Key takeaways

-

Securing reimbursement is a key challenge for digital health solution developers in Asia-Pacific, where solutions are treated as traditional medtech under most jurisdictions, which typically slows and/or limits access and increases investment requirements as compared with more digitally-tailored access regimes.

-

Some companies have nonetheless navigated reimbursement in the region, charting their strategy to draw on traditional medtech market access capabilities, as well as garnering the support of digital advocates and partners to pursue alternative funding until more widespread coverage is available.

-

L.E.K. and APACMed explored the reimbursement and broader monetization of digital health across APAC, identifying best practices used by some digital health leaders in the region. A summary is shared in this paper.

-

COVID-19 has been a catalyst for the development and adoption of digital health technology. Digital health solution developers should act now to engage with key stakeholders and secure their position in APAC’s fast developing digital health markets.

The rapid development of digital health and enabling technologies creates huge opportunities for access, clinical outcome and efficiency improvements across Asia-Pacific. Digital health, however, still faces a variety of adoption challenges in the region: These include the lack of a regulatory framework tailored to digital health, unclear reimbursement pathways, poor stakeholder familiarity with new solutions and difficulty integrating solutions into existing care paradigms.

In this Executive Insights, L.E.K. Consulting and APACMed explore the reimbursement and monetization landscape of digital health in APAC. This publication presents some of the best practices adopted by existing industry players to address key challenges faced in securing reimbursement, and provides a selection of digital health case studies, which serves to illuminate the path toward digital health reimbursement and monetization in APAC for medtech and digital health companies.

To identify the key success factors for digital health solutions, we have analyzed the practices of 15 digital health solutions and companies active in Asia-Pacific today. These have been painstakingly selected to span different therapeutic areas, applications, market access and monetization models, and to represent solutions commercialized by both established major medtech companies and startups. Looking for success naturally leads us to look at some more established products and companies that have managed to navigate the difficult waters of market access: A number of the examples we draw upon have already achieved reimbursement in Japan, South Korea, Australia, Taiwan and select provinces in Mainland China that have been most forward leaning in reimbursing digital health solutions within APAC.

