Embedded finance is powering on across industries, and the party is just getting started. Five short years ago, most customers would engage digitally with financial services only if they were early adopters and weren’t associated with a traditional bank (talking to you, fintechs). The pandemic triggered a shift in customer behavior, most notably by the sudden adoption of contactless payments. Embedded finance isn’t a new concept, but it’s currently experiencing a major surge that shows little sign of slowing. Buckle up, expect some turbulence and prepare for the accelerated innovation of embedded finance (see Figure 1).

Executive Insights

The Embedded Finance Revolution: Fast, Furious and Just Beginning

The Embedded Finance Revolution: Fast, Furious and Just Beginning

November 21, 2024

Key Takeaways

Embedded finance has evolved from a niche concept to a transformative force, driven by the pandemic's surge in digital and contactless payment adoption.

The market is set for rapid growth, projected to increase at a 21.3% CAGR from $82.7 billion in 2023 to $240 billion by 2033.

Regulatory changes are reshaping competition and driving greater transparency and security.

Success in embedded finance requires financial services institutions and brands to build trust, leverage insights and create seamless customer experiences.

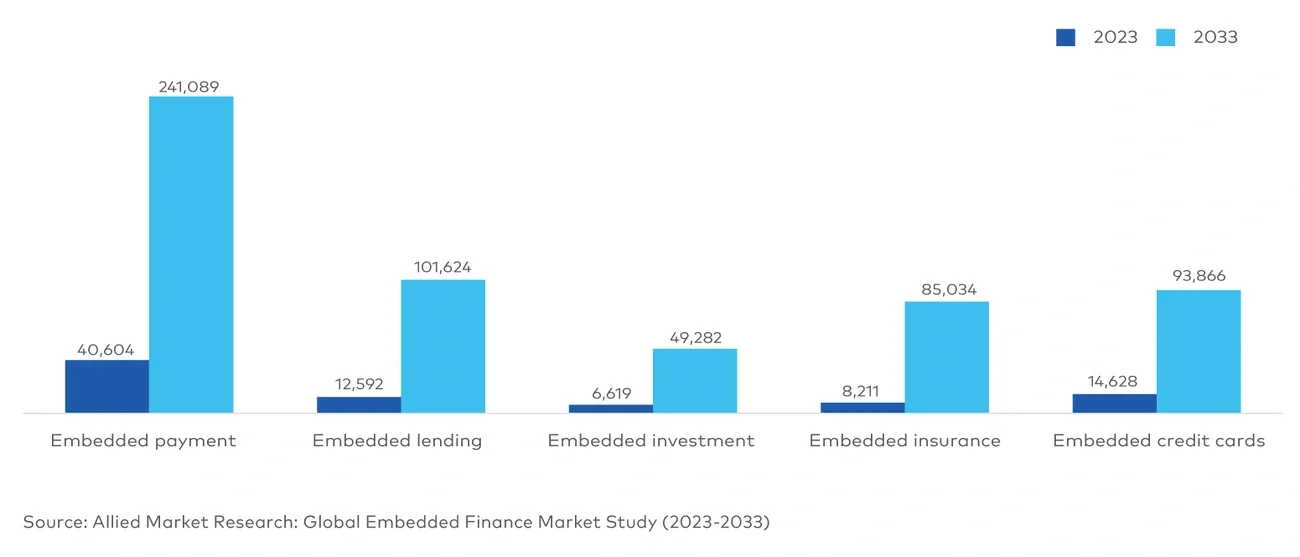

Figure 1

Embedded finance market, by type, 2023-2033 ($million)

Image

Embedded finance has a solid foothold in financial services sectors, but the convergence of shifting customer behaviors and advancing technology signals an even more promising path for growth. The global embedded finance market size was estimated at US$82.7 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 21.3% from 2023 to 2033. Customers increasingly desire financial services propositions (lend, finance, lease) seamlessly embedded into an interconnected customer journey.

This customer desire has been fueled by increased digitization, enhanced speed (5G), cloud technology and application programming interfaces. As this demand for a seamless experience intensifies, new distribution channels and propositions, coupled with technologies such as quantum computing, generative artificial intelligence (AI), Web3, blockchain, digital assets and others, will only amplify the potential innovation. For example, programmable on-chain payments can be executed when specific parameters are met, detected by AI and transacted on a customer’s behalf. Nuances like this will become the expected norm for customers as embedded finance continues to take hold.

