Key takeaways

-

Pet spending is a major component of U.K. household costs. At £153 million per week (nearly £8 billion per year), it’s equivalent to spending on take-home meals or soft drinks.

-

Spending on pets is growing faster than most categories, rising from £105 million per week in 2011 at an annual growth rate of 5.5%.

-

Growth is being driven by premiumisation, with pets being given fresh food with natural, high-quality ingredients and an increasing quantity of treats and accessories. Services such as veterinary and grooming are also growing fast.

-

A number of rapidly expanding providers are emerging in this dynamic market environment, including new challenger brands such as Naturo, Lily’s Kitchen and Good Boy.

-

Challenger brands have adopted three principal strategies to drive their success: new health-focused products, a marketing approach reliant on digital and PR, and varied routes to market.

-

Challenger brands have more room for growth in the U.K. and there’s also a major international opportunity in Europe and in the U.S.

Pet is a major category of U.K. household expenditure. With current spending of £153 million per week (nearly £8 billion per year), it is equivalent to spending on take-home meals or soft drinks. It has also been growing significantly faster than most categories, rising from £105 million per week in 2011 at an annual growth rate of 5.5%.

This growth is all the more impressive given the changing composition of the underlying pet population. The population of cats and dogs has grown by only 1% p.a. over the past seven years. Whilst there has been a slight shift to dogs, which now account for 55% of pets (up from 49% in 2011), at the same time there has been a move to smaller dog breeds. As a result, today’s pet population eats less food – in 2018, pets consumed 1,207,000 tonnes, down from 1,229,000 tonnes in 2011 (-0.3% p.a.).

Premiumisation and the growth in spending

So what explains the growth of the pet economy? Pet owners have long considered their Jack Russell terrier, Labrador or pedigreed Siamese cat as a cherished member of the family. Now, they are going a step further. The pet population may be eating less volume, but it is being fed higher quality food that reflects owners’ changing eating habits.

As the U.K. director of Mars Petcare explains: “Premiumisation is driven by pet owners willing to increase spend on super-premium products, [on] natural and scientific offerings, and on treating their pet.”

The human food and beverage sector is being transformed by consumers’ appetite for wellness and healthy living, functionality and authenticity, and affordable luxury. In the pet market, this translates as fresh food with natural, high-quality ingredients — and treats. Indeed, it is striking how the market for treats has grown in the past few years. In the seven-year period 2011-2018, some 40,000 extra tonnes of treats were sold to pet owners. Dogs have been the biggest beneficiaries.

