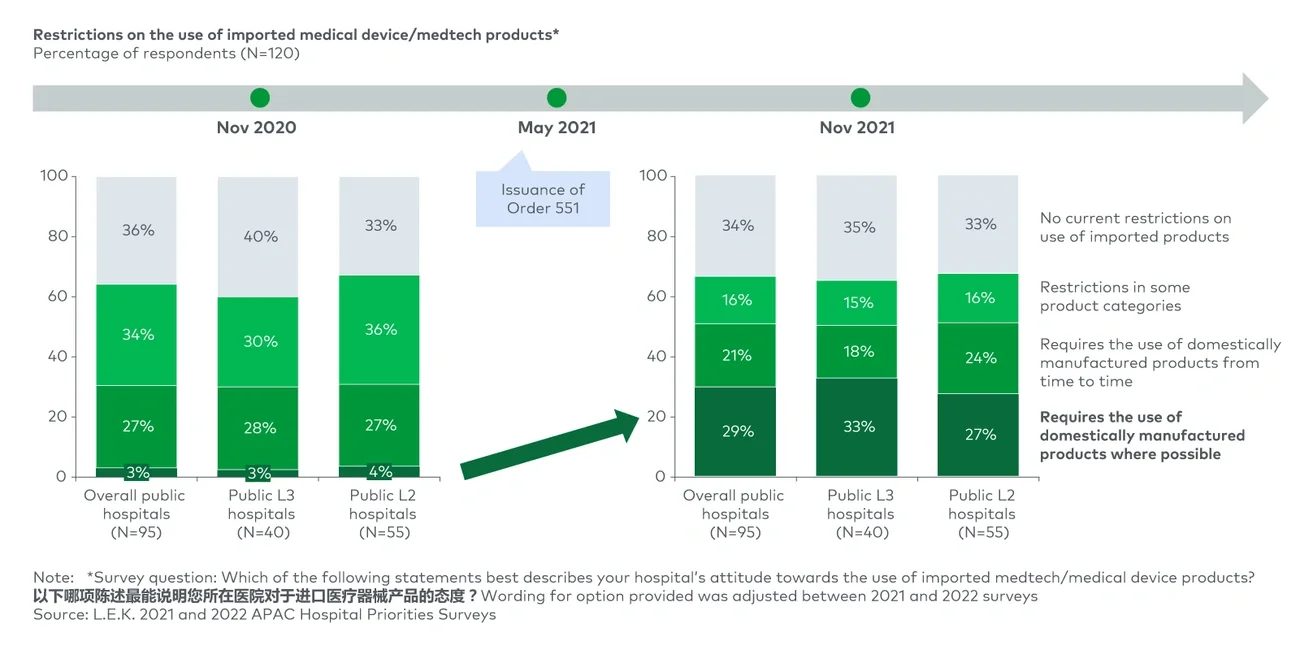

At the provincial level, a number of provinces have required import product evaluation, under which hospitals need to provide evidence to justify why they purchase imported medical equipment.

At a broader level, the policies supporting and favoring domestic products have been trending in a similar direction for several years.

A Made in China 2025 policy was first launched in 2015 to increase the proportion of domestically made, mid-to-high-end devices used in county-level hospitals to half by 2020 and to 70% by 2025 and to increase the share of domestic core medical device components to 80% by 2025. The policy is supported by the expedited registration of domestic devices and “buy local” procurement.

National guiding development plans, such as the 13th Five-Year Plan (2016-2020) and the 14th Five-Year Plan (2021-2025), further support the localization push. The more sector-specific Medical Equipment Development Plan of the 14th Five Year Plan, launched in December 2021, emphasized innovation, standardization, collaboration and talent recruitment to help leading domestic companies grow at 15%-plus per year, propelling six to eight of them into the global top 50 medtech firms.

More narrowly, several National Medical Products Administration (NMPA) orders from 2020 and 2021 also carried this forward. For instance, Order 104: Announcement on Matters Concerning the Production of Imported Medical Device Products, from September 2020, provided an accelerated registration pathway for transferring from “import” registration certificate to “local” registration certificate for medical devices and in vitro diagnostics.

