COVID-19 in the US: Consumer Insights for Businesses — Edition 5

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

In partnership with Civis Analytics, we’re publishing a series of insights on the consumer response to COVID-19. Our goal is to help our consumer-facing clients monitor sentiment and behaviors as they take shape during this unprecedented period.

At the same time, we acknowledge that the pandemic is a humanitarian crisis first and foremost. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this crisis.

This is the fifth and final installation of our COVID-19 Consumers Insights Series, which reflects the results of a recurring consumer pulse survey. Administered across 2020, the survey tracks the pandemic’s impact on consumer sentiment overall as well as by segment, geography and product. Each edition offers an updated perspective on the current landscape and what the lasting impact is likely to be.

Edition 5 reflects responses captured in our Nov. 16, 2020, survey of ~2,400 U.S. consumers who are demographically representative of the general population. All prior publications can be found at the L.E.K. COVID-19 Insights Center.

Edition 5 yielded a number of insights that we are excited to share with you now, focused on the following:

Important note: All forward-looking data reported is a reflection of consumer sentiment/expectations and does not constitute official L.E.K. forecasts.

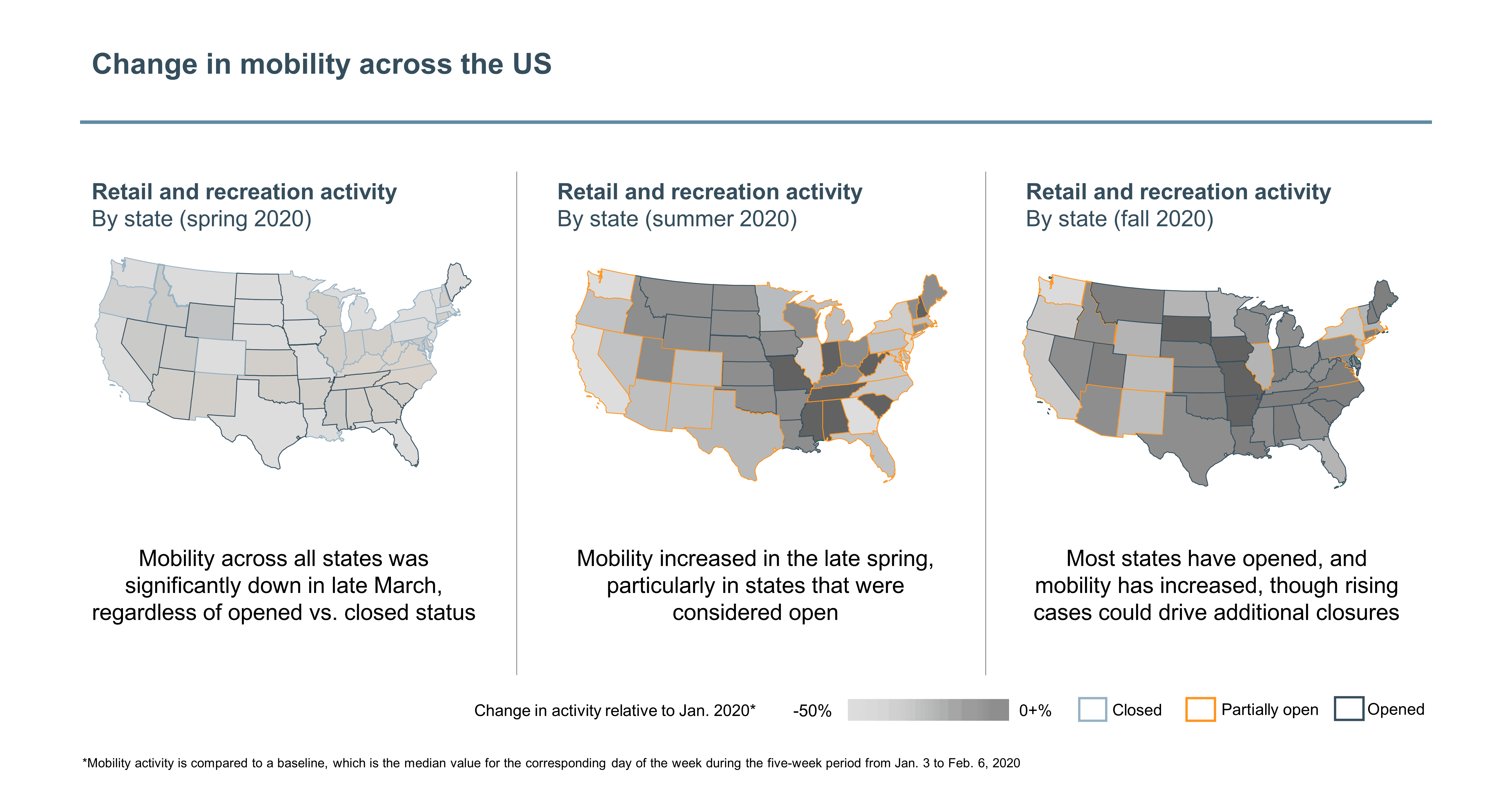

As the country and businesses have continued to open, consumer behavior has gradually shifted back toward pre-COVID-19 levels.

Consumer mobility, in particular, has dramatically increased since the height of the lockdowns in the spring. Google mobility data confirms an increase in retail and recreation activity across the country, with variance across states declining since restrictions began loosening in the late spring and early summer.

Despite these recent increases, mobility is expected to remain below pre-COVID-19 measures in the immediate term, as rising cases drive additional closures across cities and states.

