COVID-19’s impact is first and foremost a humanitarian crisis that has thrown us into uncharted territory. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this crisis.

Key takeaways

- We conducted more than 30 discussions with C-suite executives during March and April, focusing on four key questions related to the impact of COVID-19 on packaging.

- Across March and April, packaging converters were affected differently based on three societal impacts: work from home, business restrictions, and health and hygiene.

- Four thematic operational challenges emerged across packaging end markets: employee safety, supply chain management, absenteeism and the need to adapt production to demand fluctuations.

- In the face of these challenges, five new normals are expected to develop after the virus moderates, with wide-ranging implications for converters.

COVID-19 has upended the operations of companies around the globe, and within packaging, it has had a highly variable commercial impact on converters based on the relative end-market focus of each company, with some demand pockets surging and other demand pockets softening (see Figure 1). In addition to disrupting company operations in the near term (i.e., March and April), COVID-19 is expected to create a series of “new normals” within packaging in the medium to long term (i.e., the second half of 2020 and beyond).

To better assess the near-term commercial impact and new normals as well as to understand both the operational impacts and management learnings gained thus far from the crisis, we conducted 30+ discussions with C-suite executives during March and April. This Executive Insights represents a high-level summary of those in-depth discussions, which were focused on four key questions:

- What near-term commercial impact has COVID-19 had on your packaging formats, substrates and end markets?

- What operational impact has COVID-19 had on your supply chain, manufacturing/production facilities and employees?

- To what extent do you expect to see a new normal in packaging demand following COVID-19? If so, in what area?

- What are the key leadership lessons and best practices learned in order to successfully navigate through the COVID-19 crisis?