We expect the combination of these policies and the overarching approach to create fierce competition for imported medtech products from Chinese rivals in the near future. Dealing with this regulatory and policy direction and the increased domestic competition that it will generate should be a high priority for MNCs in this space.

And, in fact, several multinational medtechs have recently ramped up their localization efforts in China. Among them are Danaher and Siemens Healthineers. Danaher invested more than $100 million in 2021 to establish a new diagnostics R&D and manufacturing base in Suzhou, and in 2022, it launched an upgraded China localization strategy to accelerate local manufacturing and local innovation with the aim of producing domestically 80% of the products the company sells in China.

Another case in point is Siemens Healthineers, which is moving forward with the localization of full product lines as one of the three core pillars of Siemens’ new China localization strategy unveiled in 2022. The company is putting considerable emphasis on this effort.

“The localization strategy is a critical measure for Siemens Healthineers to further integrate itself into China’s new development landscape and achieve joint development goals with China,” said Jerry Wang, president of Siemens Healthineers Greater China in 2022.

Going local

Going local in China is an easy-to-understand, but not always an easy-to-implement, approach. Localization allows medtech manufacturers to meet patriotic procurement policies while also being included in policies that are favorable toward local companies.

Yet the definition of what it means (and takes) to be “local” remains ambiguous and changes depending on the stakeholder. For the medtech industry, gaining a “local” registration certificate from the NMPA is the minimum.

Throughout all the steps in the supply chain, we have found that manufacturing a product domestically is key to its perceived “localness” among China’s clinicians and administrators.

Although NMPA’s local registration policy explicitly lists “locally manufactured” (准字号注册证) in the definition, it does not specify the percentage of manufacturing or the number of manufacturing steps that have to be done in the country for a product to be considered “Made in China.”

This means there is some wiggle room for manufacturers to simply move final assembly, configuration, sterilization or packaging to mainland China to qualify.

But interpretations can vary, and the NMPA currently takes a case-by-case approach. We predict that the definitions may be revised in the future and become more sophisticated. For example, the NMPA may add requirements for the percentage of manufacturing or minimum levels of value added domestically for manufactured products.

Which products to localize?

Right now, it seems logical for medtech manufacturers to move parts of their manufacturing processes to China to ensure continued access and competitiveness.

But we advise corporations to think carefully when assessing and prioritizing portfolios for China localization, as it is not necessarily the optimal approach for all products and you may not need it for certain products. We regularly advise clients to look at their strategic position through this prism.

Medtech companies in particular need to consider localization through four specific dimensions, namely, market dynamics, financial implications, operational complexity and potential enterprise risks.

The first dimension focuses on the market impact of localization. It weighs the implications on market size and future growth, competitive evolution, import substitution policies, and tendering constraints from the push to “go local.” This dimension also considers the importance of lower-tier market, as characterized by the city and hospital levels within China. Essentially, the more important the lower-tier market, the higher the impact that localization will generate, given that market access for imported medtech products could be more challenging in a lower-tier market.

The second dimension views things through the lens of financial implications, or simply put, the economics of it all. It considers how a shift to achieve Made in China status will affect a company’s revenue in both the short and long term and, subsequently, how it feeds into the cost of goods sold for both the China and ex-China markets. Logistics cost considerations and possible tariff mitigations can also come into play.

Meanwhile, the depth of a company’s operational complexity will impact its global supply chain capacity and even its product registration capabilities. There is also the matter of capital expenditure to think about.

The fourth and final dimension is the potential enterprise risks. Though China’s IP protection has improved considerably, there are unique challenges and risks with IP protection and technology transfers, which are required when going local.

Options to achieve Made in China status

Those that decide to push ahead with efforts to secure Made in China status have several options (see Figure 2).

With definitions still vague, companies have room to decide what depth of manufacturing localization to employ and how it fits with their strategic plans.

Contract manufacturing through a local MAH, joint ventures, M&A activities and building from scratch (greenfield) are all viable approaches to China manufacturing localization. To help decide on a direction, companies should analyze case studies based on how other key players have utilized the different pathways.