During 2023, widespread concern arose about — and some early data came to light regarding — indications that trading down was occurring in the pet food category. If so, it would mark the reversal of a yearslong trend. How extensive was this apparent shift, and what are the implications for pet food brands? To find out, L.E.K. Consulting surveyed 1,600 dog and cat owners. Here’s what we discovered.

Consumer profiles

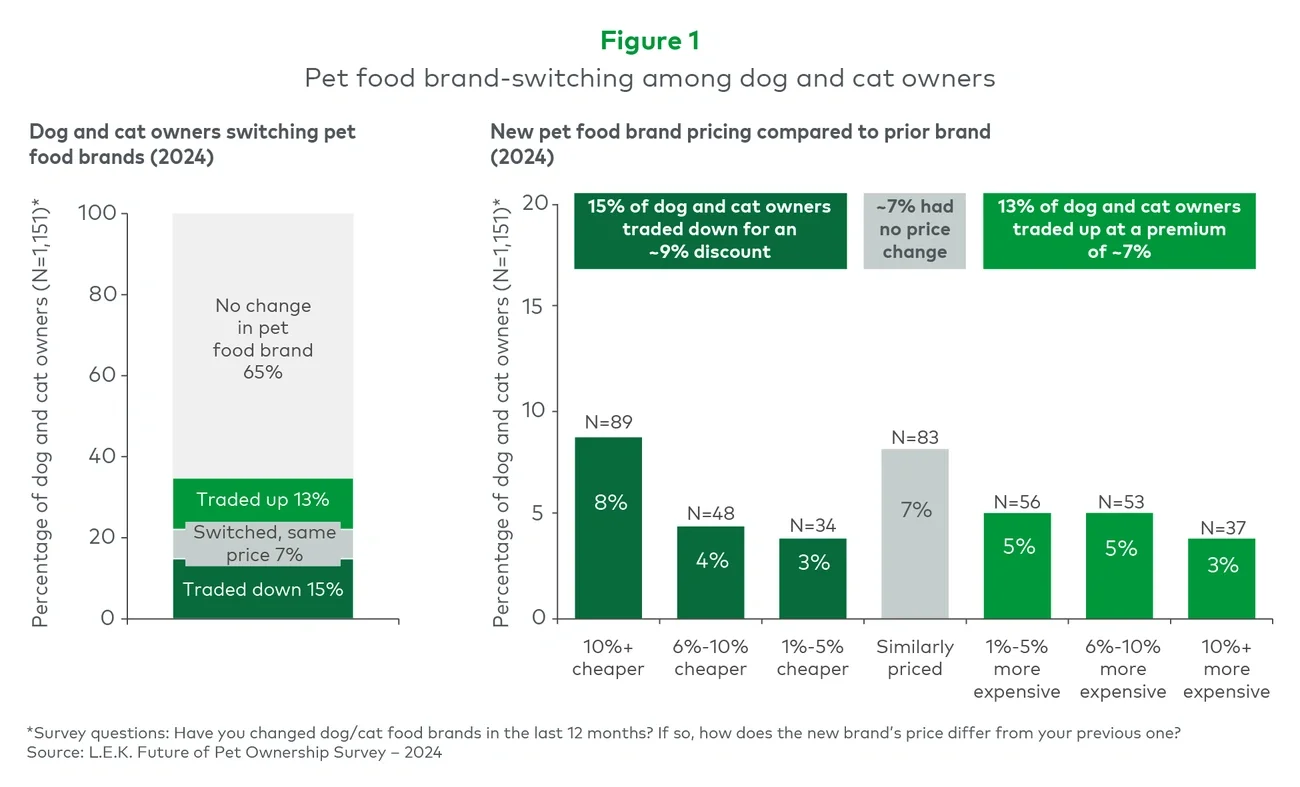

Based on our survey, roughly 1 in 3 pet owners tried a different pet food brand in 2023. One in 7 (15% of all pet owners) traded down, achieving an average discount of about 9%. Meanwhile, closer to 1 in 8 (13%) traded up at an average premium of roughly 7% (see Figure 1).