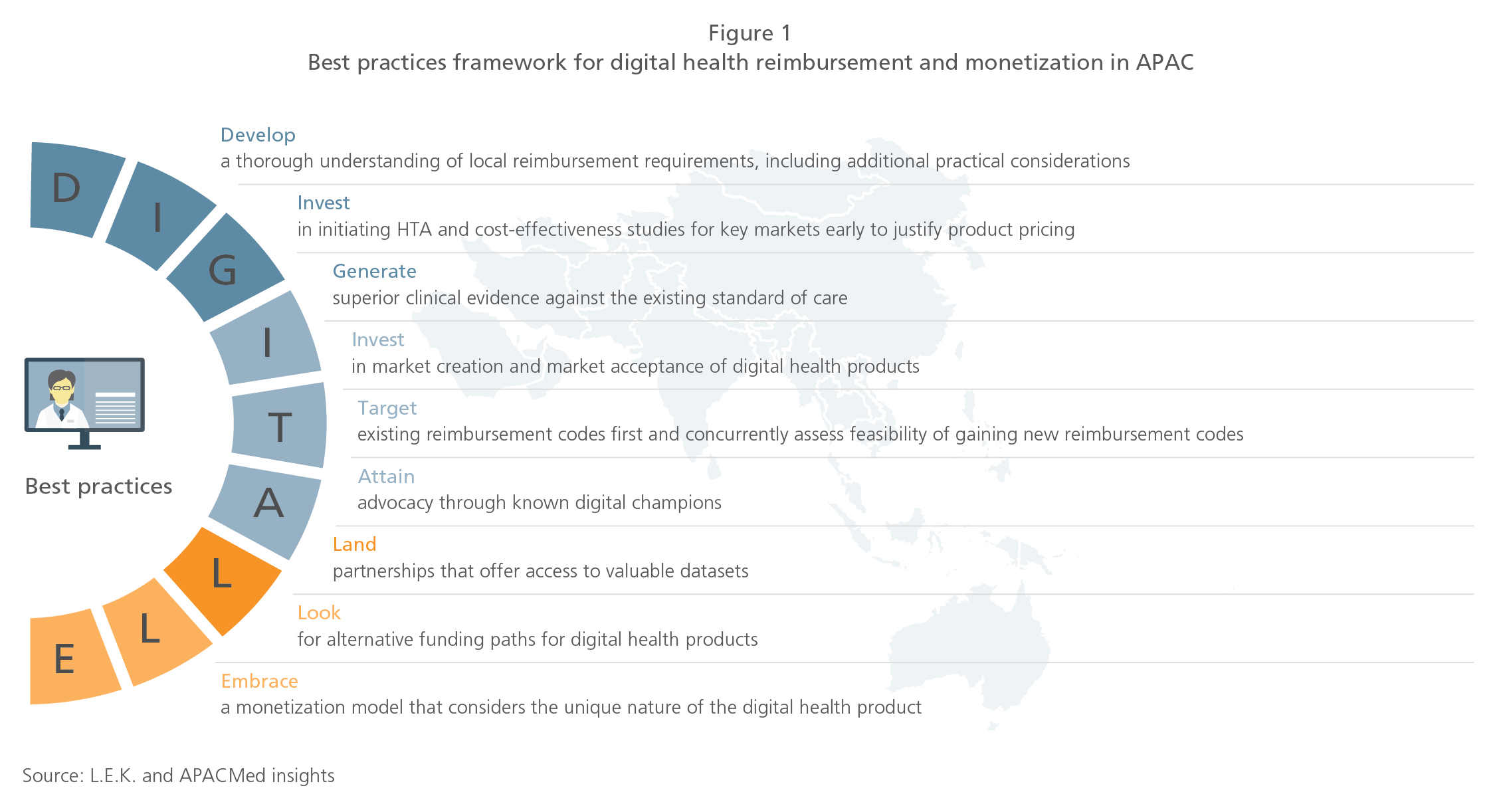

Overall, we have identified nine best practices (see Figure 1).

The first three of these best practices draw on existing medtech capabilities, as digital health solutions largely tend to get reviewed under classic medical device frameworks today.

- Develop a thorough understanding of local reimbursement requirements, including additional practical considerations. Understanding the reimbursement pathway includes knowing the “unspoken rules” through continuous engagement with reimbursement bodies. For example, Abbott (FreeStyle Libre) ensured that a randomized clinical trial was conducted for listing on the Medicare Benefits Schedule in Australia, although it was not specifically mentioned as a written requirement to gain reimbursement.