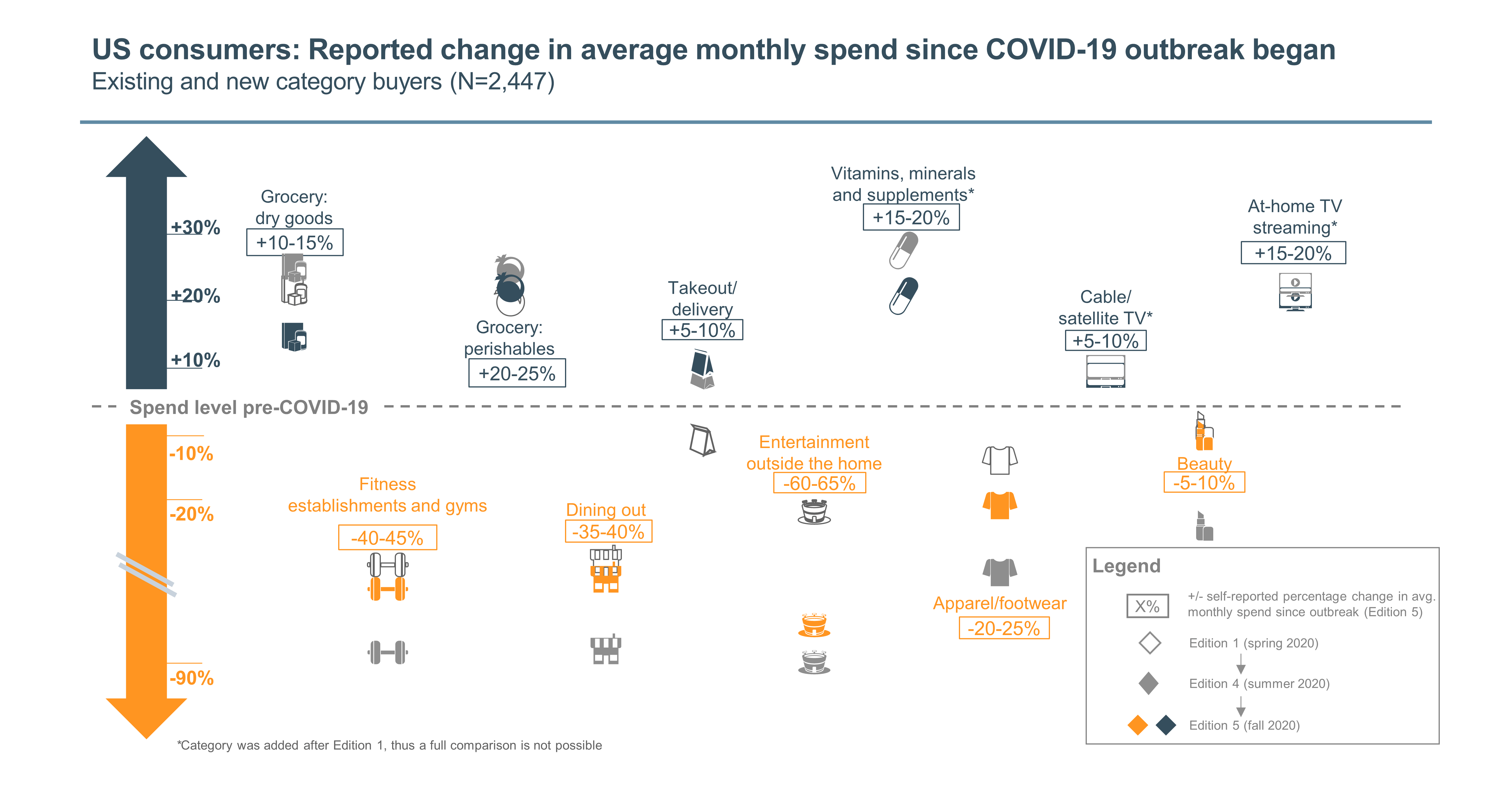

Consumer spending is gradually returning to normal, with expenditure reverting toward pre-COVID-19 norms in most key categories tracked by our research. However, expenditure on experiences and discretionary items still trails pre-COVID-19 levels.

Average spend in essentials like dry groceries (up 10%-15%) and vitamins, minerals and supplements (up 15%-20%) remains high, but outsized increases from the spring and summer have mellowed somewhat as consumers have adapted.

Spend in at-home categories like at-home TV streaming (up 15%-20%) and takeout (up 5%-10%) also remains higher than pre-COVID-19 spend, as many consumers continue to spend additional time at home relative to pre-COVID-19 norms.

Average spend in experiential categories like restaurants (down 35%-40%), fitness/gyms (down 40%-45%), and entertainment (down 60%-65%) is improving, though it remains significantly below pre-outbreak levels. Given many of these activities will be forced indoors or limited as cases rise and winter approaches, we would expect experiential spend to continue to lag that of other categories.

