Key takeaways

-

Asia-Pacific (APAC) is expected to be the fastest growing companion diagnostics (CDx) market, as CDx will play a critical role to alleviate APAC’s high cancer burden and promote effective oncology care.

-

Though market access for single biomarker CDx has been relatively successful, next generation sequencing-based CDx face reimbursement challenges as APAC countries cannot afford high costs without local proof of benefits.

-

To unlock the value of the CDx market in APAC, companies should form necessary alliances to demonstrate using CDx and targeted therapeutics lowers overall healthcare costs.

The Asia-Pacific (APAC) region, which is home to 60% of the world’s population, makes up a significant share of the global cancer burden. Given the higher prevalence of specific cancers in APAC and distinct Asian patient genotypes, diagnosis and treatment should be tailored to the APAC population. Therefore, opportunities exist for industry players to develop and increase the clinical use of precision oncology therapies and diagnostics to meet the specific needs of the APAC market.

In 2018, APAC accounted for 60% of the world’s lung cancer cases and deaths, and 75% of all gastric cancer cases and deaths.1 APAC’s high cancer burden will lead to increased healthcare costs. Oncology spending in Japan and pharmerging countries such as China and India is expected to hit almost US$20 billion by 2022.2 This is still significantly lower than the US$140 billion projected to be spent by the U.S. and the EU-5. Pharmerging markets spend less on oncology therapeutics and diagnostics because usage is constrained by availability and reimbursement.

Interestingly, Asian patients also have distinct genotypes in specific cancer types. For instance, East Asian patients with non-small cell lung cancer are more likely than their Caucasian counterparts to develop epidermal growth factor receptor (EGFR) mutations, and are also more responsive to treatment with EGFR tyrosine kinase inhibitors.3

How CDx can play a critical role

Precision oncology involves various diagnostics tests, such as companion diagnostics (CDx), which determines whether specific targeted therapeutics should be prescribed. Unlike complementary diagnostics, which are associated with a class of drugs and are not limited to specific uses in the labels, CDx is typically linked to a specific drug within its approved label. Although multiple CDx types are used to test for corresponding targeted therapeutics in several diseases, over 90% of globally approved CDx tests are associated with targeted cancer therapeutics.4

Studies have shown that under specific conditions, CDx can potentially improve the cost-effectiveness of oncology care. For example, a 2015 study on late-stage cancer patients in the U.S. demonstrated that genomic testing and targeted therapy can improve overall survival for refractory cancer patients while reducing average-per-week healthcare costs, resource utilization and end-of-life costs.5

Trends in CDx development

Most CDx tests consist of a mix of single-biomarker tests, performed largely on tissue biopsy samples using quantitative polymerase chain reaction (qPCR), immunohistochemistry (IHC) and fluorescent in situ hybridization (FISH) techniques. Next-generation sequencing (NGS) and liquid biopsy are recent technologies that will be increasingly used and thus will shape the future of the global CDx market. Current industry participants with NGS or liquid biopsy technologies include service providers such as Roche Foundation Medicine and Guardant Health, as well as equipment and reagent providers such as Thermo Fisher Scientific and Illumina. More players with products incorporating these technologies are expected to enter the market over the next five years.