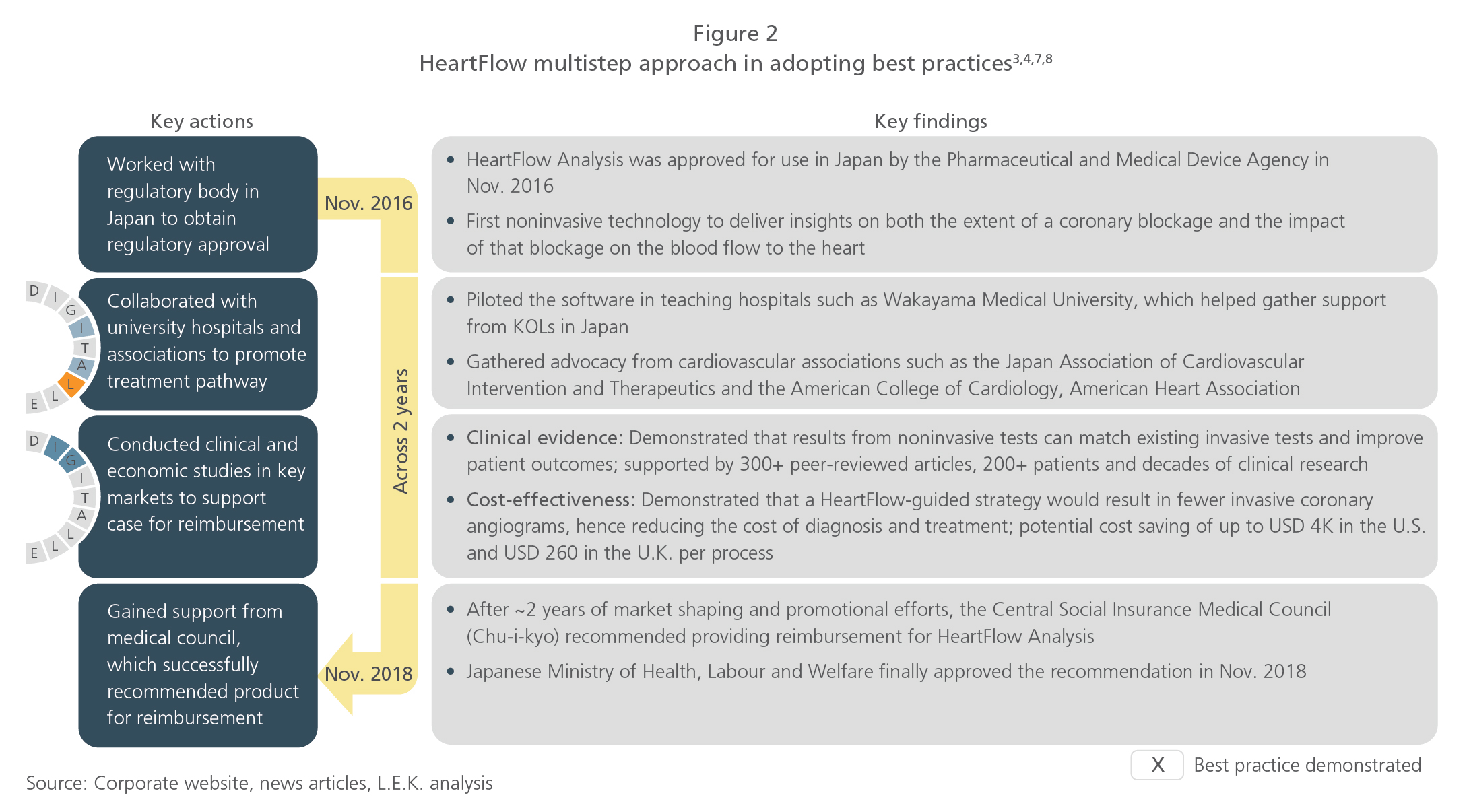

- Invest in initiating health technology assessment (HTA) and cost-effectiveness studies for key markets early to justify product pricing. For example, Intuitive Surgical conducted cost-effectiveness studies in Japan to demonstrate that total cost to treat per patient episode is lowered with its da Vinci robotic surgical system as a result of shorter duration of hospital stays.1,2 Others have leveraged studies outside of Asia-Pacific: For its technology HeartFlow Analysis, HeartFlow demonstrated potential cost saving of up to USD 4K in the U.S. and USD 260 in the U.K. per process.3,4

- Generate superior clinical evidence against the existing standard of care. For example, AliveCor clearly demonstrated in a randomized controlled trial that ECGs taken with KardiaMobile after discharge allowed doctors to diagnose more patients within a shorter time period compared with those who received the standard care.5

In addition to the best practices that mirror a medical device approach, there are additional steps that companies in the region have taken to specifically support the reimbursement and monetization of digital health solutions.

