Imagine if health care were like interacting with your favorite consumer brand. You could arrange a consultation on demand from an app on your phone, like a meal from DoorDash or a ride from Uber. A doctor might seamlessly monitor your progress from afar, or come to your home to treat you, much as someone from TaskRabbit comes to your home to help assemble your dining table. You could even have at-home equipment for testing and therapy, with professional guidance via livestream should you need it — think Peloton, but for medicine.

A world where healthcare caters to patients as consumers has been predicted for years. But so far, reality hasn’t lived up to the expectation. Now, a set of macrotrends is creating a burning platform for healthcare players to put patients at the center of their business. The impact of consumerism is leaving no healthcare sector exempt, reaching traditional healthcare stakeholders (e.g., providers, payers, medtech, life sciences) and piquing interest in non-traditional players (e.g., tech, retail).

This article is the first of a series about the implications of the new consumer healthcare reality. In this installment, we’ll start off with a look at the macrotrends driving healthcare toward consumerism. Then we’ll walk through some broad, but key, steps to getting consumer-centricity right.

A healthcare landscape in flux

The trend toward healthcare consumerism is influenced by several key landscape changes in the rapidly evolving healthcare landscape:

- Increasing healthcare costs and the shift toward value-based care

- Growing patient desire for convenience in healthcare

- Expanding competition within healthcare and the need to innovate to retain and gain consumers

Increasing healthcare costs and the shift toward value-based care

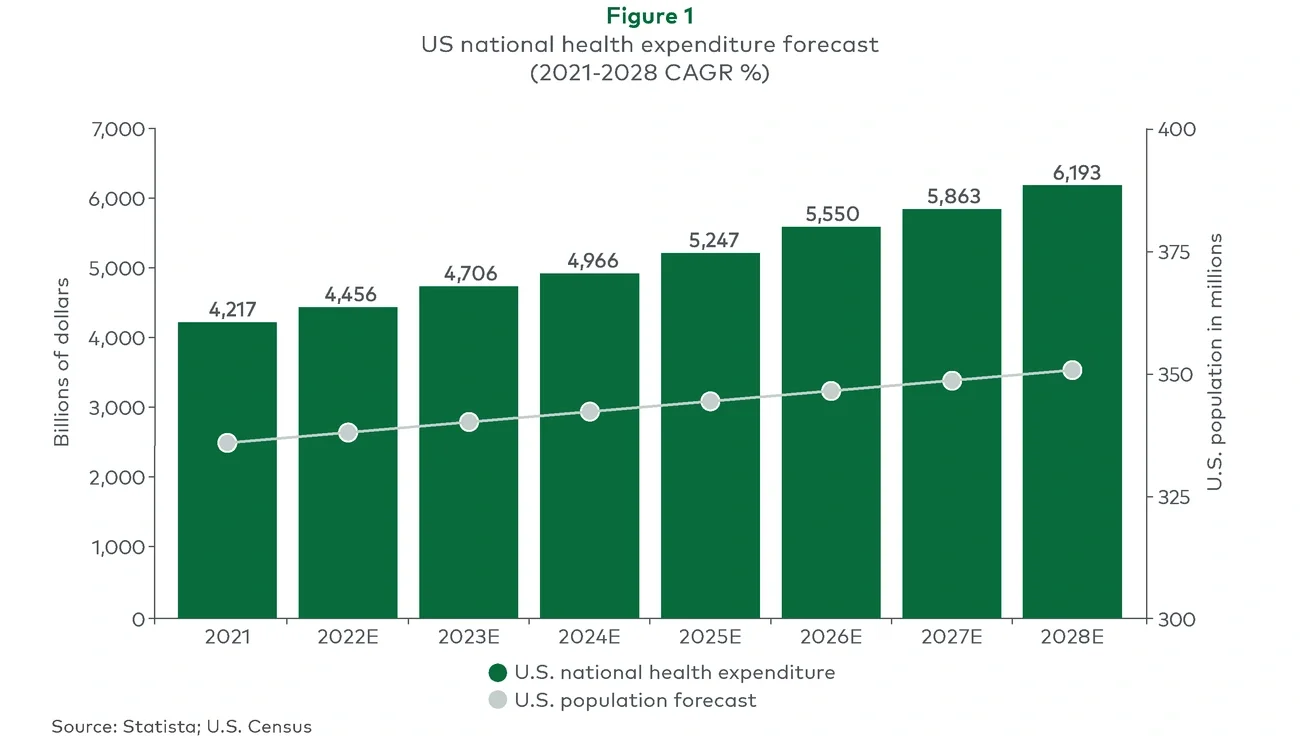

Escalating costs (see Figure 1) have healthcare providers sharpening their focus on prevention and overall wellness in a bid to reduce per-patient healthcare expenditures. A key motivator has been the shift to value-based care, in which reimbursements are tied to patient outcomes versus services delivered.