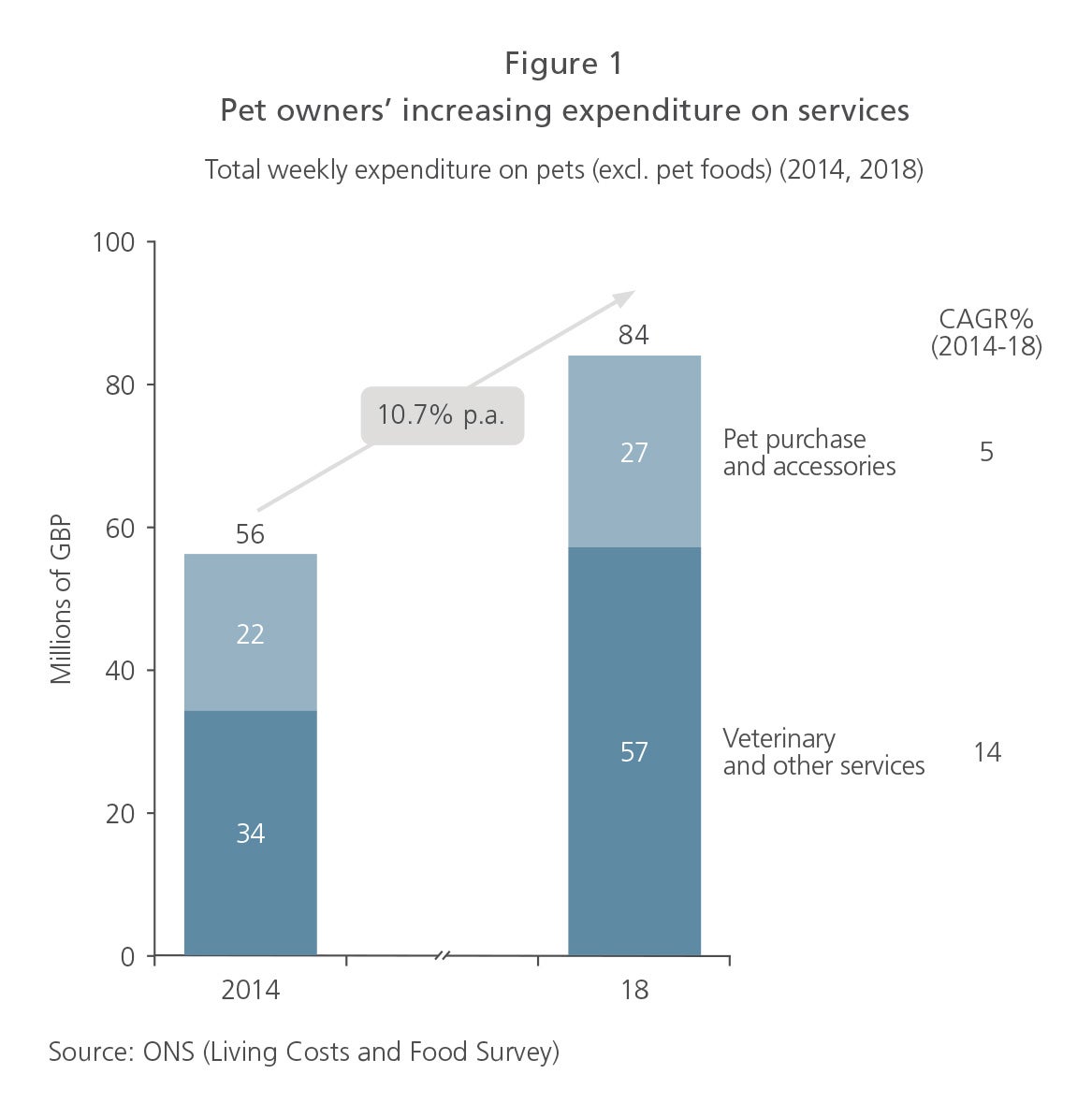

The phenomenon of treating pets with greater levels of care is apparent not only in the premiumisation of food but also in the readiness of pet owners — dubbed ‘pet parents’ — to spend money on a wide range of accessories and other services. As recently as 2014, pet owners spent £56 million per week on veterinary and other services (£34 million) and accessories (£22 million). By 2018, the amount had risen to £84 million at a compound annual growth rate of just under 11% (see Figure 1).

Expenditure on accessories represents just under 20% of the market. In a sign of the times, several luxury fashion houses are now offering pet products. For example, Barbour, the iconic British brand famous for its waxed jackets, produces a variety of dog accessories including harnesses and travel blankets, whilst Louis Vuitton offers an ultra-expensive dog collar.

The majority of the growth has been in veterinary and other services, rising by 67% to £57 million per week. Given that the size of the pet population has not changed much over the period, most of the growth has likely come from other services, such as grooming and dog-walking. This is roughly half the level of spend by U.K. households on their own hairdressing and beauty treatments (currently £104 million per week).