Growth potential of CDx in APAC

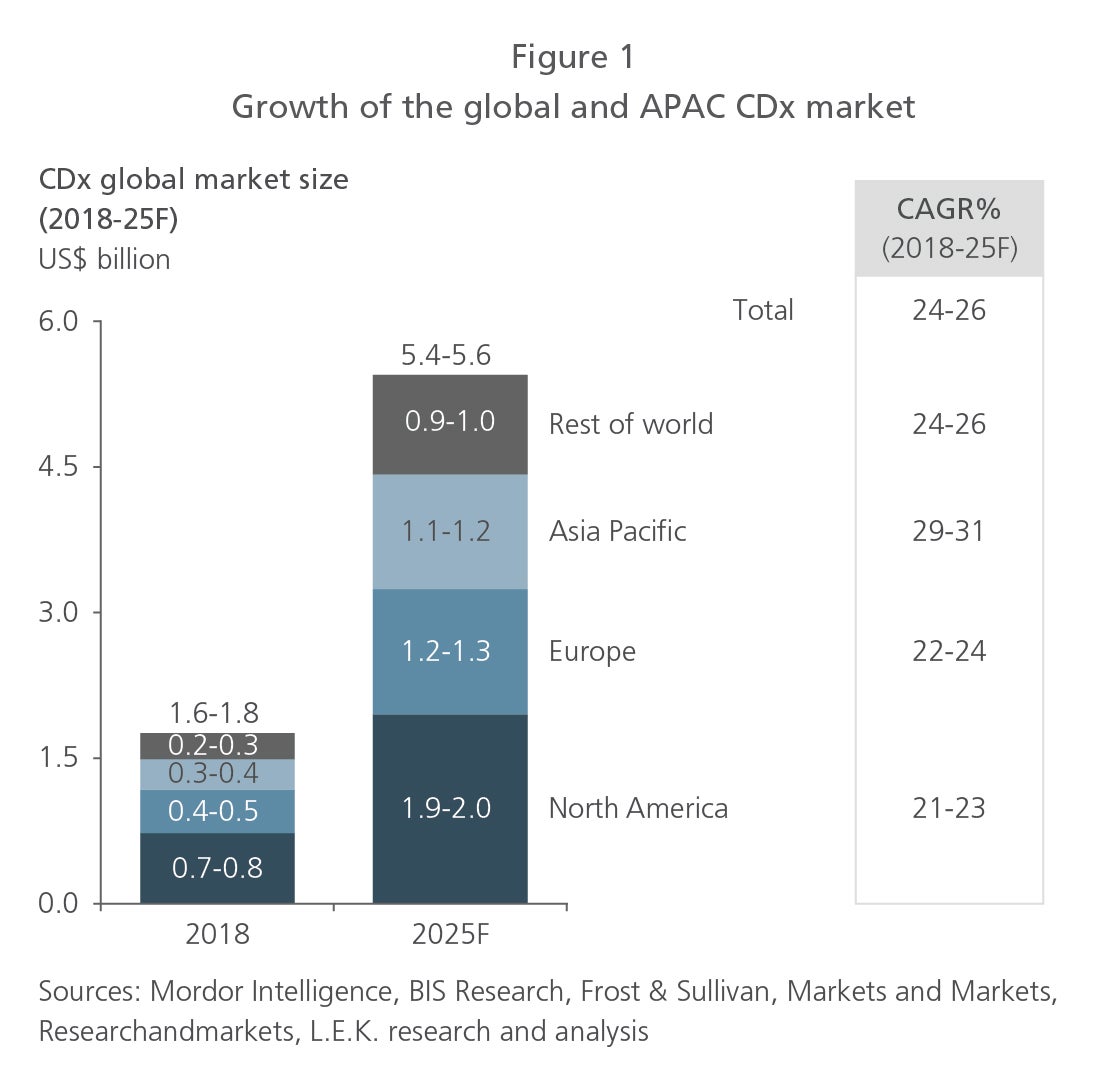

A strong growth outlook exists for the global CDx market. The global CDx market is estimated to have reached US$1.7 billion in 2018 and is projected to grow 25% annually to hit US$5.5 billion in 2025. Fueling the industry’s growth are an increasing demand for precision medicine to deliver targeted therapies to patients, the codevelopment of diagnostic and drug technologies, and the rising global incidence of cancer.

APAC is the fastest-growing CDx market. Valued at US$0.3 billion in 2018, the APAC CDx market is expected to grow faster than any other area of, and to become a major player in, the global market. It is forecast to expand 30% annually to reach US$1.2 billion in 2025. Spurring its growth are public and private initiatives to increase adoption of CDx, notably within countries such as China and Australia.

APAC Life Sciences Centre of Excellence

L.E.K.’s deep industry knowledge and proprietary tools, as well as Singapore’s strong research ecosystem, to produce materials on a broad range of life sciences and healthcare topics.

Current market access of CDx in selected APAC countries: progress and challenges

The current CDx market access landscape: APAC vs. U.S. and EU

CDx adoption is still in the early phases in APAC. The region lags behind the U.S. and the EU, which both had early leads in securing approval and reimbursement. For example, the U.S. already has more than 30 approved CDx tests, while only 15 are approved in Japan and even fewer in other APAC countries.6, 7

The path to approval: Where APAC countries stand in the development of CDx regulatory frameworks

