The COVID-19 pandemic famously prompted a surge in pet adoption as people sought companionship and suddenly had more time at home to engage in the early days of pet parenthood. This surge was a combination of pulled-forward demand and net new. Naturally, as the pandemic eased, the market for pets slowed down as well, largely due to that pulled-forward demand.

This left industry watchers wondering what the future holds for pet ownership. To find out, L.E.K. Consulting analyzed trends in the pet industry and surveyed 1,600 U.S. consumers about their attitudes toward and expectations for pet ownership. In this article, we share what we learned about who pet owners are, how they’re likely to behave and what this means for the pet industry going forward.

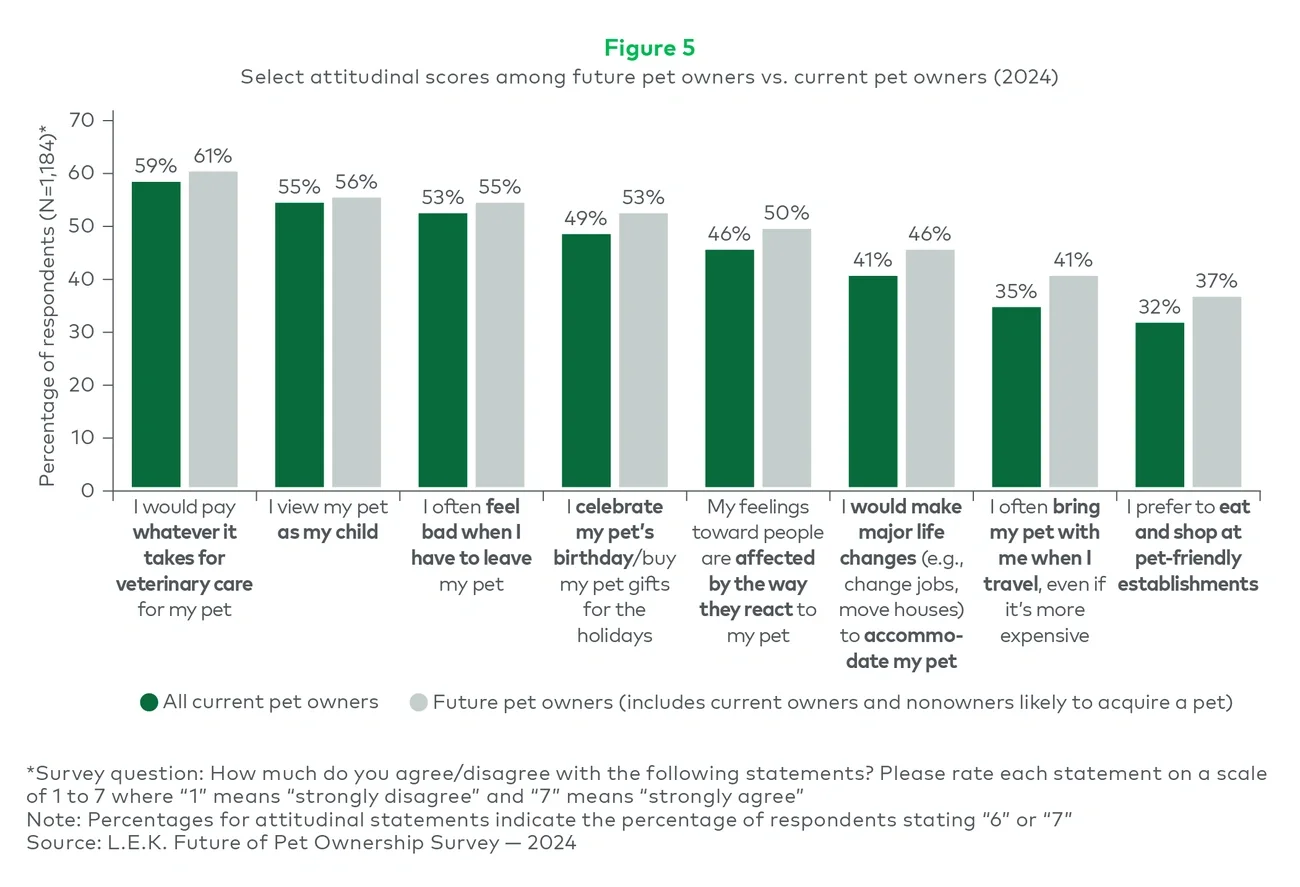

Pet ownership is sticky

Our consumer and market research suggest that the pet population will continue to grow, albeit not as quickly as before the pandemic. We estimate that, following a slight decline in the U.S. pet population in 2023, growth will remain stagnant in the near term. But over the next five years, we expect annual growth to stay around or under 1% per annum.