New providers lead the way

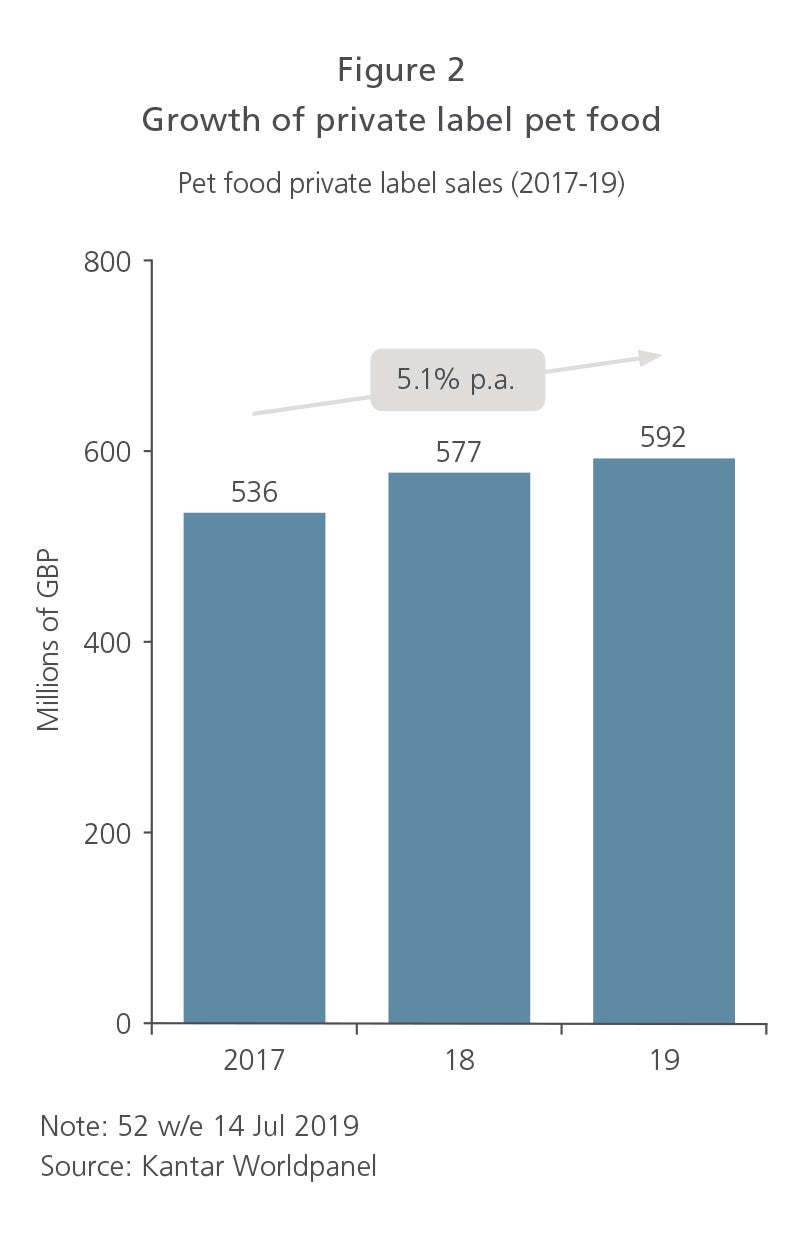

An expanding number of fast-growing providers are emerging in this dynamic market environment. It is still the case that the incumbent ‘majors’ — Mars Petcare with brands such as Pedigree, Whiskas and Cesar, and Nestle Purina with brands such as Purina One, Felix, Go Cat and Winalot — retain very strong share positions. But these brands are facing increasingly stiff competition from two different quarters. The major supermarkets, as well as specialist retailers such as Pets At Home and household goods chains such as Wilko, are starting to see significant growth from their private label pet food and associated products. In the two-year period from 2017 to 2019, sales of private label products jumped more than 10%, from £536 million to £592 million (see Figure 2).