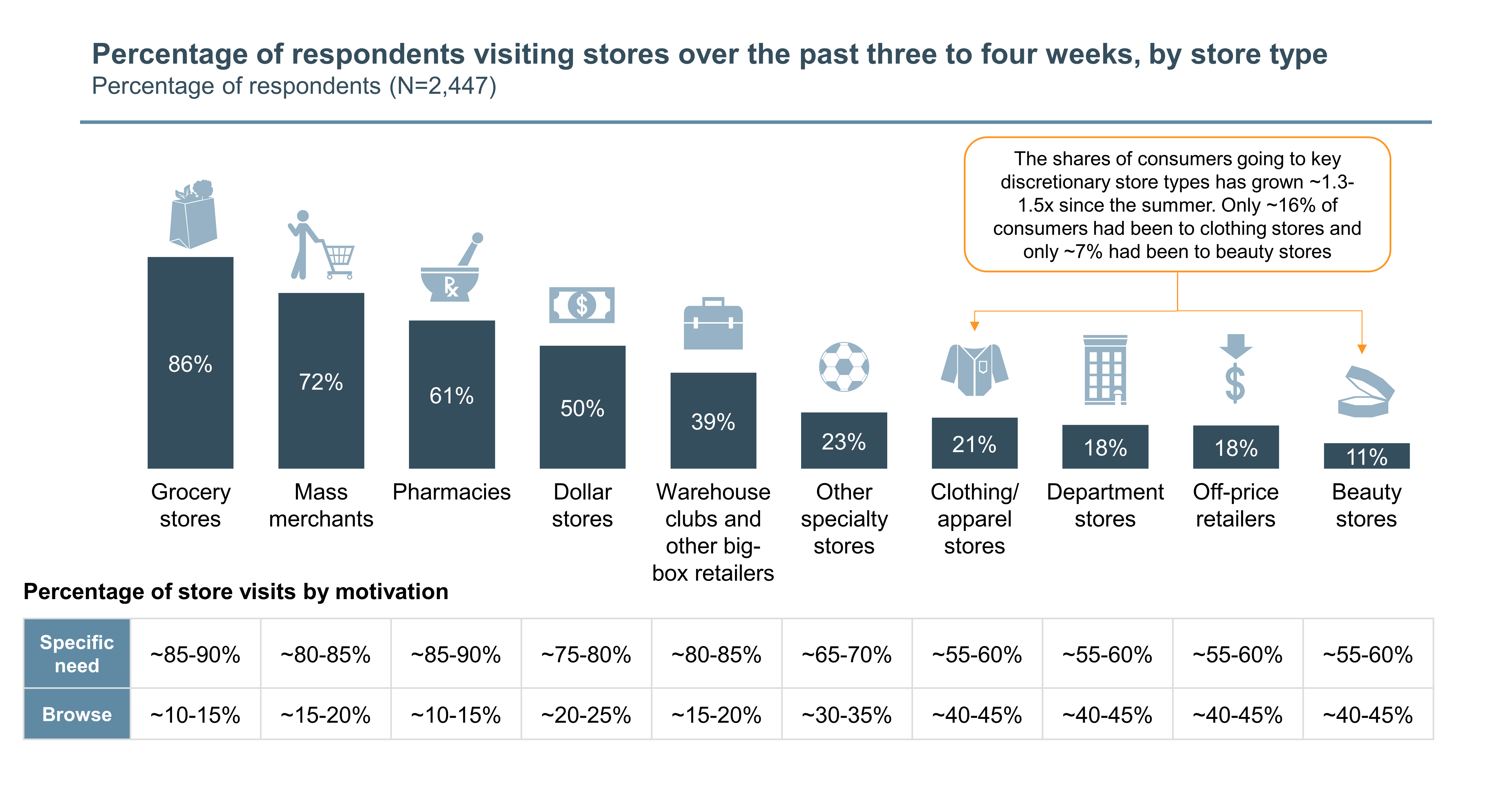

Store visits are also shifting incrementally back toward pre-COVID-19 behaviors. Consumers are gradually returning to nonessential retailers, though the majority of these trips (across store types) remain focused on filling a specific need, rather than browsing.