- Invest in market creation and market acceptance of digital health products. Companies need to commit resources and investment over multiple years to drive adoption of digital health, potentially through additional cost-effectiveness studies and ongoing evidence generation. For example, through continuous investments in Japanese market shaping and generation of evidence through clinical studies, Intuitive Surgical (da Vinci) achieved reimbursement for selected procedures after 10 years. In comparison, for the VNS Therapy System in Australia, Liva Nova had to commit resources to provide two years of health economics and clinical data.

- Target existing reimbursement codes first and concurrently assess feasibility of gaining new reimbursement codes. To speed up time to market, companies will need to work with existing reimbursement codes while concurrently seeking separate codes for digital health and higher reimbursement amounts. For example, as of 2020, B. Braun’s space pumps are reimbursed at the same rate as conventional pumps in Korea and Thailand, with no distinction made, and concurrently, the company is working with the Health Insurance Review and Assessment Service and the Ministry of Health and Welfare in Korea to obtain separate reimbursement codes.

- Attain advocacy through known digital champions. Throughout the product development life cycle, it is critical to identify and work with key opinion leaders (KOLs) and clinical societies that have demonstrated greater propensity to champion adoption of new technology. For example, in Japan, HeartFlow gathered support from professors and surgeons in teaching universities and associations such as Japan Association of Cardiovascular Intervention and Therapeutics for its digital health solution.6 In India, UE LifeSciences collaborated closely with public health agencies to facilitate large-scale implementation and gather advocacy in India for its iBreastExam device.6

- Land partnerships that offer access to valuable datasets. To support promotion of wide-scale digital health adoption, companies should also try to identify and build relationships with credible providers and channel partners that can provide access to substantial datasets for training algorithms. For example, critical to Infervision’s success in building superior algorithm intelligence is their partnership with some of the largest 3A hospitals in China, which gained Infervision access to the largest medical training database in the world.

- Look for alternative funding paths for digital health products. Companies should explore alternative payment options for digital health solutions beyond the public payer, such as tapping into public budgets (e.g., disease-specific funds) or targeting private payers supportive of digital health solutions. For example, Neurotrack worked with large private insurers in Japan — Dai-chi Life and Sompo Himawari — to roll out its digital Neurotrack Cognitive Assessments.

- Embrace a monetization model that considers the unique nature of the digital health product. Consider various dimensions for the monetization model; additionally, monitor market conditions and adapt the monetization model over the product life cycle. Monetization models include:

- Pay per use: for solutions that perform tests or analyses on a one-off basis

- Upfront plus maintenance/rental fees: for solutions that require regular maintenance after initial purchase

- Device plus consumables: for devices that come with consumables that have to be replaced on a regular basis

- Upfront plus subscription fees: for solutions that require additional software support or premium software features

Digital health companies need to remain agile and adapt monetization models based on market responses. Here are two examples of digital health companies that have evolved their monetization models over time.

- Toyota: For its Welwalk robotic system, Toyota revised its monetization model from a leasing basis to a purchase plus monthly maintenance fees approach, due to updated market assessment and healthcare institution requests.

- Butterfly Network: For the Ultrasound iQ device, Butterfly Network introduced its Enterprise business model, in addition to the original Pro Individual and Pro Team models, in order to provide greater integration capabilities and support to customers.

Digital health reimbursement is critical to unlocking greater access and driving accelerated adoption of digital health solutions across APAC. However, the road toward reimbursement can be long, especially in countries with poorly defined digital health regulatory, evaluation and reimbursement frameworks, requiring significant time and resource commitment from companies. Hence, when evaluating digital health opportunities in the region, companies need to ask themselves the following:

- Which markets are best suited to adopt our new digital health solution? Which markets should we prioritize?

- What are the registration and reimbursement frameworks that apply for digital health solutions? Which will be the most challenging hurdles for our solution to cross?

- What is the right strategy to navigate the various registration and reimbursement pathways across the APAC region? How can we move fast to demonstrate the value of our digital health solution?