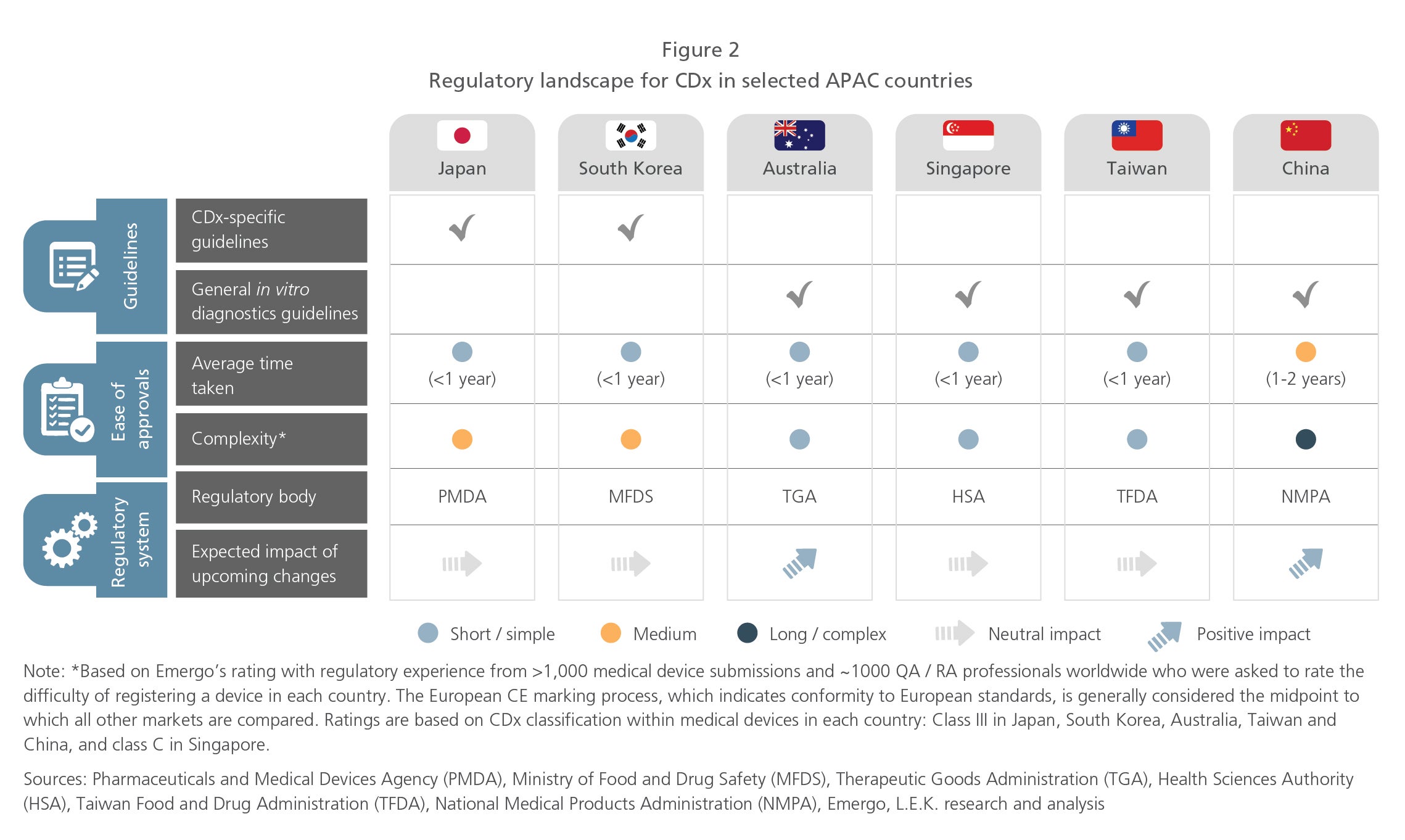

Market access for CDx is still evolving in APAC, with various countries at different stages of development. We examine the regulatory landscape for CDx in the developed APAC countries of Japan, Australia, Taiwan, China, Korea and Singapore.

Regulations can facilitate the widespread adoption of CDx by enabling coordinated evaluation of CDx and corresponding targeted therapeutic products. Currently, Japan and Korea are the only APAC countries that have published CDx-specific guidelines, including perspectives for CDx tests that utilize NGS and liquid biopsy technologies. However, other countries have yet to define such guidelines (see Figure 2).

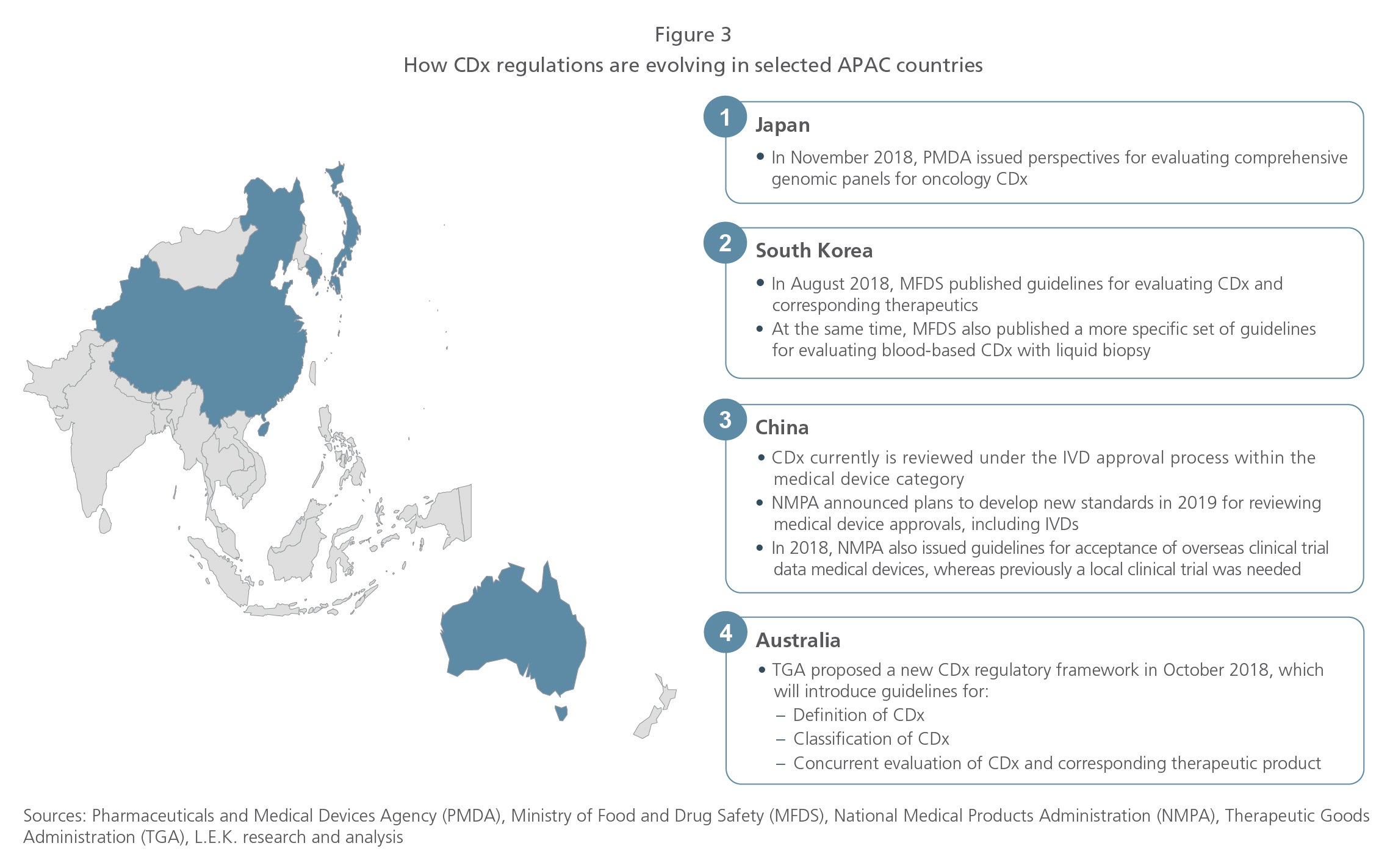

Reducing the timeframe for approvals is critical in bringing CDx to market. Like the U.S., most APAC countries have a short regulatory approval process: less than a year. China’s approval process, however, can stretch up to two years. Since 2018, Australia and China have begun reviewing their regulatory frameworks to potentially shorten approval time frames and reduce the complexity of the approval process (see Figure 3). These changes will drive greater CDx adoption.