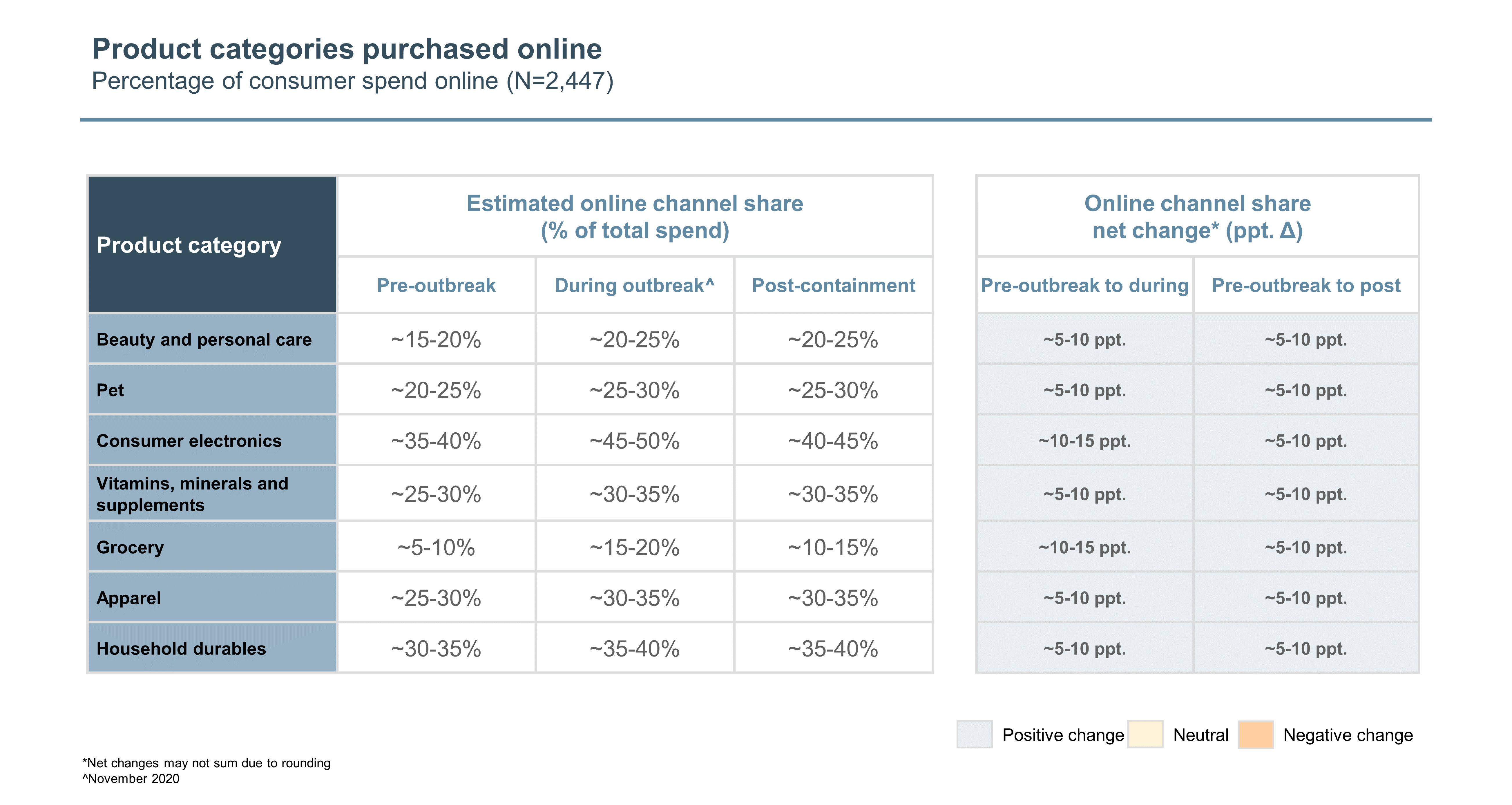

As consumers venture back to brick-and-mortar retailers, online shares of spend are down relative to their peaks during the pandemic. However, online spend still exceeds pre-COVID-19 levels by ~5-15 percentage points across categories, as consumers stay cautious and continue to minimize trips to stores, particularly for discretionary items.

Current variances in online shares by category are in line with pre-COVID-19 estimates. Ecommerce shares remain highest in discretionary categories such as consumer electronics (~45%-50% online), apparel (~30%-35% online) and household durables (~35%-40% online). Online’s share of spend is lowest in groceries (~15%-20%), as few consumers bought groceries online pre-COVID-19 (~5%-10%) and most have returned to shopping in person at these essential retailers.

Consumers expect much of their shift online to be permanent, even after the outbreak is contained, with ecommerce share expected to increase ~5-10 percentage points across categories versus pre-COVID-19 levels.

