The increasing burden of mental illness has long been recognised as a serious and worsening world-wide problem, recently further exacerbated by the COVID-19 pandemic. Furthermore, current treatments are often unsatisfactory for many patients; they may work only partially or not at all, or have intolerable side-effect profiles. Against this backdrop, psychedelics have recently emerged as a potential solution to revolutionise mental healthcare and there continue to be significant and exciting developments in the sector.

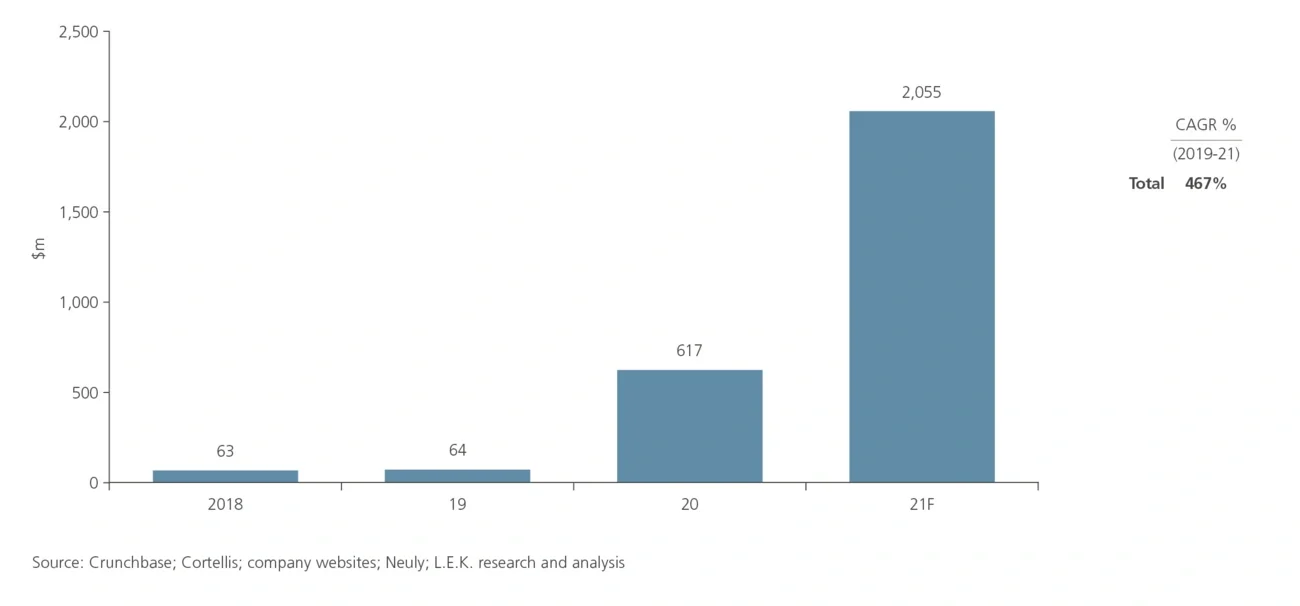

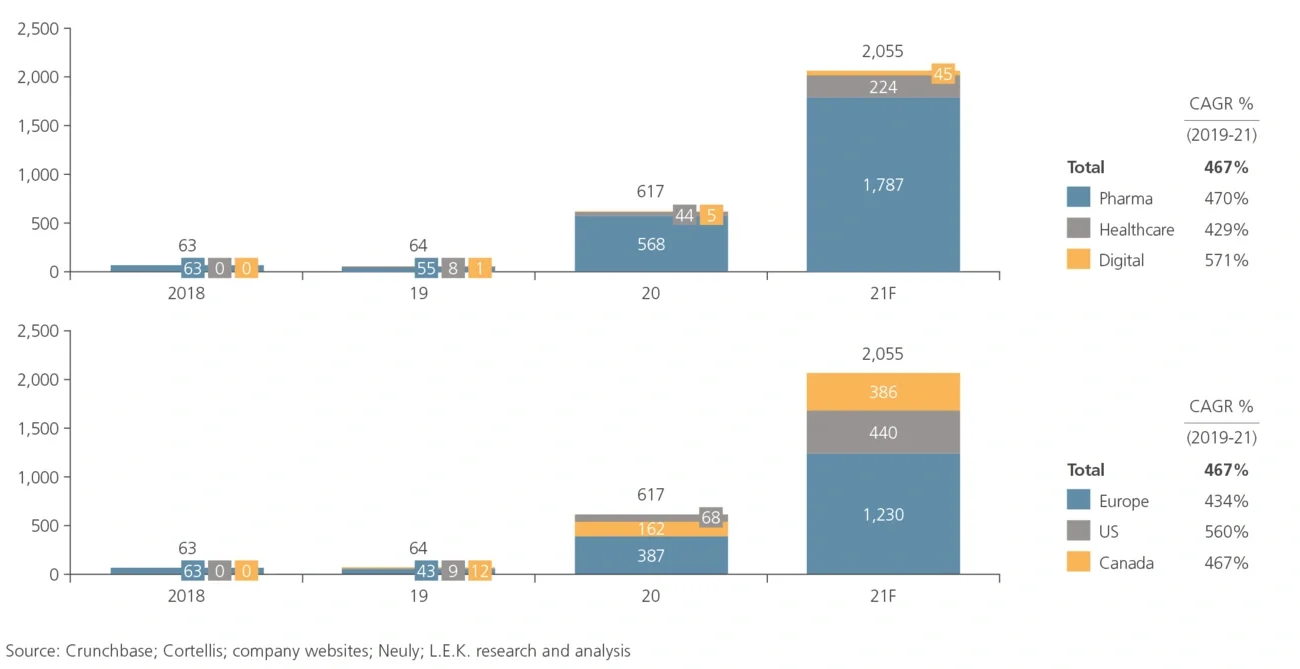

The recognition of the huge commercial opportunities to use psychedelics for mental illness has driven substantial investment in the sector in the past four years. 2020 saw a ramp-up of investment, and this accelerated in 2021 as investors hoped to tap into a potential multibillion-dollar market. Investors have been attracted by increasingly impressive scientific results, larger and more robust clinical trials, advances in establishing the legal therapeutic framework for psychedelics, growing public support for a serious change in mental healthcare, and the establishment of the infrastructure to deliver psychedelic-assisted psychotherapies.

Despite the influx of funding, there has been little published analysis of investments entering the psychedelic space. We analysed over 110 financing events from more than 60 companies working primarily within the psychedelic sector between 2018 and 2021. These companies included pharmaceutical businesses focused on discovering, developing, and manufacturing psychedelic drugs; healthcare companies establishing clinic networks and retreats for psychedelic-assisted psychotherapy; and technology companies producing telehealth platforms and electronic health record software specifically for medical practices using psychedelics. To supplement this analysis, we conducted a range of interviews with leading investors and businesses in the space.