Traditionally, BPC products have been more about pampering than paring back. But concerns about the industry’s environmental impact are prompting more consumers to factor sustainability into their product selections. What does that mean for the BPC industry? To find out, let’s look at the issues involved and the areas where companies have been focusing their efforts. We’ll wrap with five key lessons BPC companies can draw from the broader movement toward sustainable beauty.

Executive Insights

A Beautiful Concern: Sustainability Takes Hold in Beauty and Personal Care

A Beautiful Concern: Sustainability Takes Hold in Beauty and Personal Care

April 26, 2022

Key takeaways

Most consumers would pay 35-40% more for a sustainable version of their regular beauty and personal care (BPC) products, part of a trend that’s become a significant growth driver for BPC brands.

In response to the uptick in consumer demand, BPC businesses are focusing their sustainability efforts in three areas: packaging, ingredients and energy.

The trend’s growth indicates that sustainability is becoming table stakes for BPC brands and is tied into an emerging minimalist mindset.

Amid regulatory fragmentation and varying industry standards, brands that take the initiative on sustainability will have the advantage.

Cleaning up the industry’s act

From formulations to containers, BPC products leave a big environmental footprint. Just how big is anyone’s guess. According to Euromonitor, in 2021 the beauty industry produced 97.9 billion units1 of plastic packaging alone.2 Then there’s other packaging like foil packets, cardboard boxes and shrink-wrap — not to mention applicators and the ingredients that go into the product itself. It’s unlikely that much of this material is recycled: The Environmental Protection Agency says that close to 70% of the 14.5 million tons of plastic containers and packaging the U.S. generated in 2018 ended up in a landfill.