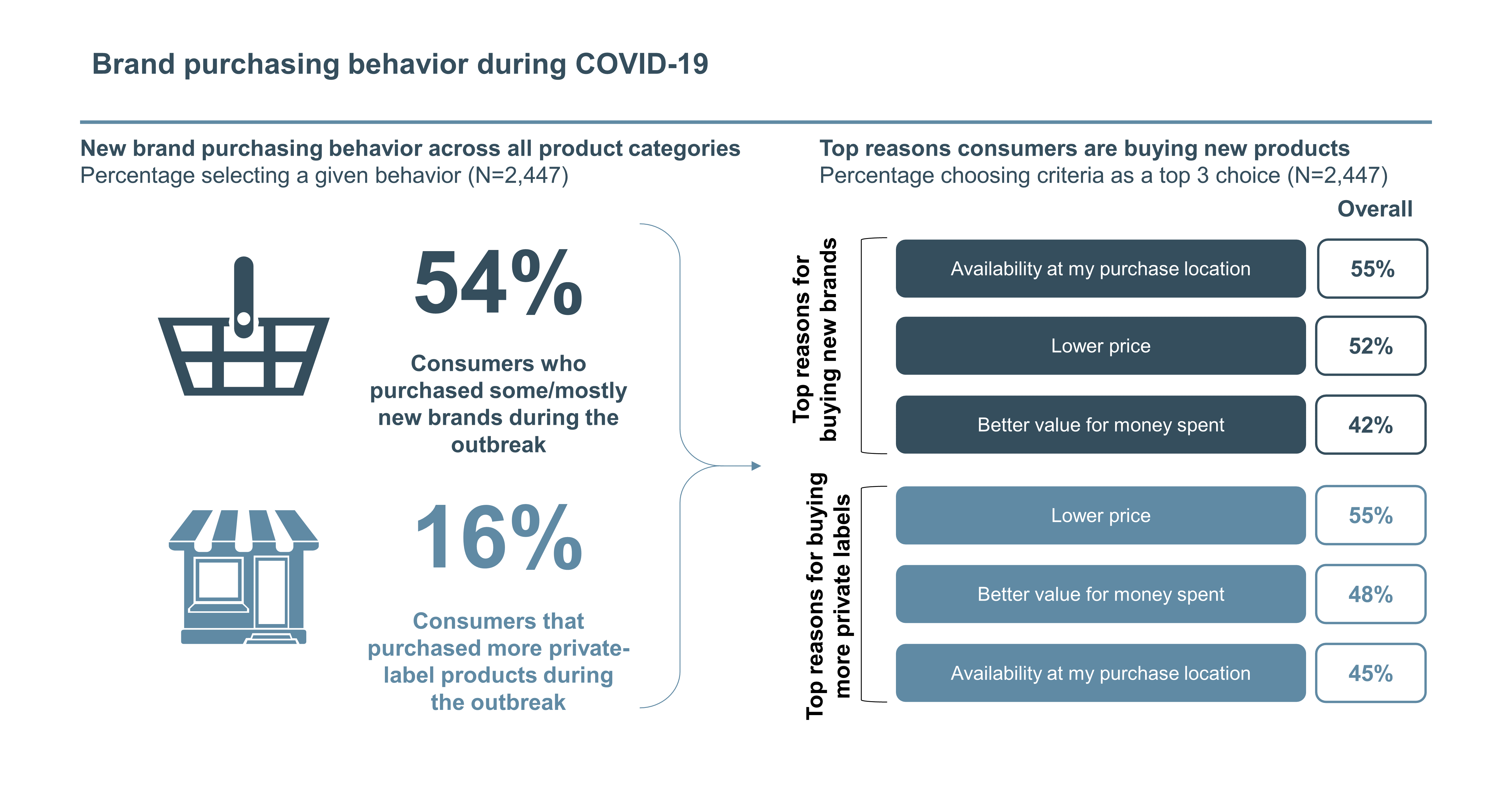

COVID-19-related shifts in channel behavior and income have also driven the trial and adoption of new brands. Approximately 54% of consumers have tried new brands and ~16% have purchased more private labels during COVID-19, primarily due to availability where consumers are shopping, pricing and relative value.