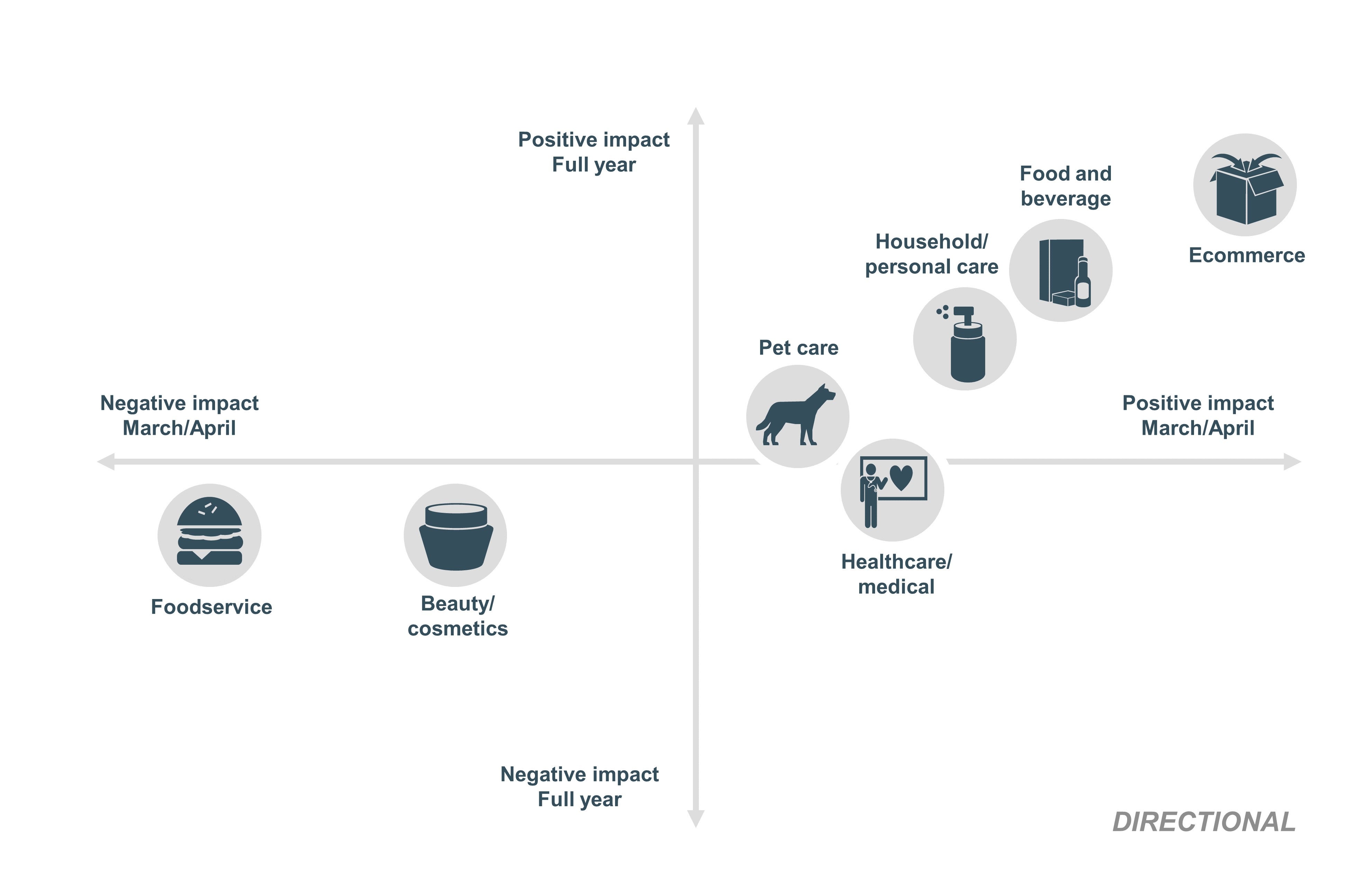

Figure 1

March/April and full-year 2020 impacts of COVID-19 relative to pre-COVID-19 baselines, by end market

Commercial impact

Across March and April, packaging converters were differentially affected based on their end-market exposure. While certain interviewees reported cutting shifts and furloughing some employees due to demand softness, others noted that they had added capacity, mostly by adding shifts, and were operating close to 24/7 to meet surging customer demand (see Figure 2). These differential impacts were driven by three key societal dynamics during COVID-19:

- The transition to work from home for millions led to surging demand for products such as protective packaging in ecommerce as Americans expanded home office capabilities, but led to softening demand for products such as color cosmetic packaging and bottles for nonalcoholic beverages, which are frequently purchased “on the go” by commuters.

- Business restrictions have affected a range of end markets, but their impact has been felt particularly acutely across on-premises foodservice (excluding foodservice takeout/delivery packaging formats). Given foodservice closures and the corresponding shift to “at home” dining, demand for food and beverage packaging has surged across most end-market packaging categories (e.g., protein). While a portion of this was due to stockpiling, elevated demand is expected to persist until foodservice transaction volume approaches pre-COVID-19 levels.

- Finally, an increased focus on health and hygiene has driven increased sales volume for cleaning products and hand sanitizers, creating surge demand for rigid plastic converters. Additionally, as consumers have emphasized social distancing and personal safety, they have increased their ecommerce purchases in lieu of visiting stores, creating incremental demand for cardboard packaging, flexible pouches and protective packaging.

Operational impact

During our C-suite discussions, four thematic operational challenges emerged across packaging end markets: employee safety, supply chain management, absenteeism and the need to adapt production to demand fluctuations.

- Above all factors, employee safety has been top of mind for leaders in the packaging industry. Tactics have included mandating personal protective equipment (PPE) usage, transitioning nonproduction teams to work from home, reducing employee count during shifts to enable social distancing, tasking employees with disinfecting facilities throughout ongoing operations and immediately sending home employees who feel sick (and paying them through the end of their shift).

- While actual disruptions have been low, executives regularly report concern surrounding supply chain management, including difficulties crossing international borders in Europe, New York-related delays in the U.S., and challenges procuring service technicians to maximize equipment uptime.

- Converters report increases in employee absenteeism due to COVID-19 and have implemented hazard pay (typically about $2 more per hour) as a mitigation tactic; interestingly, converters report absorbing the margin impact instead of passing it on to customers.

- Last, given demand disruptions, many converters have noted the need to adapt production to meet new levels of demand. For those experiencing surges, tactics have included rationalizing stock-keeping units (SKUs), adding incremental molding and hiring temporary staff; however, those experiencing softer demand have been forced to furlough employees, reduce shifts and, in the case of a converter producing protective packaging for automotive, selectively shutter production.

New normals

In the face of these challenges and given the massive impact that COVID-19 is having on how almost all Americans live their lives, five new normals are expected to develop after the virus moderates, with wide-ranging implications for converters.

- The most critical new normal is expected to be a permanent step-change acceleration in ecommerce adoption. As millions of new consumers experience the convenience (and safety) of buying online, a significant subset are expected to “stick,” elevating ecommerce volume and driving incremental demand for protective packaging, flexible pouches and corrugated board. In particular, we expect substantial ecommerce penetration gains in grocery retail, which has historically had relatively low levels of online penetration as compared with other categories (e.g., apparel, electronics). We expect brand owners will place increased importance on packaging formats and substrates that protect the product through online grocery fulfillment channels.

- Interviewees broadly expect to see higher volumes of packaging used, particularly within the grocery store. Previously unpackaged items (e.g., loose produce) are expected to be packaged more frequently in the future. Additionally, certain items that were packaged by consumers in flexible bags, such as pay-by-the-pound nuts and grains, are now being prepackaged in rigid plastic containers. This dynamic is expected to drive demand to both flexible and rigid converters serving the grocery store.

- Additionally, demand for tamper-evident packaging is growing as packaging customers (e.g., grocers, food processors) utilize more of it within their operations to ensure food safety for U.S. consumers. This is expected to drive demand for tamper-resistant solutions such as stickers and shrink bands as well as more complete packaging solutions (e.g., tear-away); these complete solutions are patent protected and increased demand is likely to benefit a select subset of converters holding these patents.

- Corporate focus on sustainability initiatives is expected to be relatively muted through 2020 (as compared with 2018-19) as brand owners and regulators prioritize health and safety above sustainability goals. For instance, despite leading nationally on many sustainability standards (e.g., fuel economy), California announced on April 23 that it would permit the usage of single-use disposable plastic bags in the grocery store for at least the subsequent 60 days. That said, in looking beyond 2020, the degree of focus on sustainability initiatives is expected to return to pre-COVID-19 levels. This can be largely attributed to strong underlying consumer sentiment and publicly stated 2025 or 2030 sustainability goals that we do not expect brand owners to abandon.

- Finally, elevated usage of personal hygiene products such as hand sanitizers and wet wipes is expected to persist following COVID-19, as U.S. consumers continue to expect access to these products in the public domain and as businesses and workplaces provide these products to their employees and customers. This dynamic is expected to drive demand for bottles, closures and dispensers.

Leadership lessons

As management teams have navigated the crisis, four primary learning opportunities have emerged. First and foremost, communication has been and continues to be a critical tool in maintaining employee morale and limiting absenteeism. Converters have used communication tools ranging from digital apps to handwritten letters, with the aims of creating transparency, emphasizing a sense of purpose to employees around the essential nature of their work and sharing best practices across the organization. Executives have broadly reported successfully adapting to working remotely, and a subset expect remote working to become more common post-COVID-19, including a potential review of the commercial office space footprint that is truly required. Finally, converters report weighing the benefits from potentially revising their commercial strategies following COVID-19 with the aim of generating near- and long-term revenue opportunities through additional capacity, repurposing assets to support COVID-19 relief (e.g., manufacturing PPE), and adapting business development activities to a more virtual world.

If you would like to learn more or request access to the full Packaging C-Suite Roundtable report, please contact us at industrials@lek.com.

01032023160138