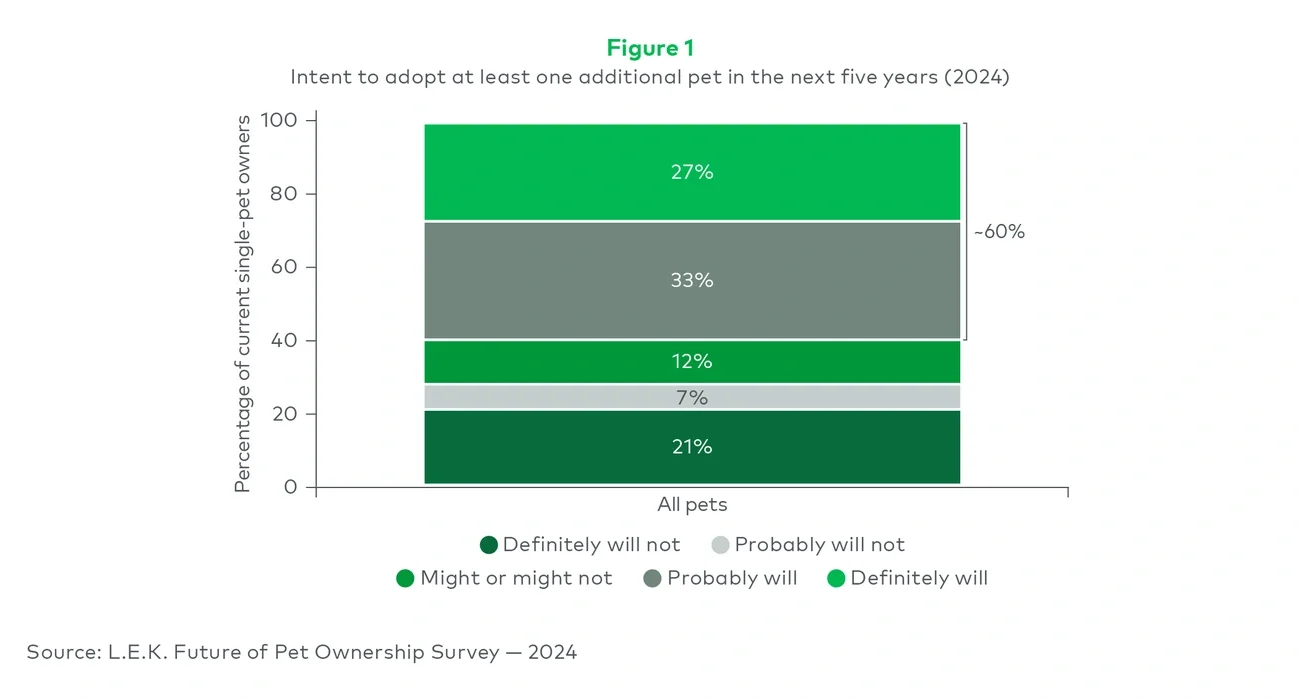

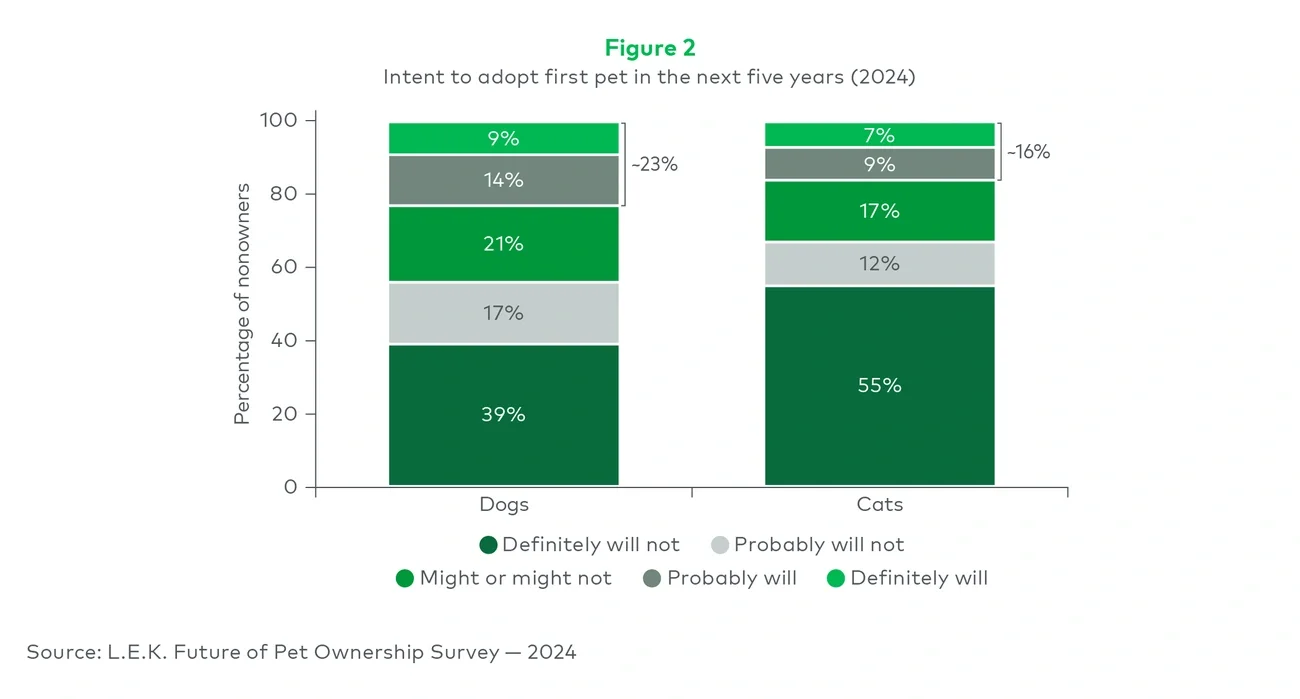

This slow-but-positive and steady outlook is due to several factors. One is that pet owners tend to remain pet owners, providing long-term stability to the pet population. Among survey respondents, 94% of dog owners and 97% of cat owners say they expect to replace their pet upon its passing. In addition, multi-pet households are likely to become more common, with 60% of single-pet households indicating they probably or definitely will adopt at least one additional pet over the next five years (see Figure 1).