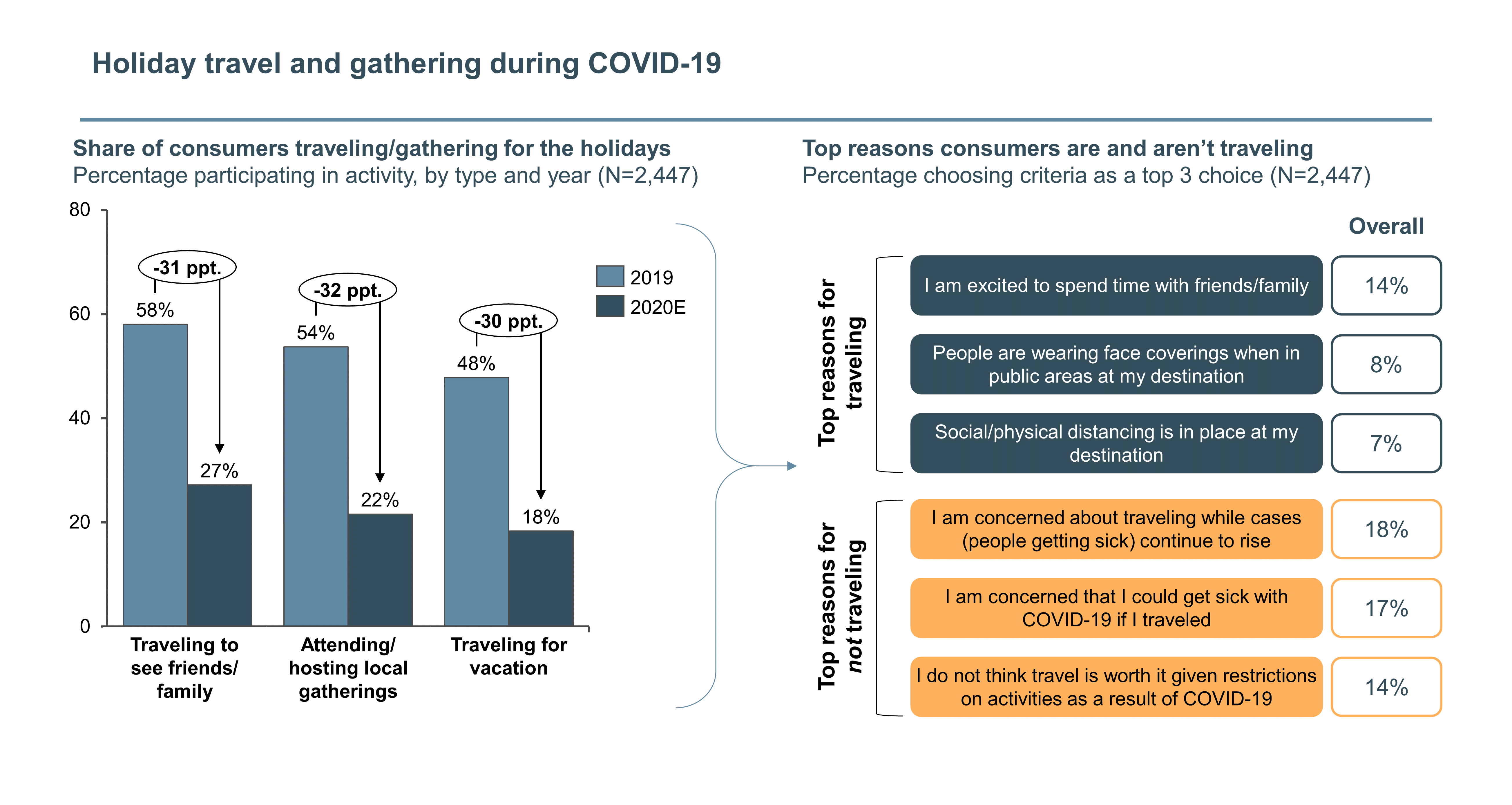

Consumers expect that COVID-19 will have a significant impact on the 2020 holiday season.

Most notably, consumers will stay home this year. The share of consumers traveling to see family/friends (~27%, versus ~58% in 2019) or for vacation (~18%, versus ~48% in 2019) is down significantly year over year. The share of consumers attending local gatherings is similarly expected to be down in 2020 (~22%, versus ~54% in 2019).

Recent spikes in COVID-19 are having a significant impact on this behavior, as concerns over rising cases and getting sick are the top reasons consumers are abstaining from travel this holiday season.