- How do we monetize to maximize value before and after reimbursement? Which stakeholders are benefiting? Which are most willing to pay? How should we structure payment and pricing to drive adoption, support reimbursement and capture value?

- What are the partnerships that can speed up our path to scale, both before and after reimbursement?

- What market-shaping activities are required? What are the best return on investment activities for us, and over what time frame?

To explore these issues, APACMed and L.E.K. Consulting organized a panel discussion on Aug. 11, 2020, to discuss the study findings and gather panelist experiences on key learnings and watchouts in navigating the reimbursement landscape in APAC. The panelists also shared their recommendations on commercialization strategies, keeping in mind the need to build a sustainable business model. The key takeaways from the panel discussion included the following directives:

- Engage in dialogue early with key stakeholders and ensure that the value of the solution is clearly articulated. It is critical to begin a dialogue with key stakeholders early in order to develop a clear health economics value proposition that is substantiated by evidence in the relevant market. Companies need to take time to support a proper adoption process for their solution in order to understand payers’ willingness to pay and thereby optimize value. Given some digital health technologies can be very sophisticated, early dialogue will also help ensure clear articulation of value to all stakeholders through a mutually understood terminology.

- Identify true unmet need. Developing the technology itself may not be the hardest part; finding the right outcomes for the technology to demonstrate value and articulating true unmet need can prove to be more challenging. This is where dialoguing with payers, understanding incentives within the healthcare system and ensuring that the solution is bridging a true gap rather than offering a nice-to-have component will help companies identify and quantify the value of their technology.

- Manage stakeholder expectations with the future in mind. There is a tendency for companies to provide their solution either for free or for a minimal cost in order to rush the product into market to gather real-world evidence. As a result, an expectation of a free/low-cost digital health solution is set for both purchaser and provider, which then challenges the sustainability of the business model. It is important to first develop a plan that looks at the funding mechanisms before and after reimbursement, and manage expectations accordingly.

- Prioritize countries where reimbursement frameworks are in place and your digital health solution is valued. One way to look at the market is to understand whether your solution provides gains in value versus reduction in cost. Companies should prioritize where they provide gains in value as the ecosystem will help speed up both commercialization and reimbursement.

- Do not shy away from working with the private sector. Companies have the ability to play in a system that is mixed (private/public) with a fair amount of private insurance and private payers, as that allows them to have the runway they need to gather real-world evidence. This can be especially beneficial for startups, where market acceptance is key to getting both reimbursement and funding from investors.

- Find your cheerleader. To enable speed to market, it is critical to find the right credible partner who will also serve as your cheerleader and change-management champion. For example, medical societies are great partners, as they understand the incentives within the healthcare system, can generate real-world evidence and can be change champions.

- Respond to the changing and evolving healthcare landscape driven by the COVID-19 outbreak. The outbreak has served as a pivotal catalyst in improving acceptance and adoption of digital health technology, as seen by the tremendous regulatory and reimbursement acceleration for telemedicine and remote monitoring solutions following the outbreak. Companies should act now to engage more actively with key stakeholders and continue to drive the momentum of digital health acceptance and adoption.

In summary, the pathway to reimbursement is long and ever-changing, posing multiple challenges along the way. Despite this, many companies have successfully navigated and shaped the reimbursement landscape in APAC, achieving reimbursement in select countries. Examining how these companies have acted has provided many valuable lessons learned, synthesized into the nine best practices. This reimbursement framework along with the experiences and key learnings from the panelists offer a toolkit for startups, new entrants and existing players alike in effectively navigating the reimbursement landscape in APAC.

Endnotes

7 https://hfdc-corpweb.s3-us-west-2.amazonaws.com/assets/docs/HeartFlow-FFRct-Japan-Approval-FINAL1/HeartFlow-FFRct-Japan-Approval-FINAL1.html.

8 https://www.heartflow.com/newsroom/heartflow-receives-national-reimbursement-approval-in-japan/.

04292022080452