Crossing the reimbursement threshold: The APAC experience

Reimbursement is also important in realizing the therapeutic and cost benefits of precision medicine as well as commercial adoption of CDx. So, what progress are we seeing in APAC, and what does the future look like for CDx?

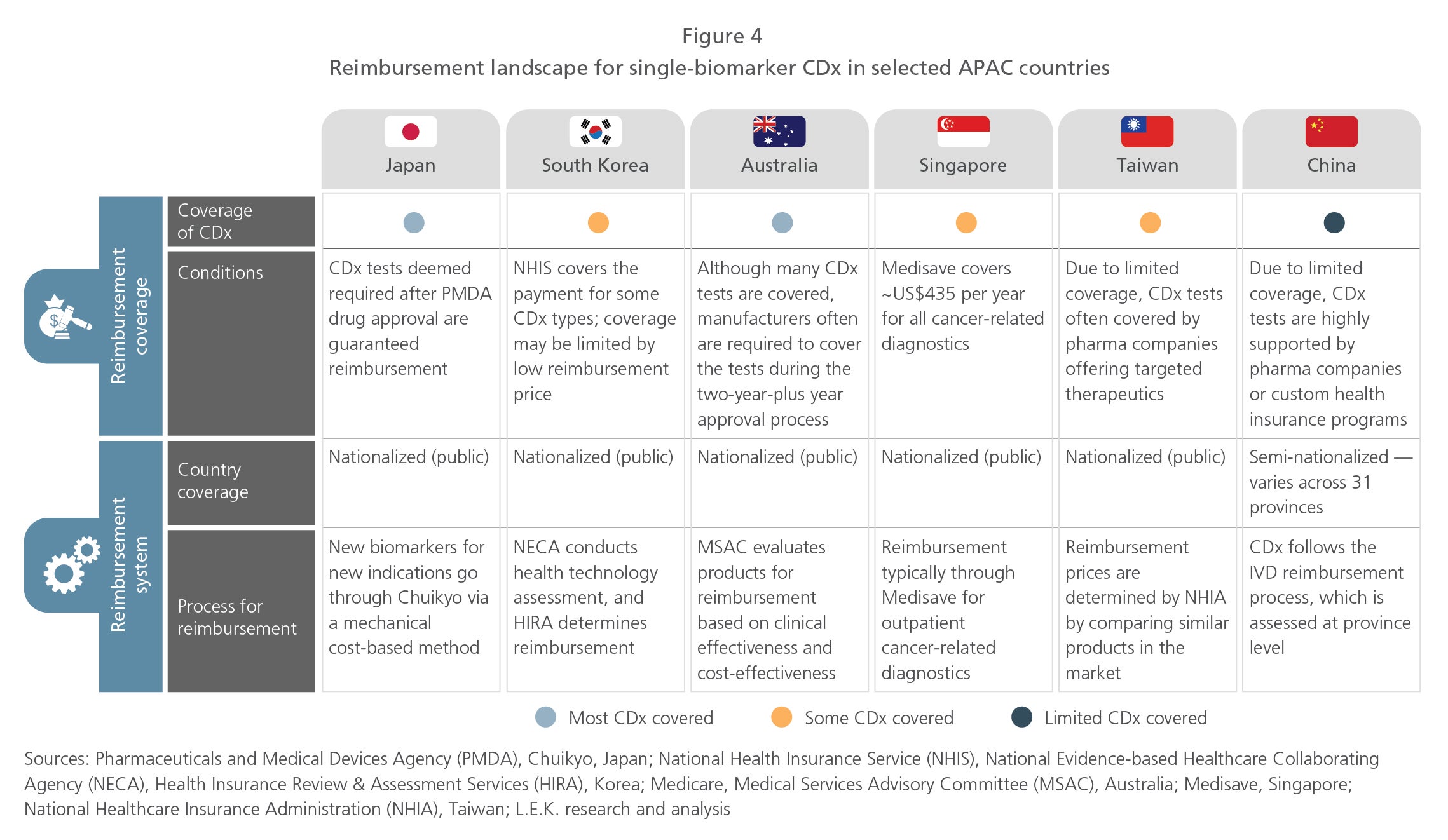

Diverse reimbursement policies for single-biomarker CDx. Reimbursement policies for single-biomarker CDx vary across APAC (see Figure 4). Most single-biomarker CDx tests can secure reimbursement in Japan and Australia, but other APAC countries do not have clear policies. China’s provincial-level reimbursement system for diagnostics has also hindered single-biomarker CDx adoption.

Due to varying CDx coverage in APAC, many pharmaceutical companies offering targeted therapeutic products often cover single-biomarker CDx tests, which are priced between US$60 and US$400, to accelerate market access. Due to the lack of coverage in most countries, however, reimbursement barriers still exist for single-biomarker CDx assays.

Challenges in coverage of NGS-based CDx due to high costs. NGS-based CDx has certain advantages over single-biomarker CDx. NGS technologies overcome the issue of limited tumor tissue through measurement of multiple biomarkers in one test, and enable collection of real-world data to expand indications for targeted therapeutics. Also, NGS-based CDx enables high-quality genomic profiling, which is required for some mutations that are difficult to identify via other methods. Examples include testing for high tumor mutational burden (TMB) for Bristol-Myers Squibb’s Opdivo (nivolumab), or testing for neurotrophic tyrosine kinase (NTRK) mutations for Bayer and Loxo’s Vitrakvi (latrotrectinib) and for Roche’s entrectinib.

Priced at US$2,000 to US$6,000, NGS-based CDx is more expensive and faces greater reimbursement barriers than single-biomarker CDx. Public reimbursement could be challenging across APAC, especially in price-sensitive countries such as South Korea and Taiwan, and pharmaceutical companies are also more reluctant to provide coverage at this price point.

