There are some positive factors to consider

Both here and overseas, green hydrogen seems to have some current factors and future potentials in its favour. For some industries in particular — fertiliser and ammonia production, and steel manufacturing — it becomes the most likely or indeed only solution as an alternative to ‘traditional’ hydrogen sources.

The United States Department of Energy forecasts that the global green hydrogen market is expected to grow, with the cost of green hydrogen production falling from $6 per kilogram in 2015 to $2 per kilogram or lower by 2025. Countries like Japan and South Korea are also pursuing hydrogen as a policy priority.

Supporting this, the Institute for Energy Economics and Financial Analysis (IEEFA) in January 2021 also predicted the price of green hydrogen will drop 70% in the next decade in regions with cheap renewables, such as the Middle East or the Pilbara in Western Australia with its access to cheap green energy sources like abundant daytime solar power.2

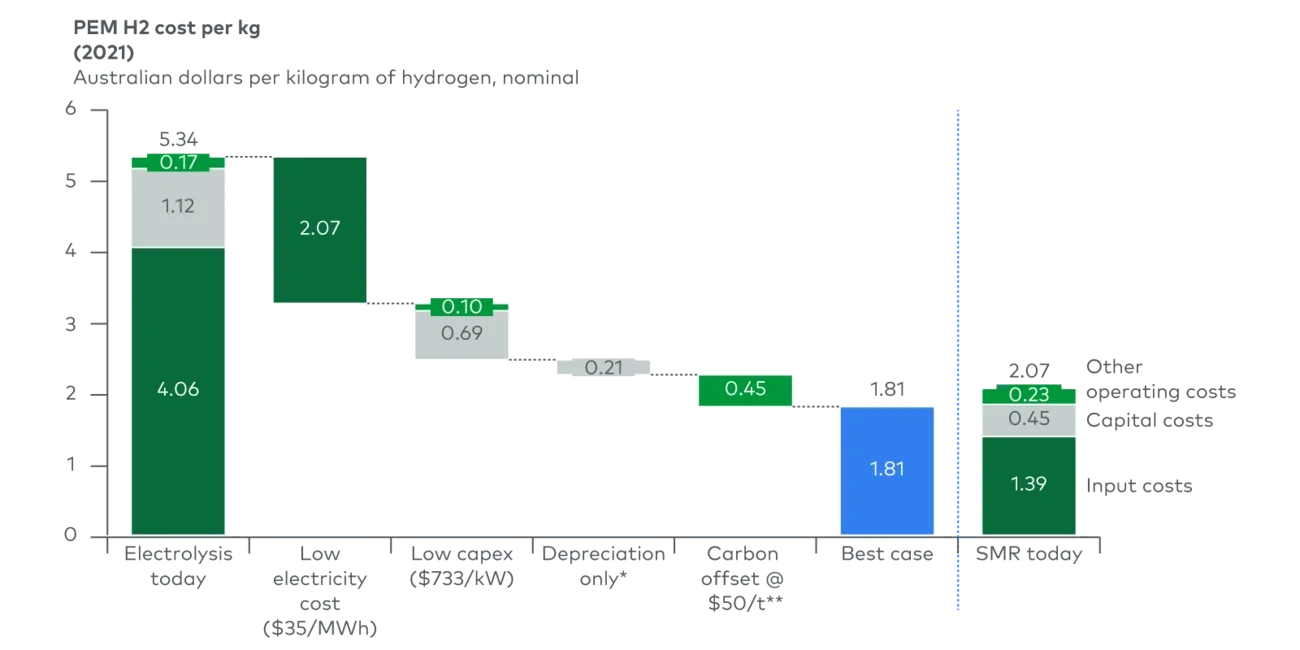

In east coast Australia, green hydrogen today costs twice as much as conventional grey hydrogen, but a 2020 Australian National University report estimated that Australia could be producing it for much cheaper, even currently, and it could equal the price of conventional hydrogen by 2030.

