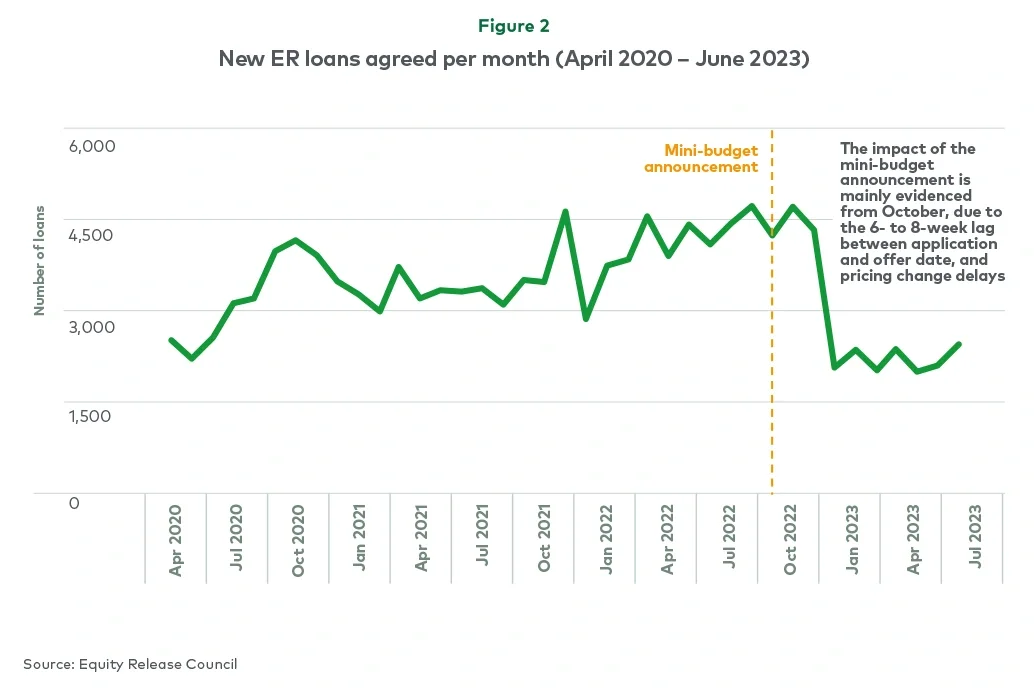

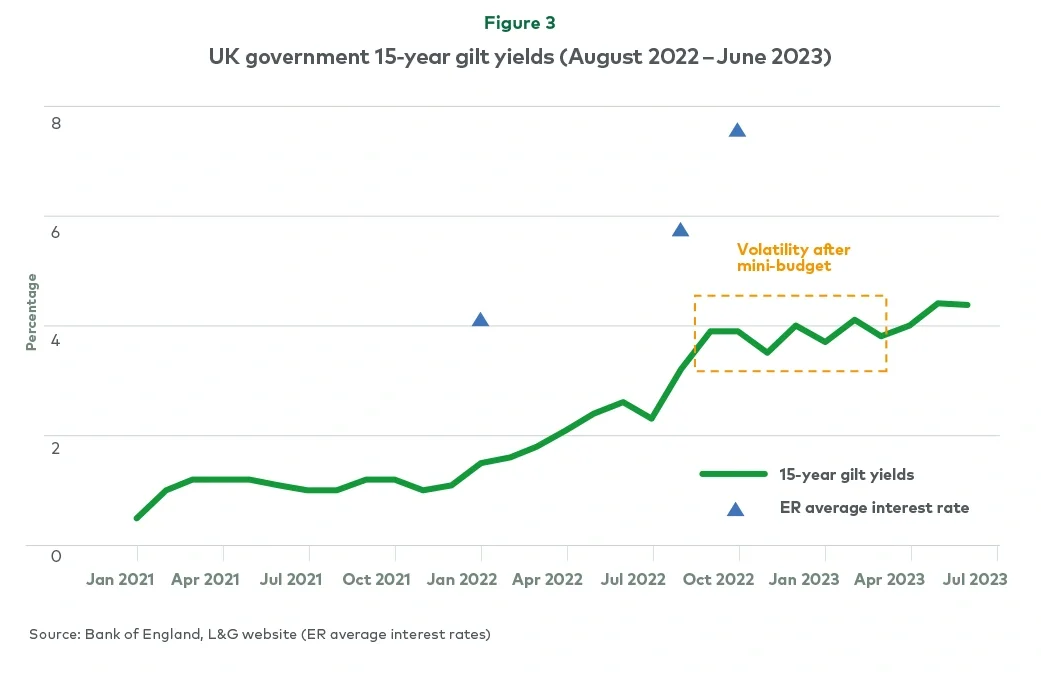

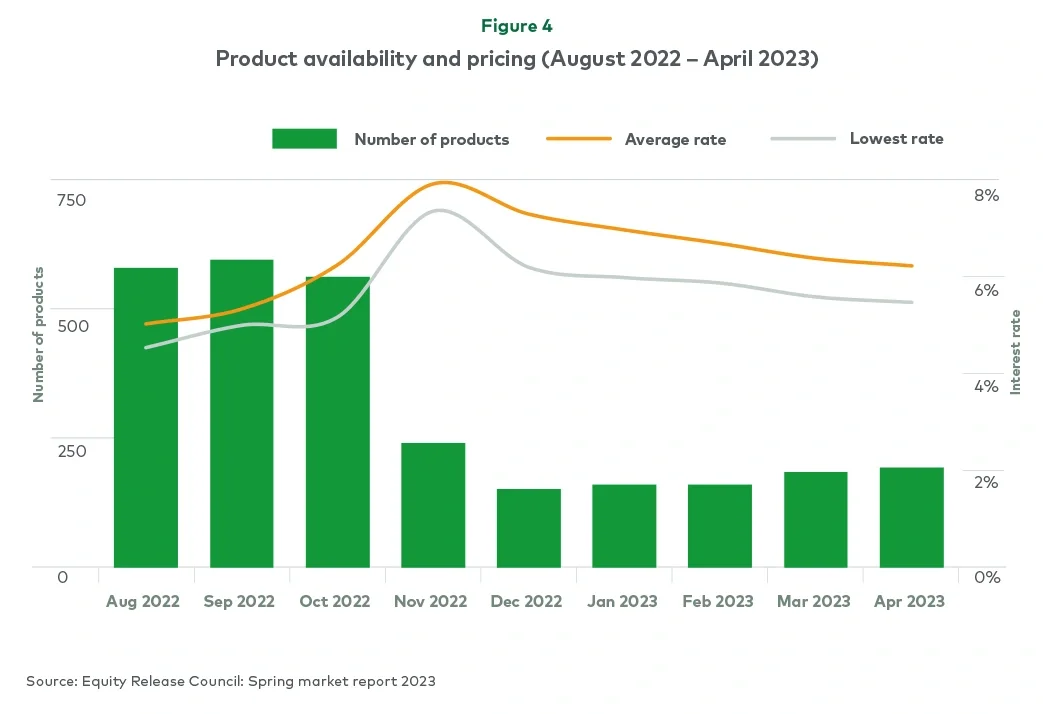

This significant drop in product availability (i.e. a drop of c.75% in number of products in the market), combined with reduced marketing activity of leading ER providers, caused the reduction in the total value and volume of ER loans in the closing months of 2022.

This was primarily a supply-side driven decline, not a needs-driven decline.

The outlook of the ER market remains strong

Despite the sharp decline in the last three months of 2022, the ER market is now on a robust recovery path, with leading providers experiencing attractive month-on-month increases in enquiries and flows of new loans. Flows in some customer segments (mainly lower LTV products) are already back to pre-mini-budget levels, and are set to outgrow them in 2023. In our view these are early proof that the UK ER market as a whole has far from gone into retirement.

The underlying, structural need drivers of this market all remain unchanged:

-

We have an ageing population, with a growing number of consumers reaching retirement age (>600k growing at c.3% p.a. for the next 10 years)

-

Inflation remains above long-term averages, continuing to drive up cost of living

-

Consumers with rich DB schemes are in long-term decline (2%-3% p.a.)

-

Property remains the largest proportion of retirees’ wealth

-

Care costs are continuing to increase

-

Rising interest rates are contributing to higher mortgage costs

In summary, the underlying need for ER is not an issue and has remained robust throughout the period, perhaps even intensifying. This was driven by financial pressure from higher interest rates, escalating cost of living and the rising cost of care. Even more, the temporary decrease in availability of high LTV products has resulted in significant latent demand from ‘younger’ consumers with unmet needs who are ‘forced’ to use lower LTV loans out of necessity to pay off existing debts. This increased and latent demand is not going away and will need to be addressed.

There also continues to be sufficient funding from traditional and established funders to support the short-, medium- and long-term growth of the ER market. This is because funders’ underlying need to structure pension liabilities is unaffected and continues to be driven by a buoyant DB de-risking market. Leading DB de-risking advisory firms estimate an annual flow of £40bn-£50bn for the medium term. Assuming an average of 10%-20% will be deployed in ER loans (as it has in the past), this alone would suggest an annual flow of c.£10bn is possible. In addition, leading providers are exploring increasing interest from alternative funders and funding sources (domestically as well as internationally).