Following in the footsteps of the U.S., which began Medicare coverage in early 2018, Japan is one of the first to provide NGS-based CDx reimbursement in APAC. Japan’s Ministry of Health, Labour and Welfare has recently approved reimbursement of Thermo Fisher Scientific’s Oncomine Dx Target Test, and is expected to decide on coverage for Roche Foundation Medicine’s FoundationOne CDx by mid-2019.

Key challenges for CDx adoption

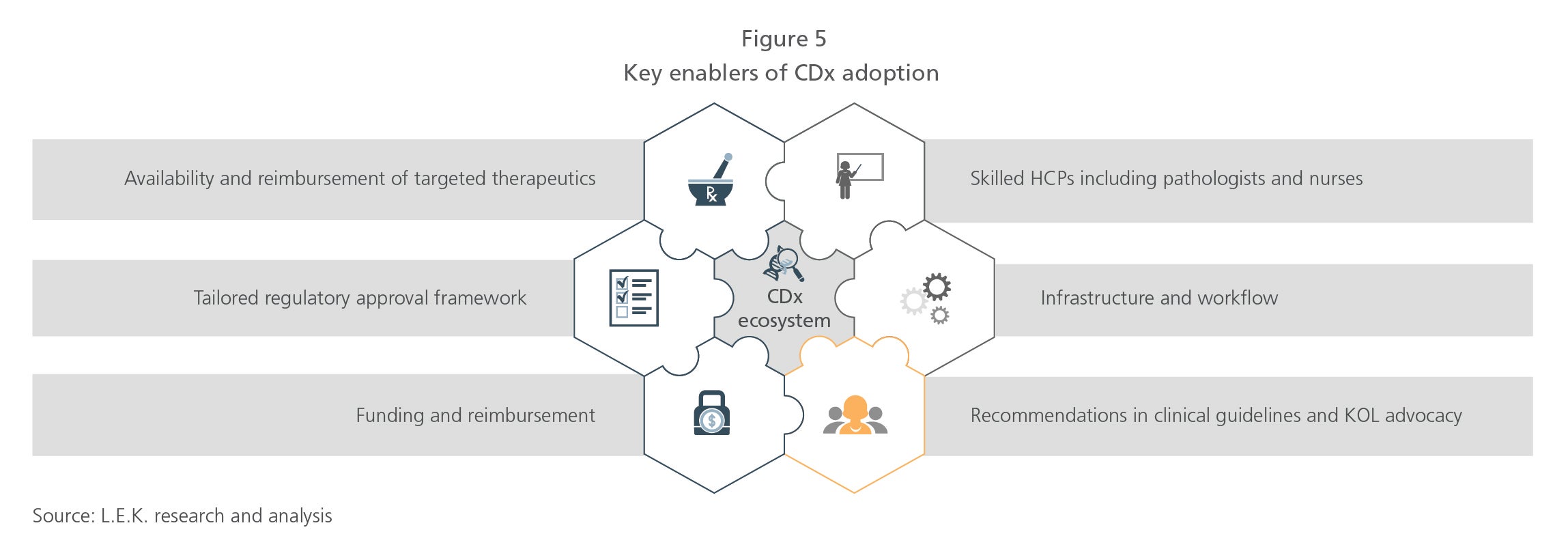

Critical success factors for CDx adoption

As APAC countries tap into the potential of CDx in precision medicine, they need to drive adoption of CDx by taking the following steps (see Figure 5):

- Improve market access for targeted therapeutics and CDx. Countries need to enable patient access to the targeted therapeutics and CDx, especially through reimbursement. First, countries should increase efforts to approve and reimburse targeted cancer therapeutics. The more targeted therapeutics enter the market, the greater the need to conduct CDx tests. Countries should then implement CDx-specific regulatory frameworks and define reimbursement coverage of CDx.

- Deepen engagement with HCPs. Second, countries should provide clear guidelines to healthcare providers (HCPs) and should encourage advocacy from key opinion leaders (KOLs) to foster greater CDx testing in daily clinical practice.

- Integrate CDx into daily clinical use. Finally, to ensure routine usage of CDx, countries need to build clinical infrastructure, train skilled HCPs, and develop simplified and standardized workflows across medical institutions.

Perceived barriers according to oncologists in selected APAC countries

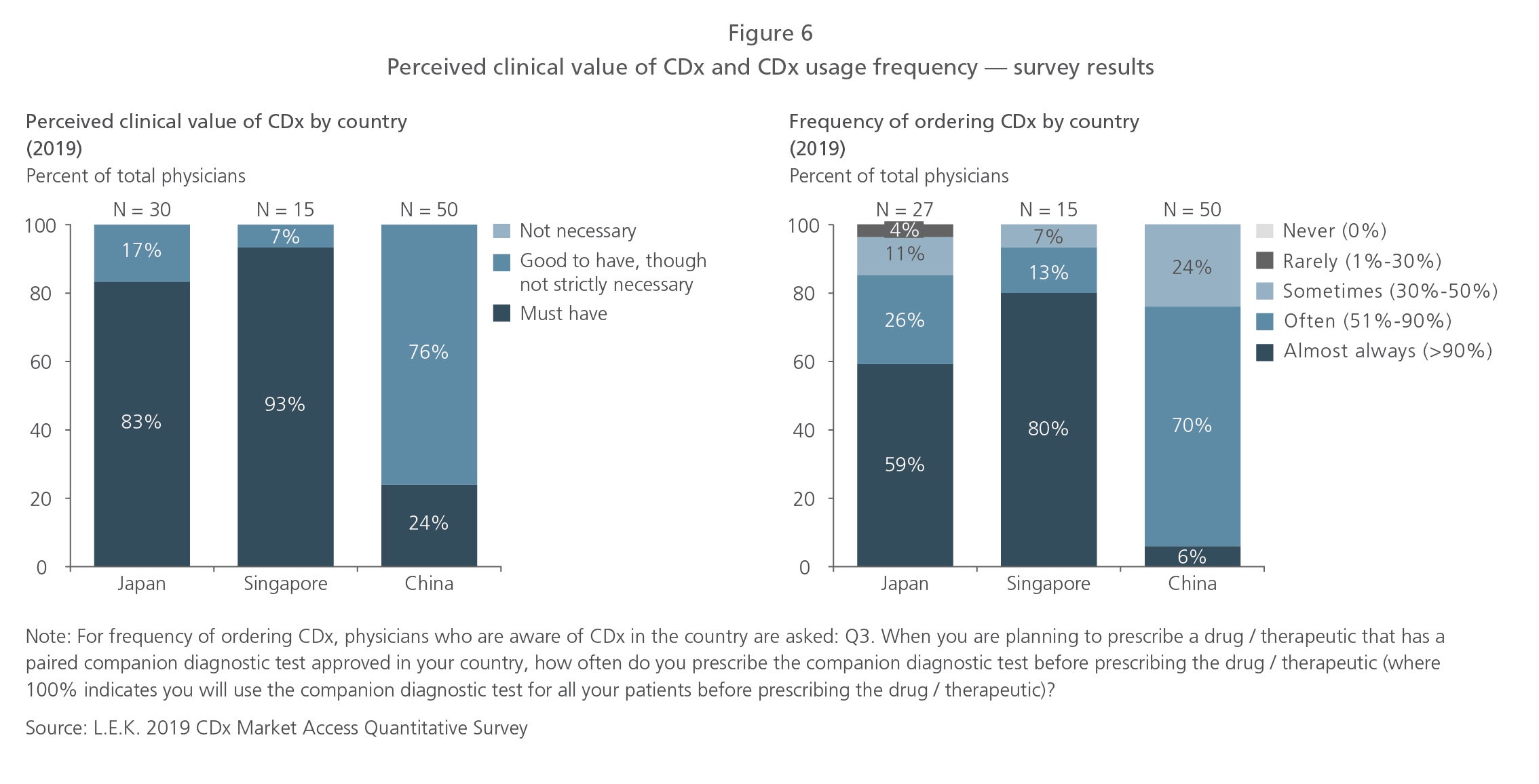

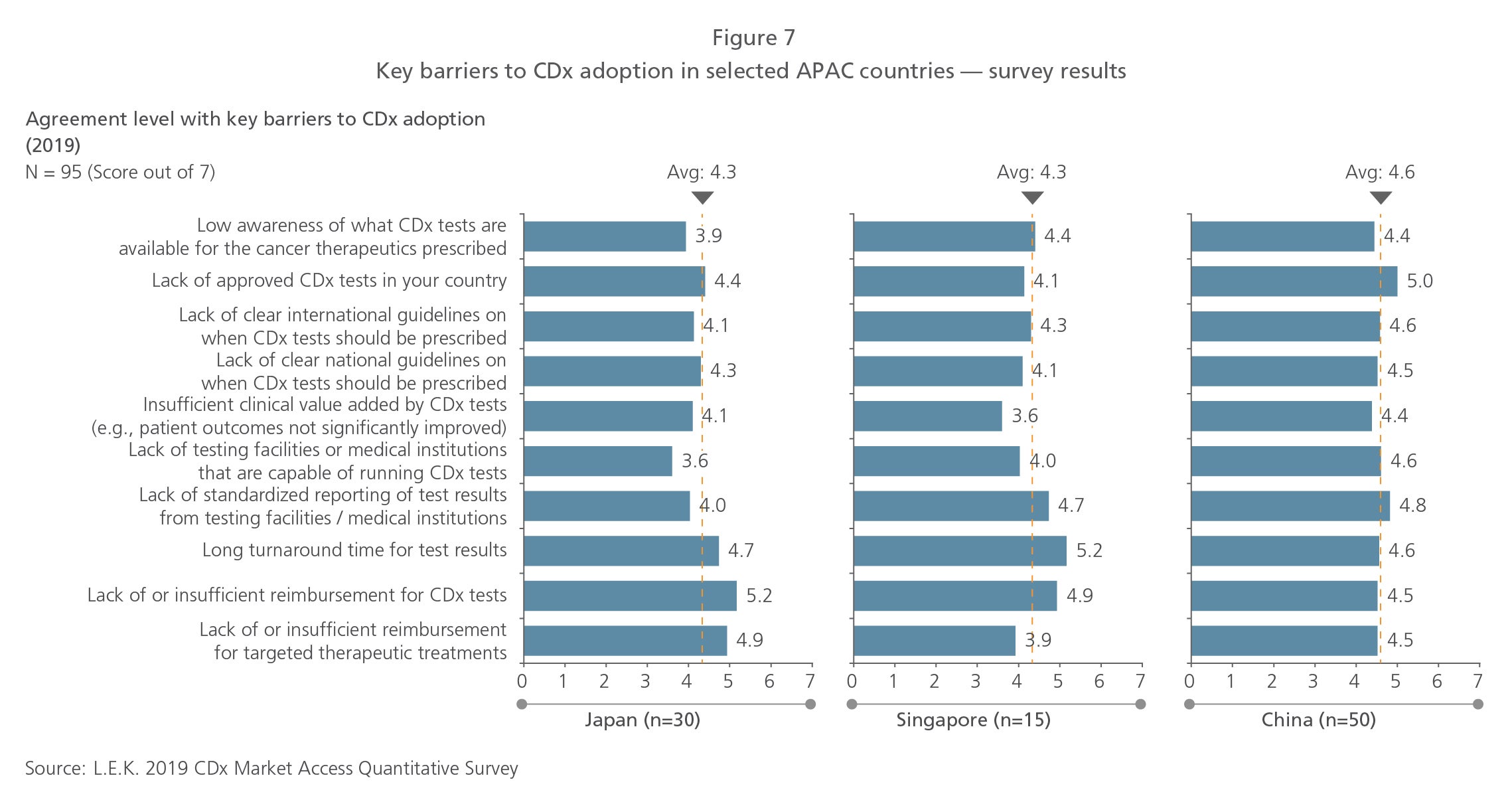

To better understand APAC oncologists’ perceptions of key barriers to clinical usage of CDx, L.E.K. Consulting conducted an online CDx market access survey in May 2019 with 95 physicians in Japan, Singapore and China who treated cancer patients with targeted therapeutics. Here is what we discovered:

