Sound fundamentals underpin the digital intermediaries market

A number of macroeconomic conditions make the underlying market for digital intermediaries an especially strong one:

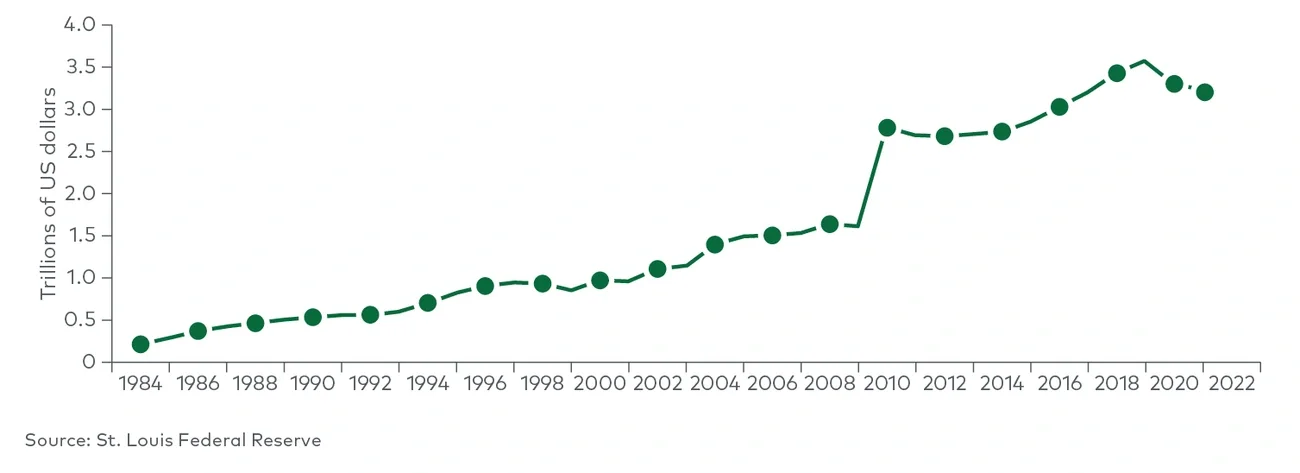

Low interest rates: Despite the Federal Reserve’s campaign to steadily increase rates, they remain within the range of historical norms; the target rate is forecast to decline by approximately 1.3 percentage points through 2025, based on a summary of economic projections from the Fed’s Open Market Committee.

Higher inflation: Highly inflationary environments like the current one result in high consumer prices, which creates a need for greater borrowing as well as an increased need to shop around for the best rate.

Low unemployment rate: The U.S. labor market has sound fundamentals, including a historically low unemployment rate, which means consumers have higher disposable income, so they spend more. This disposable income is being stretched by the current inflationary environment, but continued low unemployment preserves a population of potential borrowers (as evidenced by recent credit card origination and personal loan borrowing data).

Positive consumer sentiment: Consumer sentiment is a strong indicator of economic performance as consumers may pull back spending and borrowing during times of pessimism and spend or borrow more when they’re feeling optimistic. Currently, consumer sentiment may present a headwind, but only temporarily.

Rising household income (HHI): Growth in real median HHI (as it grew pre-COVID-19 from 2014 to 2019) improves consumer spending capability and makes financial products such as credit cards, mortgages and personal loans more affordable. HHI growth represents an important tailwind, assuming inflation continues to cool.

Positive demand-side trends: Consumers are increasingly financially conscious, aware of multiple product offerings, and seeking to take advantage of the most efficient financial vehicles available and apply them to a widening range of spending uses. In the meantime, new players in the credit card and lending space, alongside emerging digital payment methods like buy now, pay later programs and mobile wallets, are adding complication and nuance to the landscape.

Positive supply-side trends: Lenders are expanding access by launching more competitive product offerings for a wider range of use cases (e.g., travel credit cards, vacation loans) to a broader customer base (e.g., subprime borrowers).

Changing dynamics are fueling consumers’ need to shop around

As noted above, macroeconomic indicators began shifting in 2022, and the Federal Reserve has increased the federal funds rate to temper persistently high inflation driven by strong post-COVID-19 consumer demand, government stimulus efforts and a raft of supply chain challenges resulting from lockdowns, labor shortages and other macro disruptions such as the war in Ukraine.