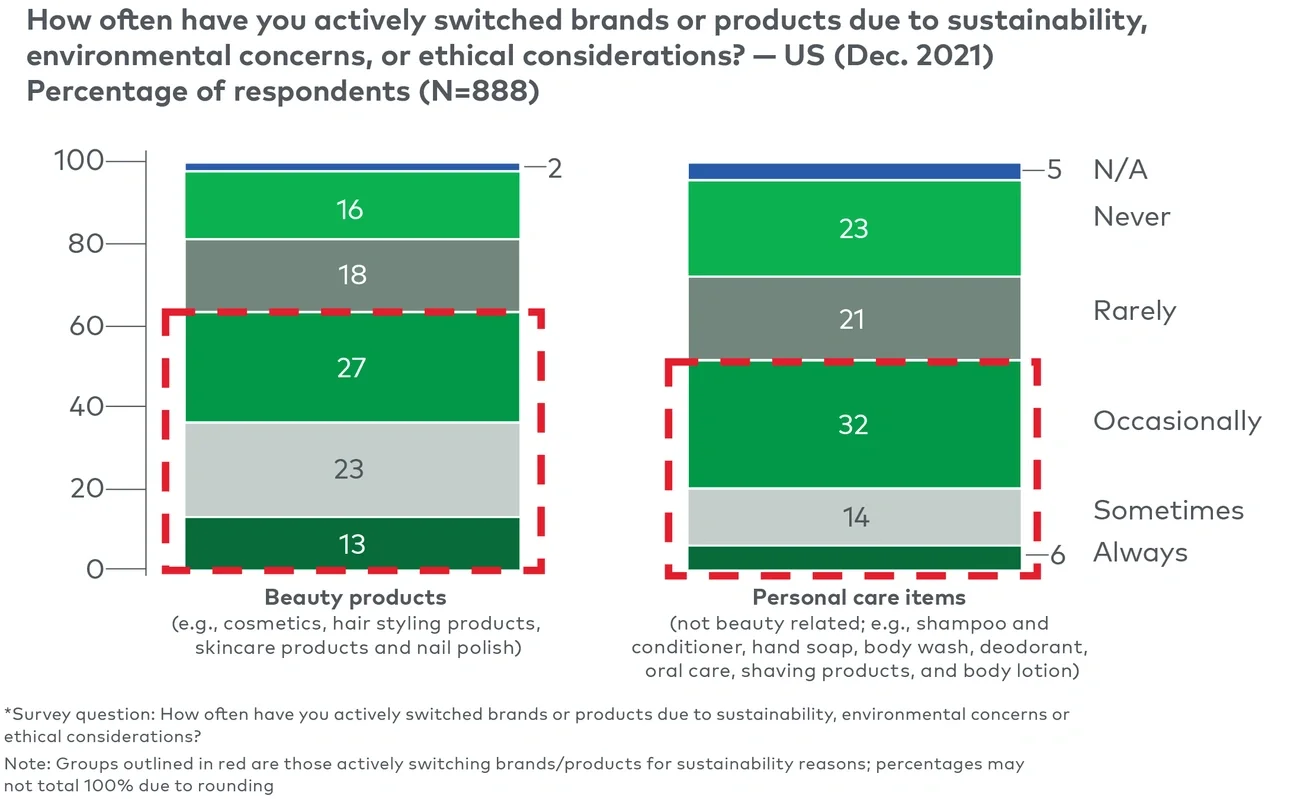

The issue is on the radar of a growing number of consumers. According to L.E.K. Consulting’s Consumer Sustainability Survey 2022, U.S. consumers rate sustainability as their fourth-highest criterion for purchasing beauty products. The same survey reveals that 58% of U.S. consumers state they would pay more for sustainable versions of their regular personal care products, while nearly the same proportion, 56%, would do the same for their beauty products. How much more would they pay? About 35-40%, consumers say. In addition, most U.S. consumers say they have switched BPC brands due to sustainability, environmental or ethical concerns (see Figure 1).

Figure 1

Percentage of U.S. consumers who say they are actively switching beauty and personal care brands/products for sustainability reasons

Image

Companies that make progress toward these expectations are seeing the value. Some 34% of BPC brands participating in L.E.K.’s 2020 Brand Owner Packaging Study agreed that the upsurge in consumer demand for sustainable products and services had been their most significant growth driver over the previous two years. Other research bears this out. As a rough analog to sustainable skin care, the global market for natural skin care products hit $6.7 billion in 2021 and is on track to grow an average of 6.6% a year through 2030, according to a report from Grand View Research. And findings from Brandessence Market Research point to a global clean beauty market that topped $5.4 billion in 2020, with a compound annual growth rate of 12% through 2027.

Building a lean, green beauty machine

BPC businesses are responding to these consumer preferences by focusing on three areas: packaging, ingredients and energy.

Packaging. If sustainability is the goal, the first rule in packaging is simply to use less of it. That includes an emphasis on reusable packaging (with return and refill options) and getting away from single-use items (think face masks, wipes and ampules). What packaging there is may consist of materials that are recycled — like the bottles and jars that Estée Lauder uses in its Aveda line of hair and skin care or Colgate’s fully recyclable toothpaste tube — or biodegradable.

Ingredients. Sustainability can mean different things when it comes to product ingredients. Some consumers look for natural or even organic ingredients. Others focus on an absence of synthetics or ingredients they believe are potentially harmful, a category that can include preservatives, emulsifiers, thickeners and color pigments. Still another approach is to emphasize sustainable sourcing, whether that means avoiding nonsustainable resources or building relationships with supply chain partners that use sustainable practices to produce raw materials. Burt’s Bees ticks several of these boxes with its responsible sourcing policy, avoidance of certain chemicals in its products and reliance on formulas of natural origin.

Energy. Even a sustainably packaged, all-natural product takes energy to produce and get into the hands of consumers. This has BPC companies like Aveda, Dr. Bronner’s and Twelve Beauty turning to renewable energy like solar and wind power to help power their manufacturing processes. Companies can extend the reduction of greenhouse gas emissions through the supply chain. One way is by redesigning their products to make them lighter, smaller and less expensive to transport and to require less packaging, as Klorane did with its shampoo bar. Brands can also require partners and suppliers to reduce their own emissions.

Implications for the BPC industry

These are nontrivial changes for the industry to make, a sign that the sustainability trend is here to stay. What are the implications for BPC brands? Here are five that come to mind.

1. Sustainability is becoming table stakes. One sign is the increasing emphasis on cosmetics with plant byproducts or disposable agronomical wastes versus artificial chemicals. Even some natural ingredients have come under fire. Palm oil, for example, is efficient to produce and has a number of beneficial properties — but it’s also highly correlated with deforestation and habitat destruction.