- Perceptions of CDx utility vary, and usage differs. An overwhelming majority of physicians surveyed were aware of the clinical use of CDx tests in their countries. However, only 24% of the Chinese physicians believed CDx was essential to their clinical practice, and only 6% prescribed CDx to most of their patients being evaluated for a targeted therapeutic product. Although 80% to 90% of physicians in Japan and Singapore perceived CDx as essential, only 60% to 80% ordered CDx for most of their patients (see Figure 6). This suggests that some barriers to CDx adoption still exist.

- The lack of CDx reimbursement is a key adoption barrier in Japan and Singapore (see Figure 7). Physicians in Japan perceived the high costs of NGS-based CDx and patients’ 30% copayment after reimbursement as major barriers to CDx adoption. In Singapore, physicians felt that the annual Medisave coverage of US$450 for cancer diagnostics was insufficient.

- The lack of both approved CDx tests and standardized test results reporting are key barriers in China. Fewer CDx options may be available in China due to the lengthy regulatory process. The variation in equipment and tests available in labs, coupled with the lack of experienced pathologists who are able to interpret nonbinary biomarker expression results, also contributed to nonstandard reporting. These barriers may be reduced in the future as China begins to simplify regulatory processes and improve infrastructure with its national precision medicine initiative.

- Long turnaround time is a consistent barrier across all countries. Physicians in all three countries highlighted the long test turnaround time as a key issue. While single-biomarker CDx could be completed within a week, NGS-based CDx may take up to two weeks. Physicians indicated that cancer patients and their families tend to demand diagnosis decisions as early as possible, driving the need for a shorter turnaround time.

Key initiatives for CDx adoption

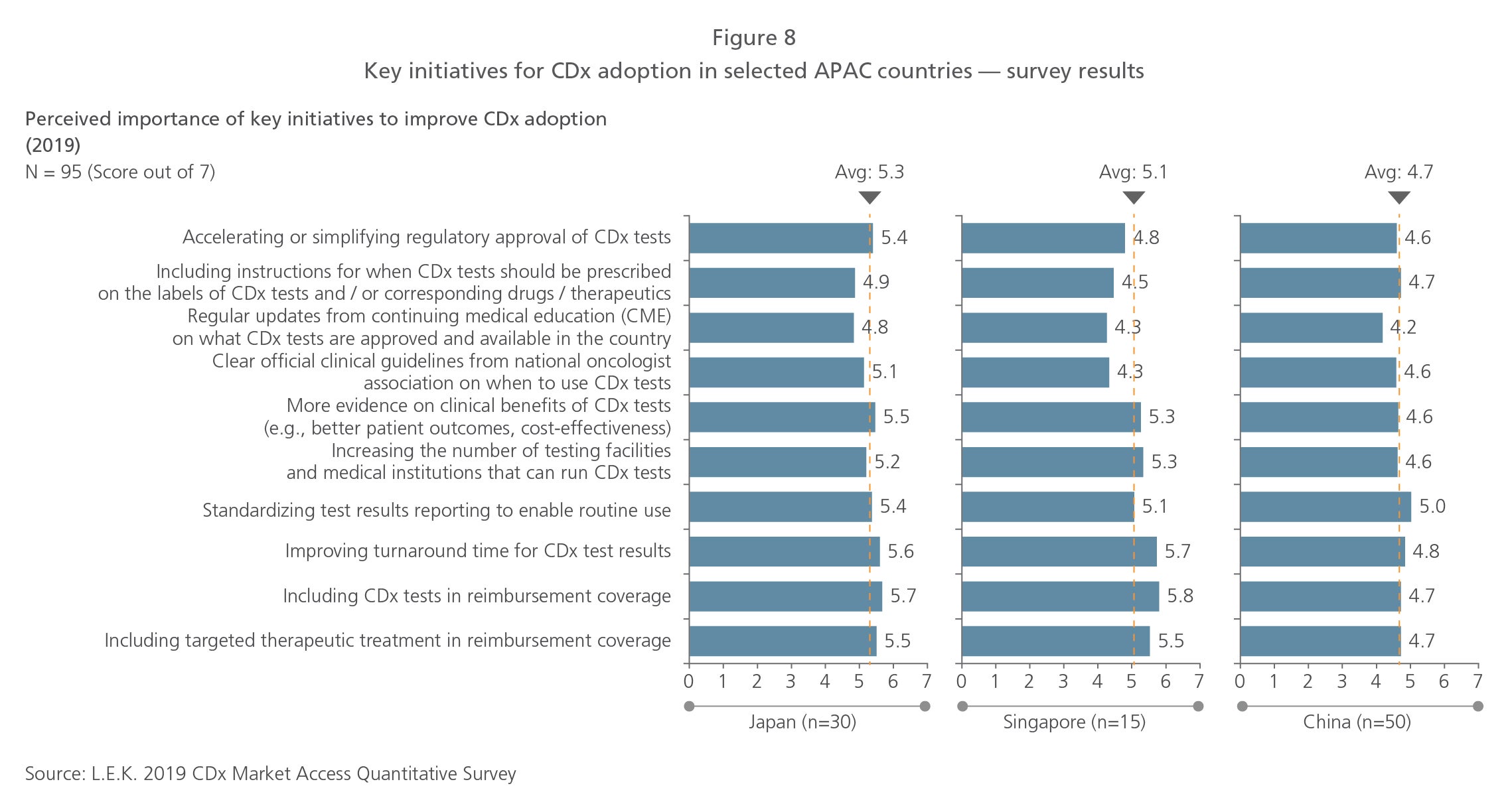

Preferred initiatives according to oncologists in selected APAC countries

L.E.K. considered oncologists’ perceptions of the most important initiatives for improving CDx adoption (see Figure 8).

