Key takeaways

-

Legacy brands can form the foundation of a successful business, particularly for specialized players — companies that build portfolios by acquiring legacy brands can then use them as a platform for further growth.

-

Three main factors influence whether a legacy brand has the potential to be a successful long-term cash generator: established brand equity, ongoing demand and barriers to entry.

-

Focused players have several layers available that may allow them to extract greater value from legacy brands than larger pharmaceutical companies.

-

The success of focused players relies on three key features: M&A as a core competency, corporate focus on core functions, connection to the market.

Legacy brands can form the foundation of a successful business, particularly for specialized players with the appropriate organizational structure and the right operating model to realize their potential.

Companies that build portfolios by acquiring unloved brands from their original owners can then use them as a platform for further growth, either along the value chain or to establish themselves as a specialty pharma company.

What are legacy brands?

Legacy brands are originator (or innovator) products whose patents expired some time ago but that still generate non-negligible revenues for their owners, despite being a far cry from their peak revenues when protected by patent. For example, U.S. sales of Eisai’s Zonegran (sold to Advanz Pharma) and AstraZeneca’s Zoladex (sold to TerSera) were both approximately $70 million in 2017, and sales of Pfizer’s Protonix were approximately $115 million. Smaller legacy brands, such as Pfizer’s Xalatan, BMS’s Plavix and Boehringer Ingelheim’s Micardis, continue to bring in about $15 million to $50 million each in U.S. sales.

These brands typically retain a modest but stable residual market share due to their brand equity, distinguishing them from branded (or unbranded) generics that may enter the market following patent expiry. Given the high degree of generic prescribing in the U.S. (approximately 90% of all prescriptions are for generics) and the use of preferential tiering on payer formularies to encourage patients to prefer unbranded generics due to lower copays, legacy brands typically only receive about a 1%-5% share of prescriptions for the molecule (based on our analysis of 12 brands). However, they often maintain pricing at a level above that of unbranded generics and more in line with their pricing prior to loss of exclusivity, and therefore have a higher share of the total molecule value and a higher gross margin than generics.

As large pharma companies look to maximize shareholder returns by focusing on the development and marketing of innovative therapies and raise cash by divesting noncore assets, legacy brands become attractive acquisition targets for specialized players.

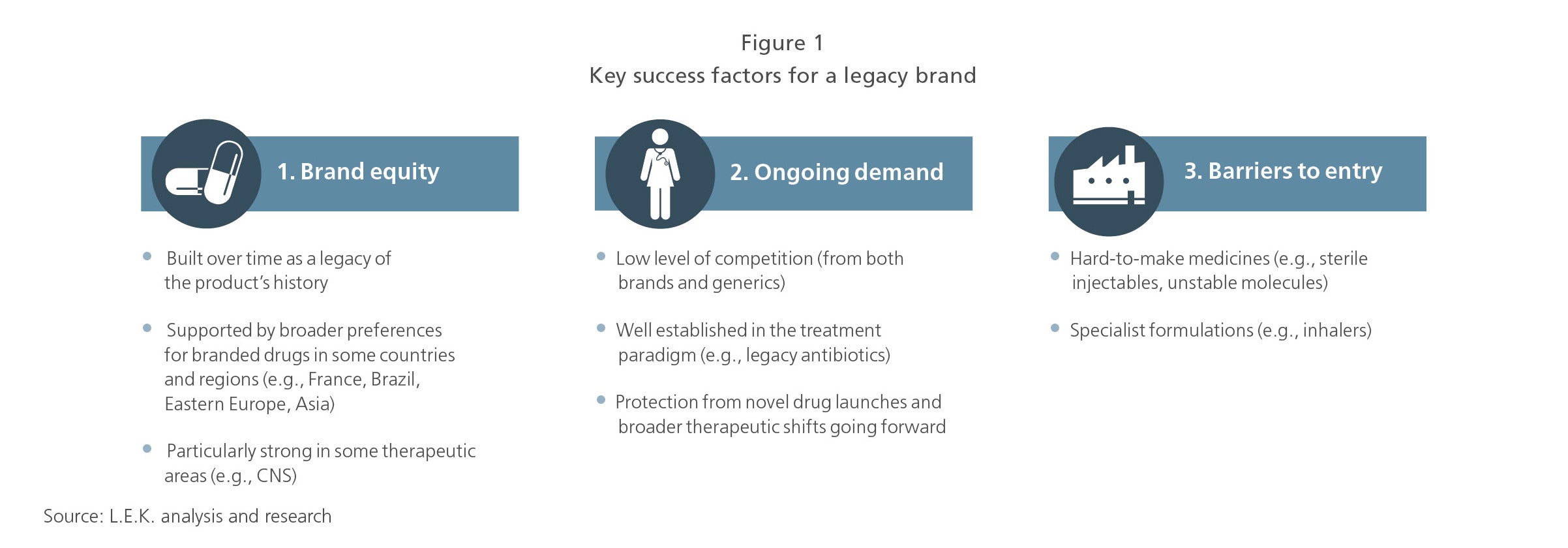

Key success factors for legacy brands

Three main factors influence whether a legacy brand has the potential to be a successful long-term cash generator (see Figure 1).

A would-be acquirer needs to consider each of these factors carefully in the due diligence process.

- Having established brand equity is critical, in terms of both patient demand and physician prescribing habits. Strong brand equity means that limited sales and marketing efforts are required due to the long-established presence of the brand in the market. In our experience, sales and marketing spend would typically be less than 5% of sales even in promotionally sensitive markets.

- Ongoing demand is required to prevent further erosion of market share, e.g., from new innovator products changing the treatment landscape.

- Finally, participation in a market with particularly high barriers to entry can reduce the impact of generic competition.

The benefit of focus

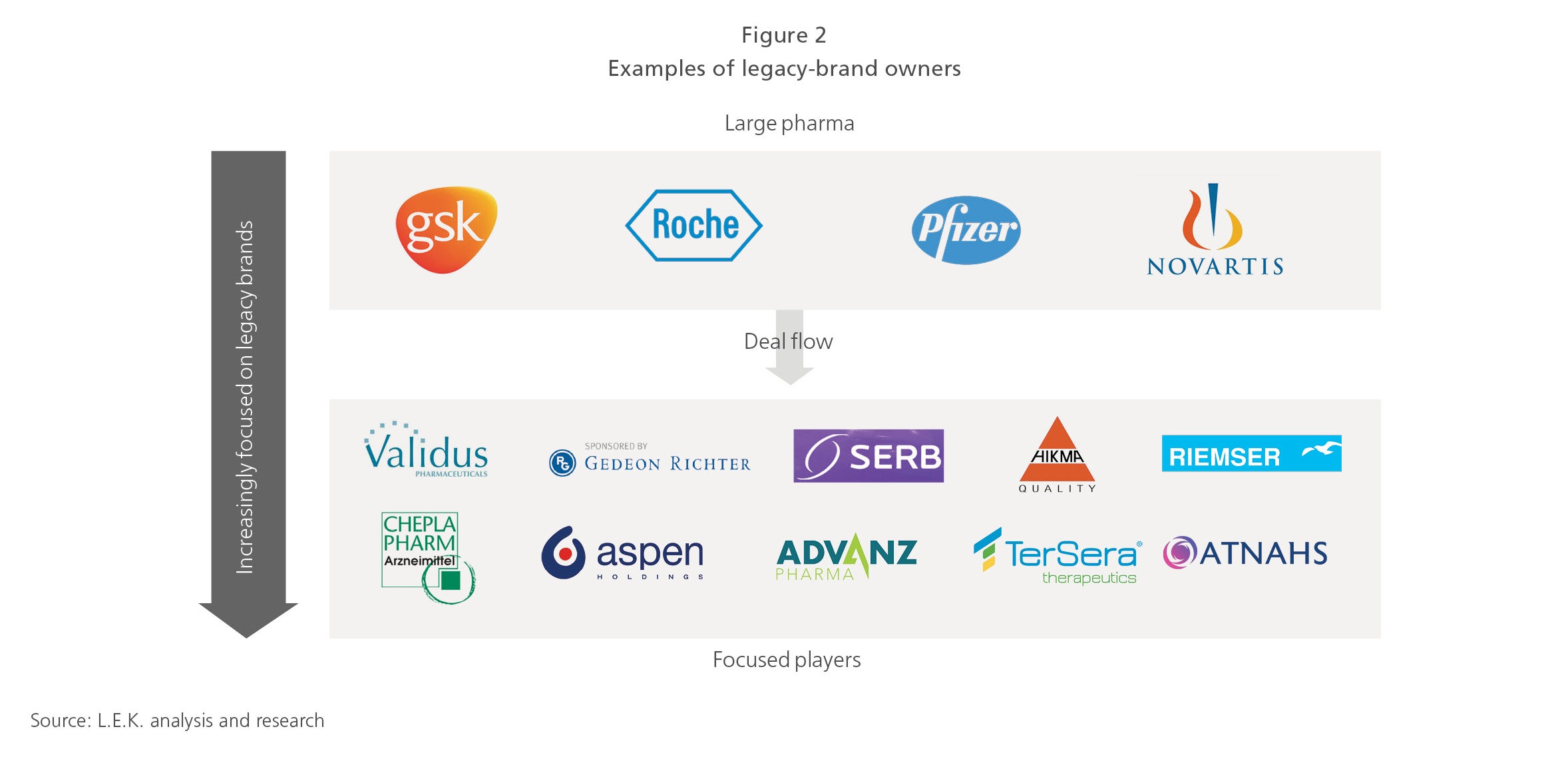

The owners of legacy brands differ, ranging from large pharma companies to more focused specialty companies that benefit from the flow of off-patent brands divested by large pharma companies and that seek off-patent asset acquisitions and build businesses around them (see Figure 2).

These focused players have several levers available that may allow them to extract greater value from legacy brands than their larger pharmaceutical counterparts could.

Legacy brands typically represent a small portion of a large pharma company’s portfolio, and often do not receive the full, albeit minor, sales and marketing efforts required to drive brand awareness and increase sales. A focused player can revitalize a brand by modestly increasing sales and marketing.

Furthermore, optimization of pricing on a country-by-country basis and in light of the latest market changes (e.g., new product launches) can allow the new owner to extract additional value in a way that a larger pharmaceutical player cannot (e.g., due to portfolio considerations). Pricing strategies should reflect the drug’s value and therefore remain defendable to avoid reputational damage.

Legacy brands still produced in-house by large pharma companies may have high costs along the value chain, from active pharmaceutical ingredient to finished product, and may depend on older or suboptimal manufacturing sites. There is often opportunity to reduce costs by outsourcing or optimizing various value chain steps.

Finally, successful companies in this space typically look to extract additional value from an acquired asset through increased geographic coverage, line extensions and/or life cycle management (e.g., new formulations).

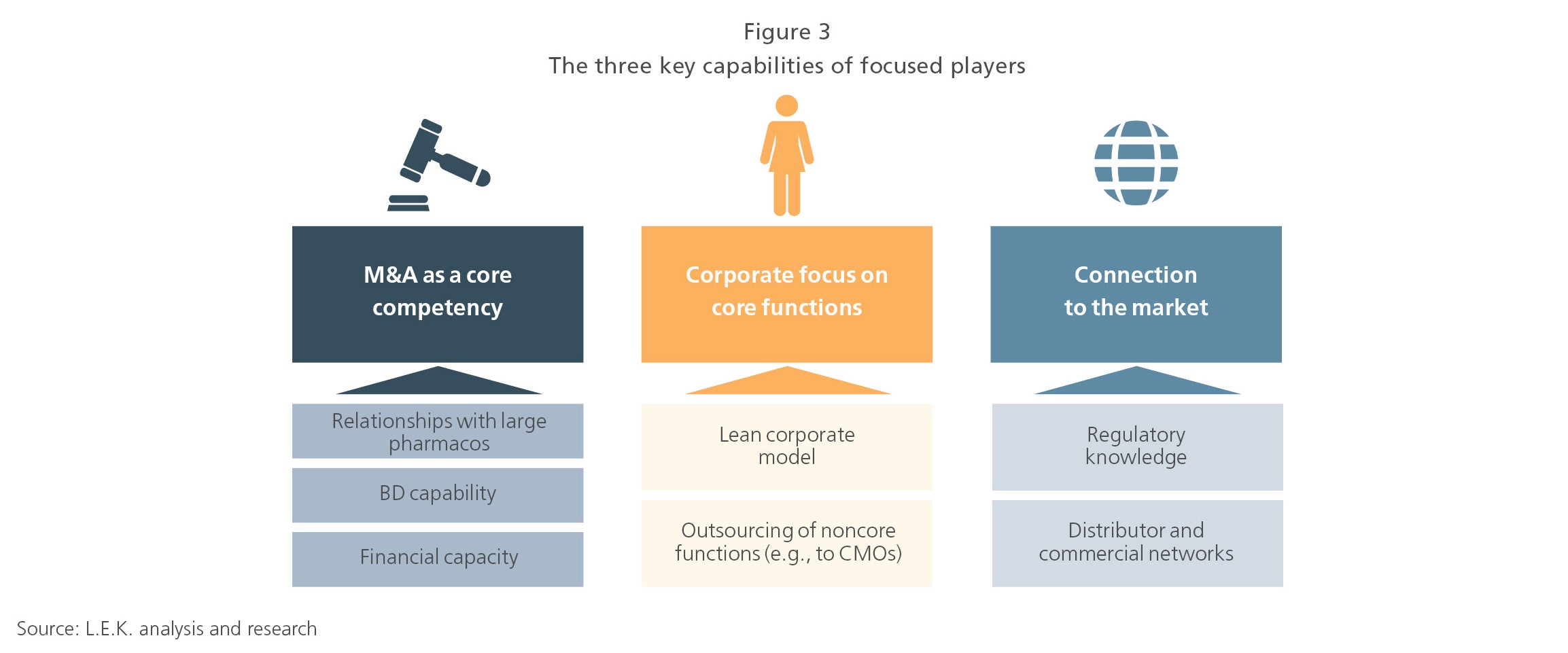

How companies can build successful businesses around legacy brands

The success of focused players relies on three key features (see Figure 3).

- M&A as a core competency. Being highly competent in M&A requires established relationships with large pharma companies for deal flow, business development capabilities or external support to pursue and negotiate transactions, and the financial support to close deals.

- Corporate focus on core functions. An asset-light lean structure maximizes margins, with only core functions such as executive management, business development and supplier/partner management kept in-house. Manufacturing tends to be outsourced to contract manufacturing organizations, as is sales and marketing via distributors or contract sales forces as required.

- Connection to the market. Companies should be highly connected to the market in order to be able to respond to opportunities through in-depth regulatory knowledge (e.g., to accelerate transition of acquired marketing authorizations), and by leveraging key distributor and wholesaler relationships in order to provide a robust supply chain and to launch in new geographies.

Given the requirements for success, it is imperative that focused players have the appropriate executive/management team in place with the right capabilities and connections (i.e., with pharma, CMOs, external advisors, banks, and private equity or other investors) required to maintain deal flow and build the business. As portfolios grow, success is also driven by a greater strategic focus, allowing companies to compete more effectively in M&A and realize synergies in the portfolio.

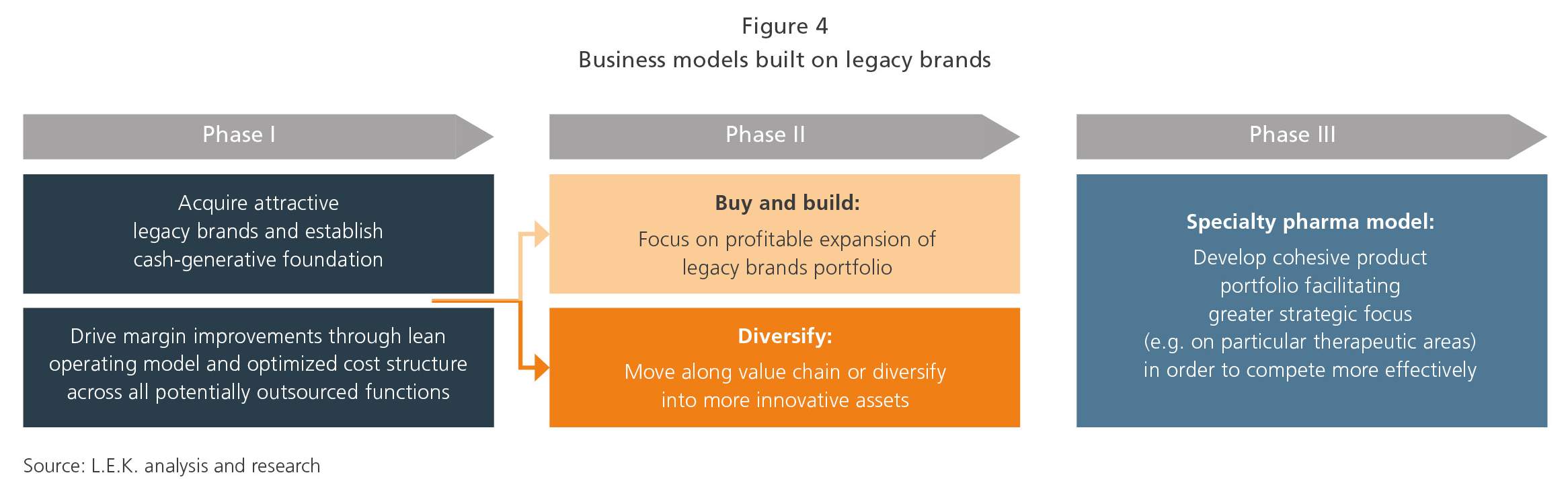

Legacy brands as the basis of long-term business models

Leveraging these key capabilities, companies have successfully built portfolios around legacy brands (see Figure 4). In the longer term, they can keep following a buy-and-build strategy or look to diversify their business model. For example, they can move along the value chain (e.g., through development of their own sales and marketing capabilities) or can look to expand into more innovative areas (e.g., by using generated cash for innovative product R&D or life cycle management). One example of such a transition is EUSA Pharma, which started around a portfolio of legacy products acquired from Jazz Pharmaceuticals and has since focused on targeted acquisitions for innovator brands still under patent protection (i.e., moving away from legacy brands) to build a business around oncology and rare diseases. Another is SERB, which has built a cohesive emergency care, endocrinology and neurology portfolio through 16 acquisitions over the past 12 years.

These businesses have the potential to be very attractive from a financial perspective. Operational efficiencies (e.g., through outsourcing and synergies) can lead to attractive margins, with some companies reporting >50% EBITDA margins.

Legacy brands also offer significant scalability to support growth via addition of other products or expansion into new geographies, and provide a cash-generative foundation that can be used as a platform for further bolt-on acquisitions or to facilitate a transition into more of a “specialty pharma” model as and when the portfolio coalesces around particular therapeutic areas.

Given their financial attractiveness (high cash flow and low clinical risk), legacy brand businesses have garnered a high degree of interest from private equity, with several recent transactions backing focused players. For example, in June 2017, Charterhouse invested in SERB, which had grown from €3 million sales in 2001 to €65 million in 2016, and in 2019 funds advised by Triton acquired a majority stake in Atnahs.

Legacy brands, and the companies that have focused on building portfolios around them, have the potential to be attractive opportunities for immediately cash-generative acquisitions that are ripe for value creation through operational improvements, or as a foundation for a more diversified business.

When contemplating acquisition of a legacy-brand product or company, potential acquirers should take care to assess not only the current positioning of the products themselves, but also the management team and the ability of the company to create value from the brands and to construct a cohesive portfolio around them.

01022024150138