While the consumer need is unchanged and remains robust, we do not expect a V-shape bounce back. This is partially due to changes in consumer behaviour that can already be observed in the market. ER customers are coming back to the market, but higher interest rates and lower LTV products have resulted in a shift from one-off lifetime mortgages to increasingly popular drawdown facilities, with an initial lower drawdown amount. However, as time goes by and cost pressures remain, these consumers will in due course return again to draw down to release equity from their property as they continue to need funding in their later years. This means a delayed flow, but not a lost flow, for ER.

Strategy and innovation are key requirements to win

The ER market could recover faster if products with higher LTVs become available to all consumer age segments. This could, and in our mind will, be achieved through product innovation, changes in traditional funders’ appetite and continued entrance of alternative funders. The market could also recover faster if demand for lower LTV products increases well beyond historical levels — a likely outcome given current macroeconomic conditions and some consumers in younger-age cohorts using existing offers instead of waiting for the return of higher LTV products.

ER is only one piece of the ‘retirement income puzzle’, and not the answer to all questions. An ageing population with a deep need for funding during retirement is (increasingly loudly) calling for innovation of the overall later-life lending market. Traditional and alternative funders have a long path ahead to find answers to this demand, but alongside the obvious challenges there are clear opportunities for those with the right strategy.

Having a clear understanding of consumer needs, thinking strategically and acting innovatively are all required to win in this market environment. Please get in touch if you would like to discuss the content of this paper in more detail and benefit from our experience in having advised firms in navigating the ER and later-life lending markets for over a decade.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting