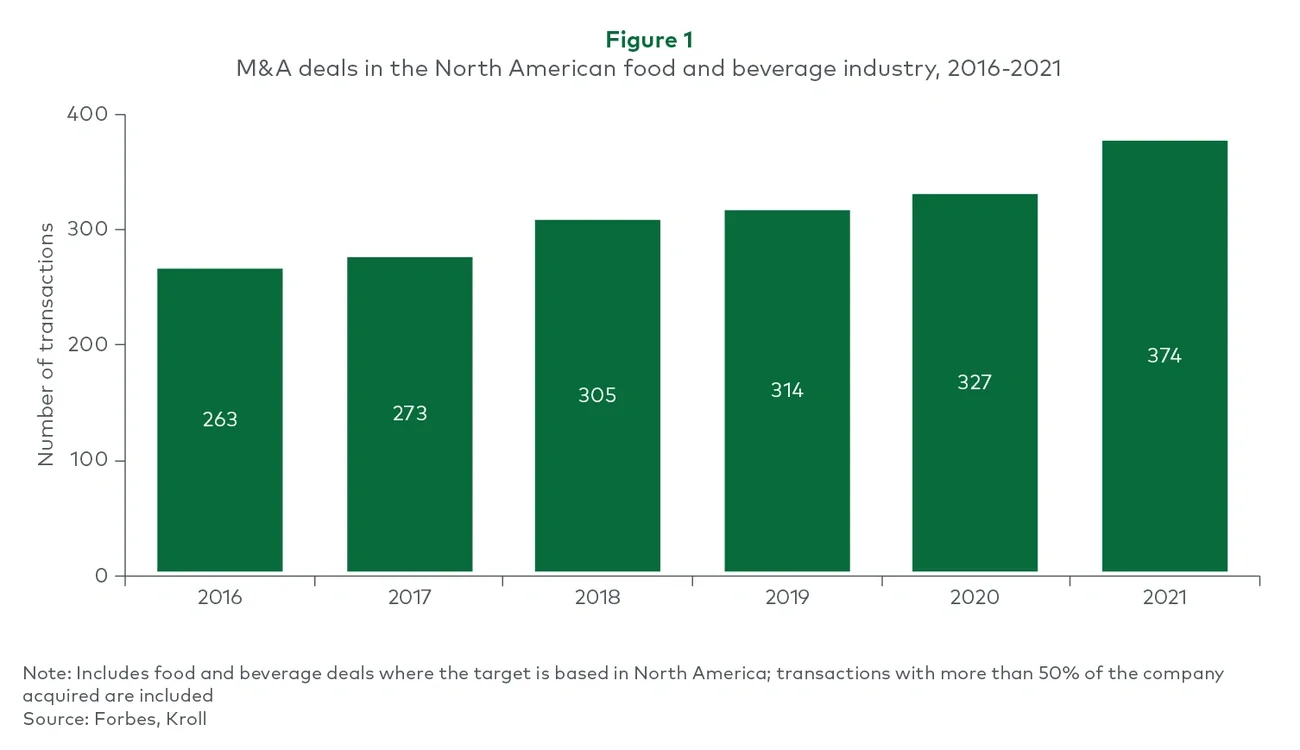

Food and beverage (F&B) saw record M&A activity in 2021, even in the face of higher inflation, tangled supply chains and the lingering impact of COVID-19. A combination of low interest rates, sound economic growth, strong capital markets and shorter portfolio company hold periods provided a strong environment for deals in the sector (see Figure 1).

Image

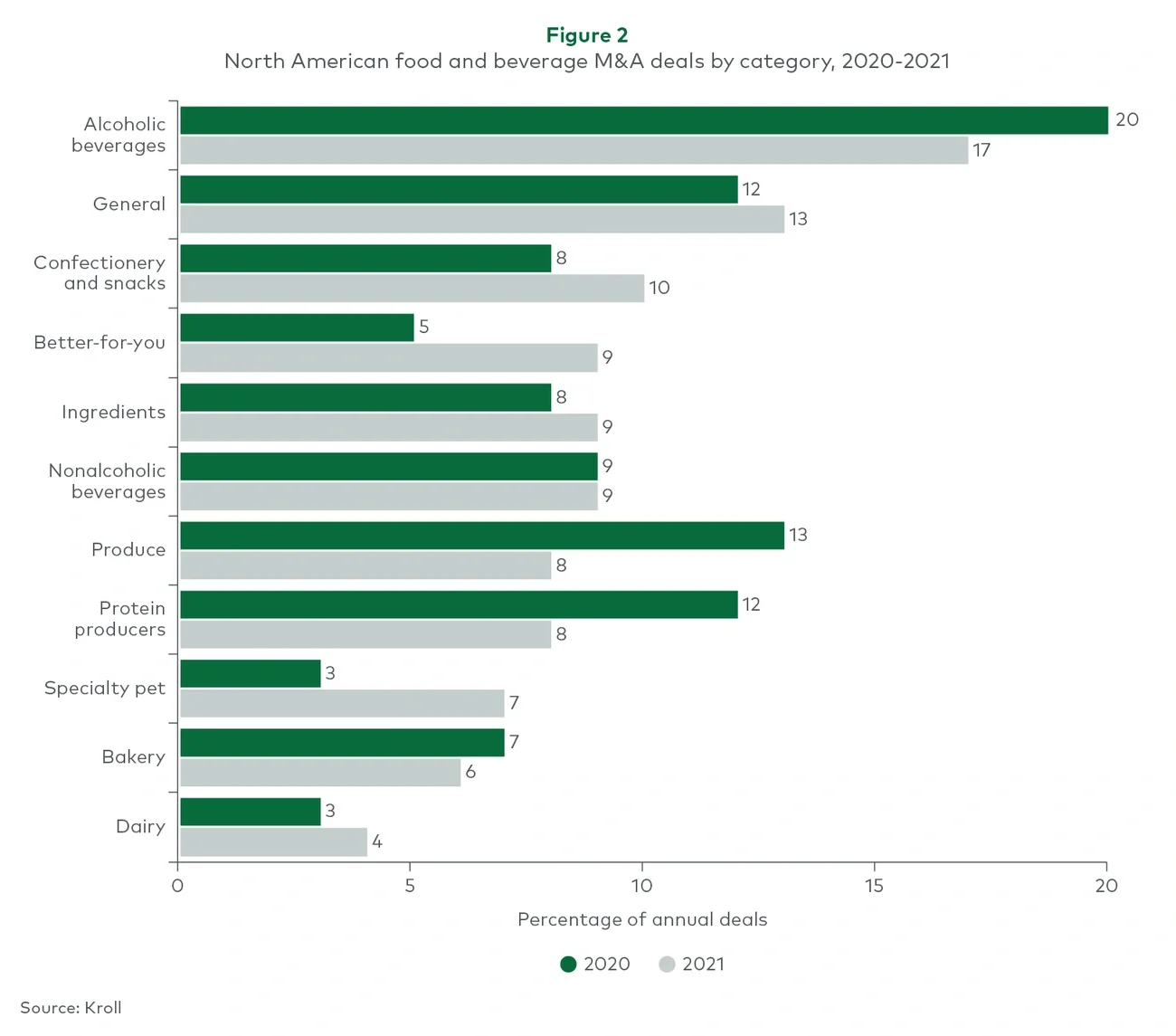

M&A deals in the confectionary and snacks, Better-for-You (BFU) and specialty-pet segments saw strong growth in 2021. Among all categories, alcoholic beverages had the highest deal volume during the past 2 years (see Figure 2).

Image

And on the heels of a record-breaking 2021, M&A activity in food and beverage continues to be strong in 2022. Indeed, ample dry powder and robust fundraising activities continue to favor high levels of private equity (PE) activity in this sector. Notably, the COVID-19 pandemic has reshaped consumer behavior and with it, the types of possible F&B investments. New consumers have flocked into the food-at-home segment, particularly those between 25 and 44 years of age. While a full reopening of bars and restaurants without pandemic-related restrictions may reverse some trends, certain stay-at-home behavior is expected to carry over. For example, 71% of Americans recently indicated they are likely to continue to cook at home more than they did before the pandemic began.

In 2022, emerging so-called foodtech companies and products warrant further attention from investors. By 2030, plant-based alternatives are expected to grow from low single digits today to 10%-15% for meat and 10%-20% for dairy. In the meantime, controlled environment agriculture has experienced an influx of investments from PE, pension funds and retailers.

For both existing and potential PE investors in F&B, 10 megatrends are impacting the industry:

-

F&B continues to be an attractive area for investment. The F&B industry is currently valued at around $1.9 trillion and has demonstrated both steady growth and resilience to recession over time.

-

Inflation is impacting recovery from the pandemic. Consumer prices for food spiked far above a 2.4% historical food CPI average in 2021, though they remained below the highs seen during 2008.

-

Plant-based products are becoming ubiquitous. As consumers increasingly choose healthy foods, purchases of plant-based options for traditionally non-vegan meals are continuing to rise, including among non-vegetarians.

-

Functional and better-for-you F&B is garnering more interest. Products with functional benefits are gaining traction, as are BFY options such as clean-label/grain-free.

-

Indulgence as a driver for consumer choice is important and evolving. Consumers continue to indulge in sweet snacks but are also seeking healthier alternatives to their favorite classic desserts and treats.

-

Ethnic/authentic foods are reaching wider audiences. Evolving consumer demographics, interest in new cuisines and the flavor diversity that result is lifting demand for a wider variety of ethnic and ethnically authentic foods.

-

Environmental, social and governance factors are becoming more important. The use of upcycled food, activism in line with social justice causes and equitable firm-wide initiatives are among the practices enabling heightened success for many F&B brands.

-

Frozen foods have surged as the pandemic has continued. The pandemic has been a boon for frozen foods as consumers continue to look for convenient, healthy options for all eating occasions.

-

Private label and freshly prepared foods are maintaining and gaining traction, respectively. Not only has the growth of private label historically outpaced brands by a significant margin, investing in perimeter and freshly prepared foods is now also top of mind, according to retailers.

-

Co-manufacturing continues to be highly attractive. A rise in third-party manufacturing, numerous rollup opportunities and enticing acquisition multiples continue to make co-packing an attractive investment choice.

Changing consumer behavior and the availability of tech-powered new options combined with robust economic fundamentals are continuing to power M&A activity in the F&B space, with 2022 showing no signs of slowing down— even after hitting never-seen-before levels the year before.

To learn more about how we can help your organization create value in the F&B industry, please contact us.

Related insights

You might also be interested in these insights.

English