Sustainable products and business practices are likely to become even more important as younger consumers replace older ones in the marketplace. At first, consumers will look for sustainable products to add to their bathroom shelf, but eventually they may ignore products that deprioritize sustainability altogether. For brands, key focus areas include transparency — especially online, where most buyers do their research — and alignment with influencers who promote mindful consumption. Other initiatives, such as recycling programs, can also come into play.

2. A minimalist mindset is emerging among BPC consumers. Some of that is a desire to reduce their consumption, as evidenced by the roughly 20 million online videos featuring “shop your stash,” no- or low-buy, and anti-haul challenges. But there’s also growing consumer interest in the fresh-faced, no-makeup look of Merit, Jones Road and other brands. As a result, consumer discussion of intricate and bold looks is waning. In 2019, for example, social media posts about festival makeup and winged eyeliner declined 6% and 9% respectively.

Minimalism has sent consumers in search of more bang for their beauty buck. Beauty detoxes (e.g., skin “fasting”), streamlined routines and multifunctional ingredients (e.g., hyaluronic acid and peptides) are expected to continue their fast-growth trajectory. Products with temporary results or limited efficacy are expected to drop off along the way.

3. A fragmented regulatory environment favors sustainable practices. Consider the use of plastics, which are subject to a spectrum of regulation in the U.S. At one end are the “ban preemption” laws that some states have enacted to keep localities from regulating plastic. At the other end are states and municipalities that have cracked down on plastics more broadly. The result is a regulatory patchwork where, in the interest of risk management, many brands will adapt their practices to the most restrictive regime.

In any case, government stakeholders are responding to constituent concerns. As demand for sustainable corporate practices goes up, regulatory activity may follow. Staying abreast of it all will require coordination across functions like procurement, manufacturing and shipping. It may also require ongoing updates to everything from supplier relationships and ingredient procurement to marketing, research and development.

4. Industry heavyweights aren’t waiting for regulators. Ulta says that half of the packaging in its product assortment will be recyclable or refillable, or consist of recycled or bio-sourced materials by 2025. Sephora’s chemicals policy includes a list of ingredients to be reduced or eliminated among the third-party brands it carries. In addition, Sephora has joined other retailers like CVS, Walmart and Target on the Green Chemistry & Commerce Council, which promotes the use of safer and more sustainable chemical solutions.

Some brands are taking a similarly collaborative approach. A recent example is the effort among beauty giants L’Oréal, Unilever, Henkel, LVMH and Natura &Co to develop a scoring system that allows consumers to evaluate the environmental impact of BPC products. Responses like this one are an implicit acknowledgment that BPC brands will have to meet the sustainability demands of not only consumers but retailers as well if they want to get their products on the shelves.

5. Brands that take the initiative will have the advantage. For BPC brands, sustainability is a sweeping and often confusing set of expectations. Interpreting them in ways that are meaningful and resonate with consumers is no small strategic challenge. In the absence of industrywide standards, leading companies are defining for themselves what sustainability looks like, rather than wait for the competition or government to do it for them.

Unilever’s Dove, for instance, introduced a refillable, aluminum-free deodorant. Garnier rolled out a skin serum packaged in recycled material and manufactured in a plant that mostly runs on renewable energy. L’Oréal has committed to targets for its use of plastic, including having all of its plastic packaging be reusable, recyclable or compostable by 2025. And a host of brands, from major players to emerging upstarts, have played up their efforts to go carbon neutral.

Heading into a more sustainable future

Beauty products have a not-so-pretty impact on the environment, an issue that many companies are working hard to address. The changes they’re making reflect that sustainability isn’t just an ecological issue anymore. It’s a consumer issue as well — and for brands, it’s moving from an add-on to a must-have in a marketplace of increasingly eco-sensitive BPC consumers.

View more results from our Consumer Sustainability Survey 2022, and read how businesses need to focus on the needs of curent and future generations in our Sustainability Centre of Excellence.

Endnotes

1Types of packaging includes blister and strip packs, flexible aluminum/plastic, flexible paper/plastic, flexible plastic, aluminum/plastic pouches, plastic pouches, rigid plastic

2Euromonitor, Passport, packaging types historical/forecast

Related insights

You might also be interested in these insights.

English