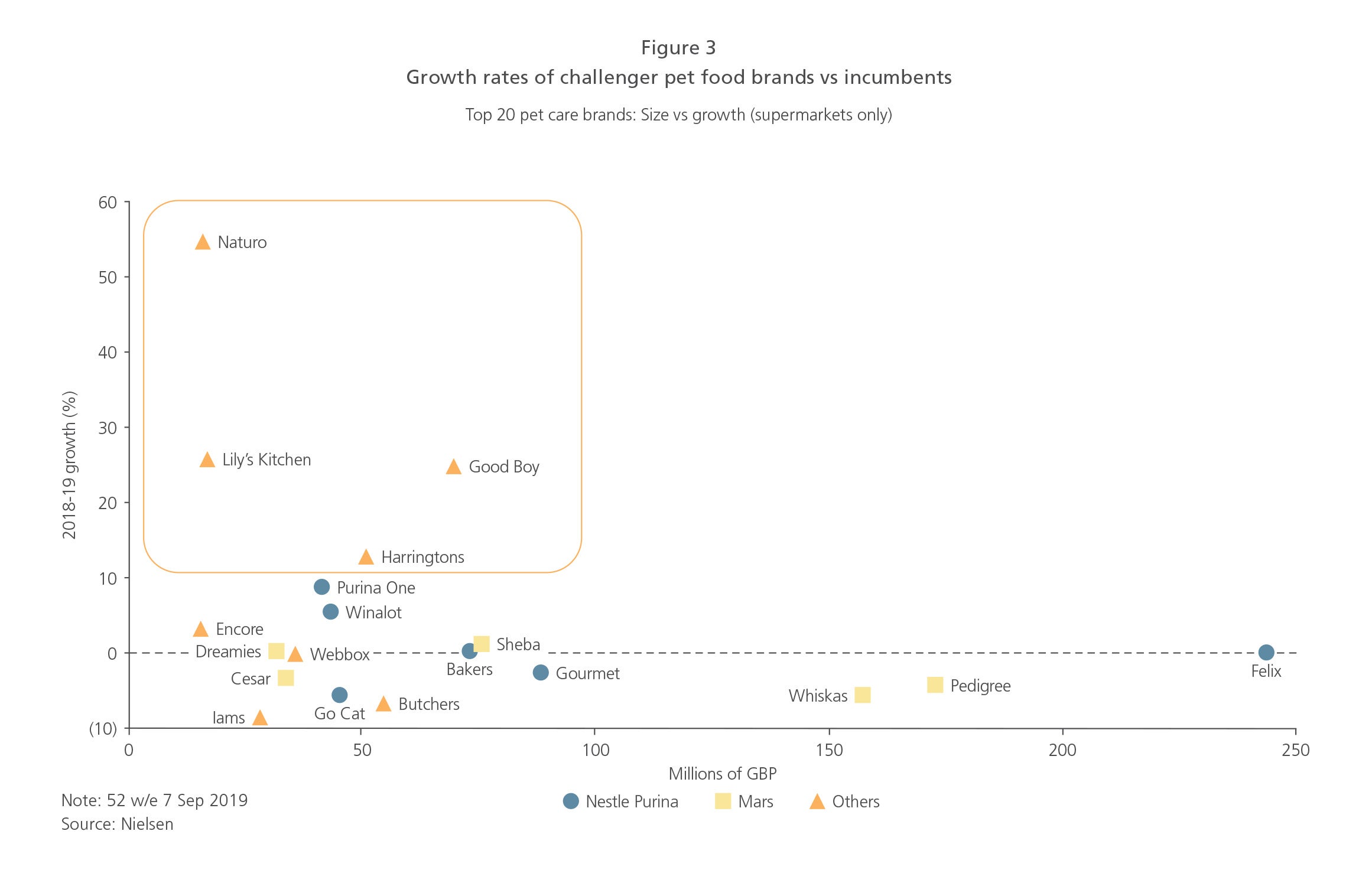

But the really striking development is the rapid rise of a new group of challenger brands that are doing things differently, capitalising on the new trend of premiumisation and enjoying some stellar growth. In the year 2018-2019, four brands reported double-digit growth rates through grocery retailers: Naturo (55%), Lily’s Kitchen (25%), Good Boy (24%) and Harringtons (11%). Over the same period, two of the biggest brands — Pedigree and Whiskas — contracted (see Figure 3).

Teaching old dogs new tricks

These challenger brands have adopted three sales and marketing strategies that are driving their performance:

- Offering an innovative range of products that appeal to pet owners who want to improve the diet of their pets. In the market for natural, healthy pet food, the emerging brands include Forthglade, Lily’s Kitchen and MPM. In the tailored nutrition category, the rising names are brands such as Butternut Box and Scrumbles, whilst in the treat category, Good Boy is prominent.

- Smart use of public relations campaigns and digital marketing to build their brand, create excitement around new products and communicate their source of differentiation in a crowded market. This is in contrast to the approach taken by the incumbent brands, which focus on traditional above the line advertising on television and radio and in-store promotions. It is noticeable that the younger brands are especially active on social media. We tracked three brands during January 2020. On average, Forthglade made 1.4 posts per day on Instagram and 1.3 posts on Facebook. Lily’s Kitchen was lower: 0.3 posts per day on Instagram and 0.4 posts on Facebook. But both posted more frequently than Mars-owned Pedigree.

- More varied routes to market. The incumbent brands focus on the grocery channel whereas newer brands, which struggle to get shelf space in the big retail outlets, have experimented with direct-to-consumer ecommerce as well as highly visible placement in local veterinary practices and specialist pet retail outlets such as Pets At Home and Pets Corner.

The incumbents appear to recognise that they need to up their game, as evidenced by the acquisition of Lily’s Kitchen by Nestle Purina in April 2020.

Where next for challenger brands?

U.K. pet owners have shown that they are willing to spend more on premium and natural pet food and treats. Penetration of these categories is still low and there remains plenty of runway for the challenger brands in their home market.

Looking beyond the U.K., there appears to be a material opportunity to increase spend in the pet category. In the U.K., pet owners spend, on average, £152 per pet p.a. on food, markedly more than both European and U.S. pet owners (£124 and £110, respectively). There is a big value prize at stake here — roughly £4 billion p.a. in Europe and £6 billion p.a. in the U.S. — and the new challenger brands have propositions that are well placed to exploit it. The key question is whether they can build the capabilities required to capitalise on the international market potential.

09222020100957