“The evolving regulatory landscape — particularly around capital — is driving banks to find new profit centers, nonbanks are looking for new revenue streams as funding costs pressure companies to do more with less (e.g., drive higher customer lifetime value with already absorbed customer acquisition costs), and customers of all shapes are looking for more integrated and efficient ways to run their finances in an increasingly complex and expensive world.”

— John Piazza, head of product for Newline, Fifth Third Bank’s embedded finance business

“Banks are beginning to recognize the immense potential of embedded finance by embracing customer orientation, verticalization and personalization. These factors are key to delivering unique, integrated and nearly invisible financial experiences that seamlessly fit into the customer journey. The future of finance lies not just within banks but also in nonfinancial services distribution, where embedding financial products into everyday platforms can create powerful new value streams and drive deeper customer engagement.”

— Aaron Byrne, financial services and fintech practice leader, L.E.K. Consulting

As the sector evolves, embedded financial and nonfinancial players will operate in an increasingly sophisticated marketplace. Understanding the expected market shifts and opportunities is crucial to devising a strategy to capture market share and foster customer loyalty.

New market players + evolving regulations = opportunity

As technology lowers the barrier to entry, more business-to-business and business-to-consumer organizations will offer new embedded finance propositions to their customers, gig workers and contractors. In some industries, this is likely to happen sooner rather than later. Social media platforms continue to explore and adapt their value propositions and build stronger relationships by creating multifaceted hubs that blend experience, commerce and financing.

Additionally, open finance will make it easier for financial and nonfinancial institutions to engage with customers and offer personalized propositions based on insights gleaned from data. Conversations about customer ownership of personal data and digital identity will be crucial here. All institutions will need sound risk management capabilities to avoid data breaches and fraudulent activity and maintain customer trust. These trends may reshape how customers conduct daily financial transactions, with each step becoming more seamless and invisible (think Apple).

“Businesses’ expectations have fundamentally changed: Operators want banking at the point of need, and increasingly that is in their enterprise resource planning software, point-of-sale platforms or other tailored workflow systems. This inevitable shift benefits business operators, software platforms and banks — all by increasing efficiencies and opening new ways to add value for customers.”

— John Piazza, Fifth Third Bank

The emergence of nontraditional players also introduces the risk of multiple accounts. This contradicts the essence of embedded finance — convenience and ease — potentially sparking another landscape shift. Customers will not wish to bank with every brand or institution they have a relationship with. Instead, the most prominent brands will likely win, and consolidation will likely follow. This environment is akin to the proliferation of digital entertainment platforms, which has resulted in consumers exploring rebundling options. Whether the winning brands will offer the best services or integrate to create a better customer experience remains to be seen.