The most important initiatives rated by the physicians generally mirrored the key barriers mentioned. Physicians in Japan and Singapore felt CDx tests should be reimbursed, while those in China believed infrastructure-related initiatives, such as standardized test results reporting, were the most important. A consistent preference across the countries was the need to improve turnaround time.

How can pharma and medical device companies support adoption of CDx?

The key barriers to CDx adoption are the lack of reimbursement for CDx and targeted therapeutics, as well as the lack of CDx inclusion in clinical practice.

However, old approaches focusing on the cost-effectiveness of a single intervention are unlikely to stimulate reimbursement actions. In addition, U.S. or European studies are unlikely to be accepted by APAC payers and providers as proof. Hence, it is necessary to show a systemic reduction in overall therapy costs (including costs for CDx, targeted therapeutic and healthcare delivery for patients across a progression of the diseases) in APAC countries, where budget continues to be a challenge.

To capture the CDx and therapeutic opportunity, industry players should consider these steps:

Create a plan

Both diagnostics and pharma players should identify where the highest cost burden exists in the CDx landscape and should match that to the current targeted therapeutic landscape. They should then focus on one or two cancers (or biomarkers) that have the greatest potential for therapy cost reduction using patient stratification and precision medicine. Specifically, they need to identify areas where the costs of CDx and the corresponding targeted therapeutic are likely to be lower than intervention costs arising from disease progression and side effects from non-targeted therapy.

Form synergistic alliances

An industry-wide initiative, such as SCRUM in Japan (see box),8 would be ideal to demonstrate overall lowered costs of therapy. Even a smaller alliance involving only a few partners — such as a CDx manufacturer, a pharmaceutical company producing the targeted therapeutic and a network of oncologists — would be beneficial in producing the necessary evidence.

Execute the plan and demonstrate benefits

Despite the initial high costs of CDx and targeted therapeutics, initiatives using these products should demonstrate not only lower overall costs but also better patient outcomes compared to treating patients over their full cycle of care.

Discuss with regulators and review necessary approval policies

To drive faster approval, industry participants should engage regulatory authorities to review current policies and should take guidance from countries that have established CDx guidelines.

Support changes in clinical practice through education

Industry players will also need to educate healthcare providers on how to interpret CDx test results and incorporate them into treatment decisions, particularly for newer NGS-based tests that physicians have less experience with.

APAC is expected to be the fastest-growing CDx market in the next five years. Despite current challenges, more opportunities for the precision oncology industry will arise as more countries pursue personalized medicine initiatives. To capture the full value of the CDx market, industry stakeholders will need to collaborate to tackle key issues such as reimbursement.

Case study on successful CDx adoption: SCRUM Japan

About

SCRUM Japan is a joint nationwide cancer genome screening project using CDx for patients with gastrointestinal cancers and lung cancers. It is a collaboration between approximately 17 pharmaceutical and diagnostic companies, as well as 250 medical institutions, led by the National Cancer Center and the National Cancer Center Hospital East.

This case study demonstrates that the presence of critical success factors in the country, as well as CDx-pharma company partnerships, are critical to drive successful adoption of CDx in APAC.

Objective

The project aims to match patients to the appropriate targeted therapies in clinical trials based on genetic analysis of their mutations, as well as to test clinical application of CDx that can detect multiple mutations.

Success and impact

In Japan, regulatory approval and reimbursement is a one-step process. As such, CDx tests used in the SCRUM study that were able to demonstrate efficacy, such as the Thermo Fisher Scientific Oncomine Dx Target Test Multi CDx system and Promega Tissue MSI Promega kit, were able to win approval and reimbursement.

The study has also received support from policy makers through the National Precision Medicine initiative, which will incorporate genetic analysis and diagnosis information from SCRUM. The initiative has used the SCRUM study data to augment e-learning content for healthcare professionals (HCPs). Establishing guidelines for prescribing the CDx will improve the skills of HCPs.

Endnotes

1Globocan 2018

2IQVIA Global Oncology Trends 2018

3Zhou, W., and Christiani, D. (2011). East meets West: ethnic differences in epidemiology and clinical behaviors of lung cancer between East Asians and Caucasians. Chinese Journal of Cancer, 30(5): 287-292

4U.S. Food and Drug Administration

5Haslem, D.S., Chakravarty, I., Fulde, G., Gilbert, H., Tudor, B.P., Lin, K., Ford, J.M., and Nadauld, L.D. (2018). Precision oncology in advanced cancer patients improves overall survival with lower weekly healthcare costs. Oncotarget, 9(15):12316-12322

6U.S. Food and Drug Administration

7Japan Pharmaceuticals and Medical Devices Agency

8SCRUM Japan

Acknowledgments

We would like to acknowledge Dr. Allen Lai, regional managing director of ACT Genomics, Simranjit Singh, Chief Executive Officer of Guardant Health AMEA (Asia, Middle East and Africa), and Devmanyu Singh for contributing their perspectives.

04292022080454