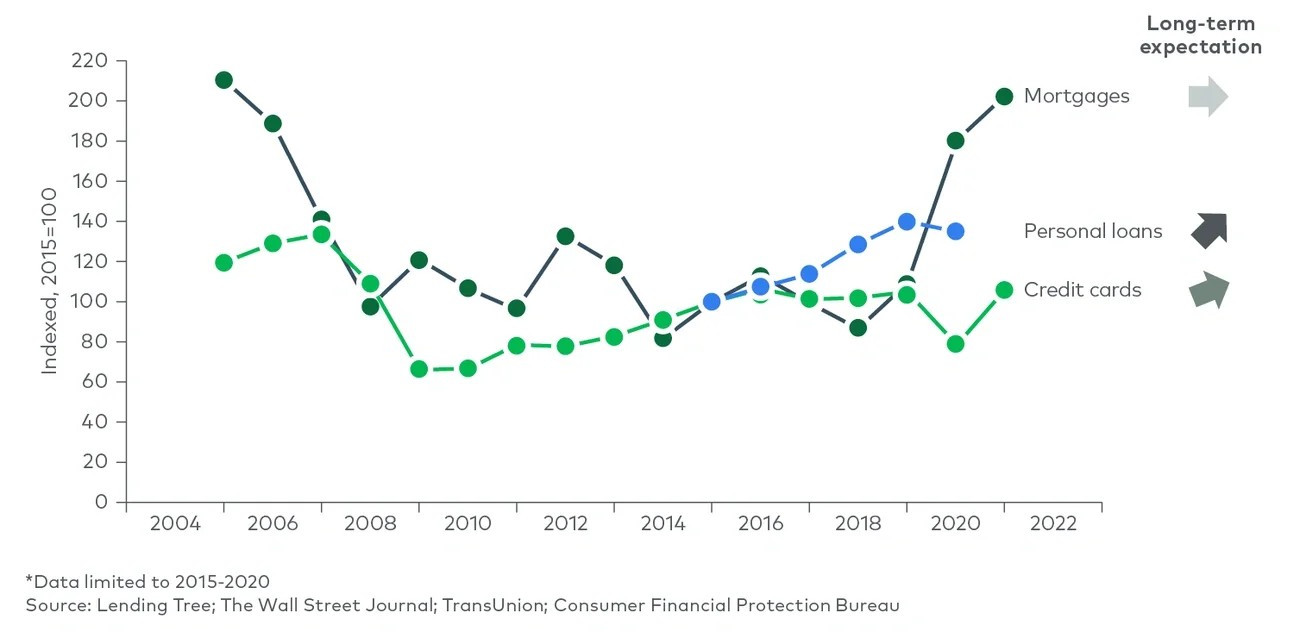

In the meantime, mortgage rates have been steadily rising (with some slight declines more recently), as the 30-year fixed rate exceeds 6.3% — well above 2021’s range, which largely hovered around 2%-3%. This has dampened home sales in the immediate term, though transactions are expected to grow as macroeconomic challenges moderate.

Such shifts place more pressure on consumers to make the best choice possible when shopping for financial products. After all, when the cost of borrowing increases significantly, lenders’ credit appetite may contract somewhat, leaving consumers without the option of defaulting to their existing lender or mainstream bank.

This creates a strong opportunity for digital intermediaries to become an even more important tool for consumers, as they provide a centralized way to compare offers across financial instruments, bringing clarity to the various trade-offs available and allowing consumers to choose the products that best suit their needs.

Digital intermediaries that have already established trust with consumers within the favorable conditions of the past decade will be well positioned to win in this environment. But that doesn’t mean there isn’t room for newer entrants as well. One way those that are newer to the market can increase their chances of success is by specializing within a particular product area and establishing strength there. Another is by providing consumers with a wide array of options and clearly articulating the trade-offs among them, though this avenue can be a difficult one.

Digital intermediaries have a long runway for growth

And in the current environment, the opportunity is especially ripe for established digital intermediaries and emerging players — as well as their investors. Established players can leverage their incumbent position and brand power to grow relationships with consumers by helping them find the best possible financial instruments during changing economic conditions. Emerging players, on the other hand, can look to enter underpenetrated markets and can provide consumers with unique content to establish themselves and build relationships. Investors, meanwhile, need to understand the markets that the various digital intermediaries serve — as well as their unique value propositions — and apply that understanding while the fundamentals underpinning this opportunity remain strong.

For more information, please contact strategy@lek.com.