The CSIRO’s 2018 National Hydrogen Roadmap report also suggests there is an opportunity for Australia to export green hydrogen to energy-hungry countries that do not have access to cheap renewable energy. It estimated potential demand for imported hydrogen in China, Japan, South Korea and Singapore could reach AU$9.5 billion by 2030. These nations all have stated hydrogen commitments that have the potential to be serviced by Australian-produced hydrogen:

-

South Korea, which has targeted approximately three million fuel cell vehicles (FCVs) to be in operation by 2040, supported by a US$1.8 billion fund to invest in hydrogen

-

Japan, which has a projected demand of 300 kilotonnes of hydrogen per annum until 2030, with the hydrogen to power approximately 800,000 FCVs and fuel 5.3 million stationary fuel cells in households

-

China, which has stated a hydrogen FCV road map with a target of approximately one million FCVs operating, with at least 50% hydrogen-powered by 2030

-

Singapore, which is currently exploring a national hydrogen strategy to replace national emissions by around 60%, predominantly through replacing existing liquid natural gas (LNG) with hydrogen

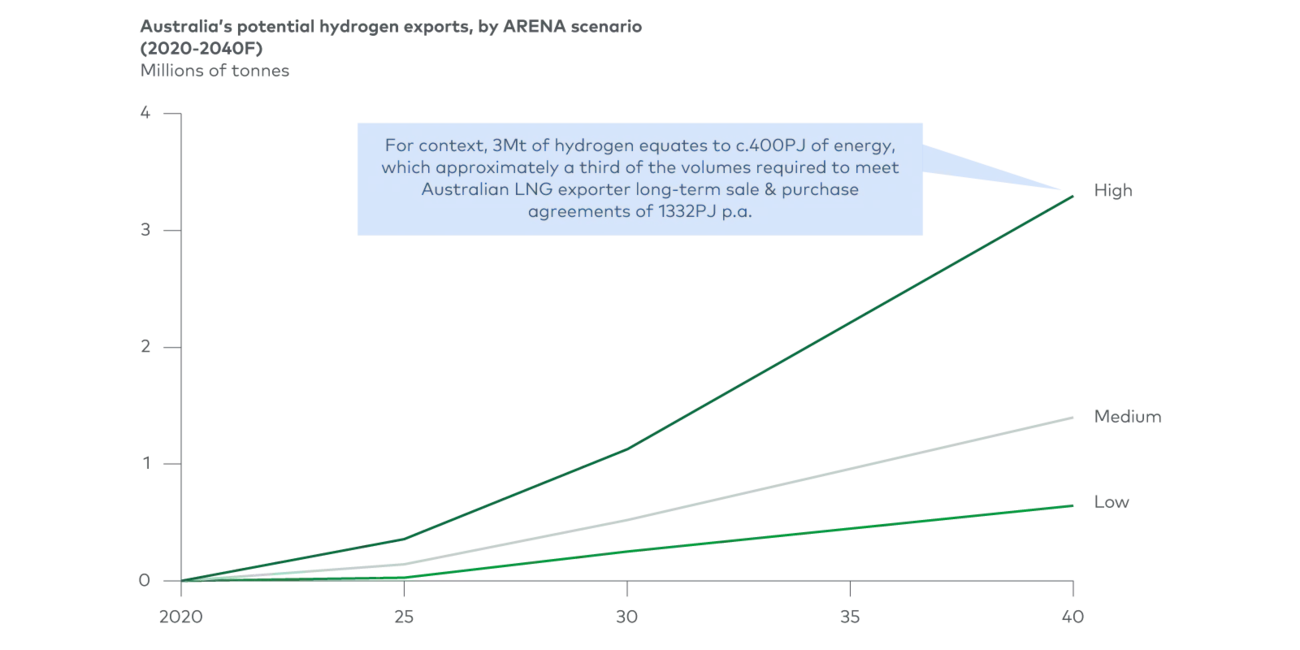

ARENA estimates of Australian hydrogen export volumes (see Figure 4) show the significant size of this opportunity for Australia. To put this approximately three million tonnes of hydrogen into perspective, it is broadly equivalent to a third of the energy exported today by Australia’s LNG industry.