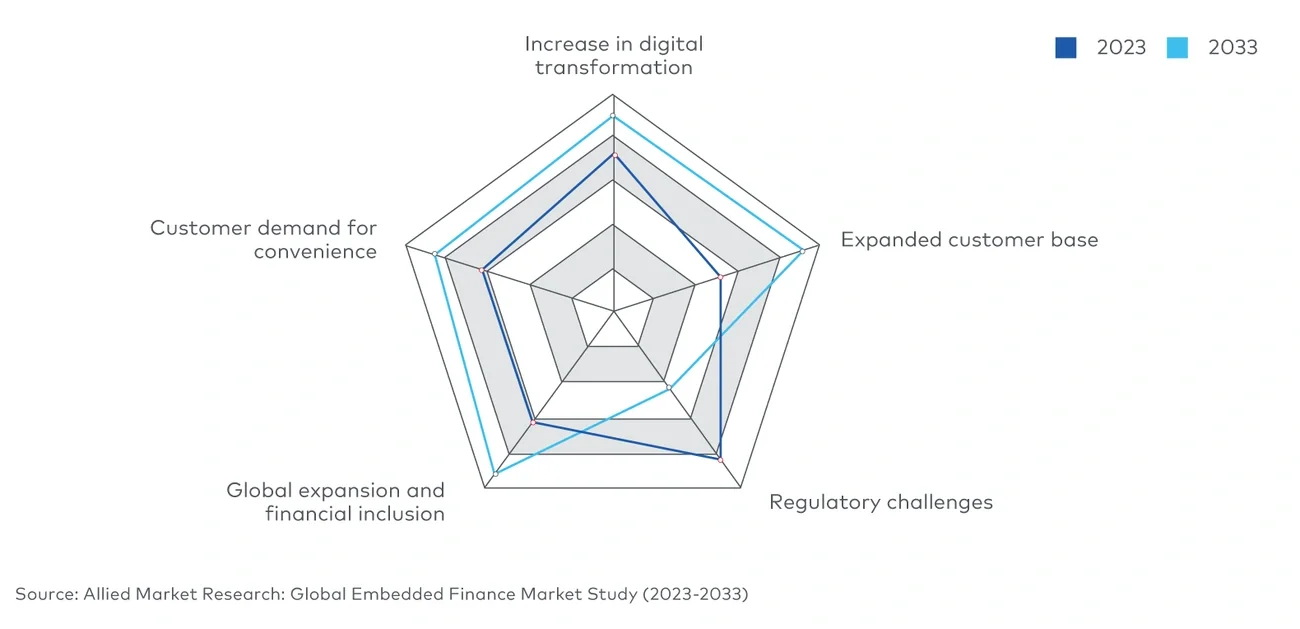

The new regulations will also have an impact on aggregation. In the U.S., the Consumer Financial Protection Bureau’s (CFPB) finalized Section 10332 rule mandates that financial institutions provide consumers and authorized third parties with access to personal financial data, including transaction details and pricing information such as annual percentage rates and fees (see Figure 2).

Figure 2

Top impacting factors in embedded finance market (2023-2033)

Image

This regulation aims to enhance transparency and competition in the financial sector. Additionally, the CFPB has proposed expanding its supervisory authority to include large technology companies offering digital wallets and payment applications, subjecting them to examination processes like the ones they use with banks. This initiative focuses on the use of sensitive personal data and addresses concerns about competition and innovation in mobile payments.

“The contextualization of financial services into the ecosystems where customers operate is increasingly important and presents a significant opportunity for banks to differentiate. Embedded finance, accelerated by open banking, offers banks a way to meet customers where they are, with solutions delivered right at their point of need through the platforms where customers spend time. And it compels banks to think differently about customer acquisition and product distribution.”

— Eric McCabe, head of embedded finance, Citizens Bank

Succeeding in the new frontier

Four key factors will define success in this new landscape: trust, insight, convenience and speed. This means scaling and competing against a broader set of competitors for traditional banks. Banking leaders must determine where their institutions best fit within the embedded finance ecosystem, whether this role is as an ecosystem aggregator, owning the enabling platform and related technology, customer distribution channels, and orchestrating products; or acting as an enabler to extend its products and services through a platform business model. Crucially, banks must resolve legacy technology challenges that have impeded growth.

Maximizing the benefits of advanced technologies is crucial, but banks must also skillfully balance the demands of structured, regulated propositions with the uncertainties of new capabilities. Banks committed to scaling up their risk and compliance function to meet new regulatory demands, while building regulator trust, will start to gain a competitive advantage. As regulations expand, brands seek banks that can safeguard their interests while supporting their growth ambitions.

“Embedded finance is banking. As we head into the next inning of embedded finance adoption, we will see more banks, non-banks, and fintech platforms look for ways to deliver integrated and unique experiences to their end users. Incumbent players, with their long-standing bank relationships and compliance expertise, are uniquely positioned to enable their ecosystems to drive adoption at scale.”

— Roy Andrew Ng, EVP, Chief Business Officer, Platform and Enterprise Products at FIS

Traditional banks can no longer rely on substantial deposits to guarantee future success and must evolve. As embedded finance becomes the norm rather than a niche, huge opportunities await organizations that build closer customer relationships and offer a superior experience. Banks are investing heavily in digital and customer experience, extending themselves into new profit pools across the value chain. Their focus has shifted to working with brands (retail/CPG/platforms) to strengthen their customer affinity and make a concerted effort to increase the perception of the value they can offer in today’s evolving banking landscape. Comparatively, brands and retailers garner their customers’ affinity and trust, which is paramount in their position and decision-making as they evaluate how to partner and mobilize embedded offerings.

Without trust, insight, convenience and speed, institutions will fail to deliver the change that’s coming and make their mark in this exciting new landscape.

To help ensure your organization is in the best position, please contact us to discover how L.E.K. Consulting can help your organization navigate the embedded finance ecosystem.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC

Questions about our latest thinking?

Questions about our latest thinking?

Related insights

You might also be interested in these insights.

English