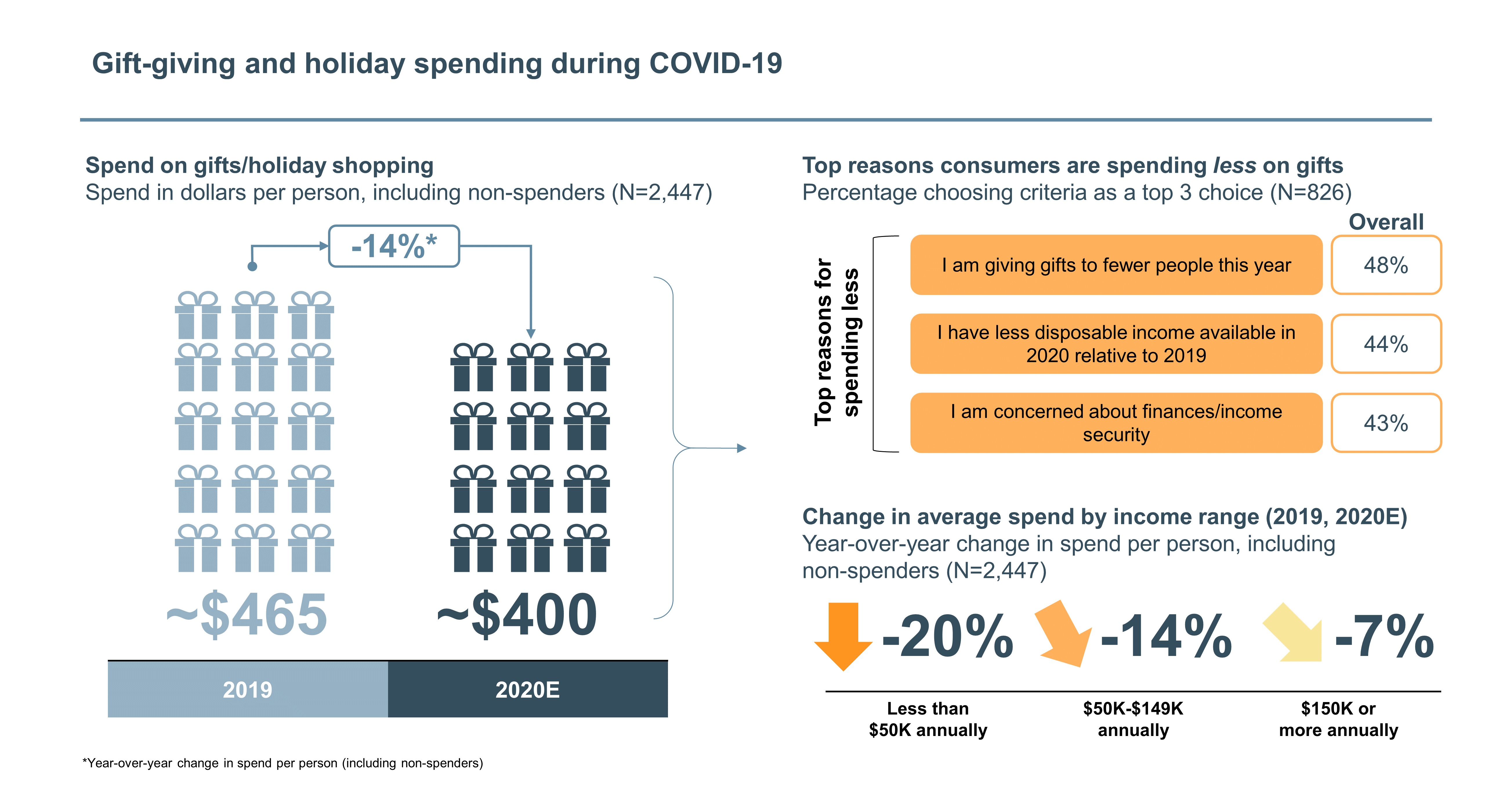

Gift spending will be more resilient than travel, as most consumers will continue to give gifts this year. However, average spend is expected to decline ~14% (from ~$465 to ~$400 per person) as consumers report decreased discretionary income and plan to give gifts to fewer people.

Across income levels, those making less than $50K per year are expected to reduce gift spend the most (~20%). Those making between $50K and $149K per year will reduce spend in line with the total market (~14%), while those making $150K or more will decrease spend by ~7%.

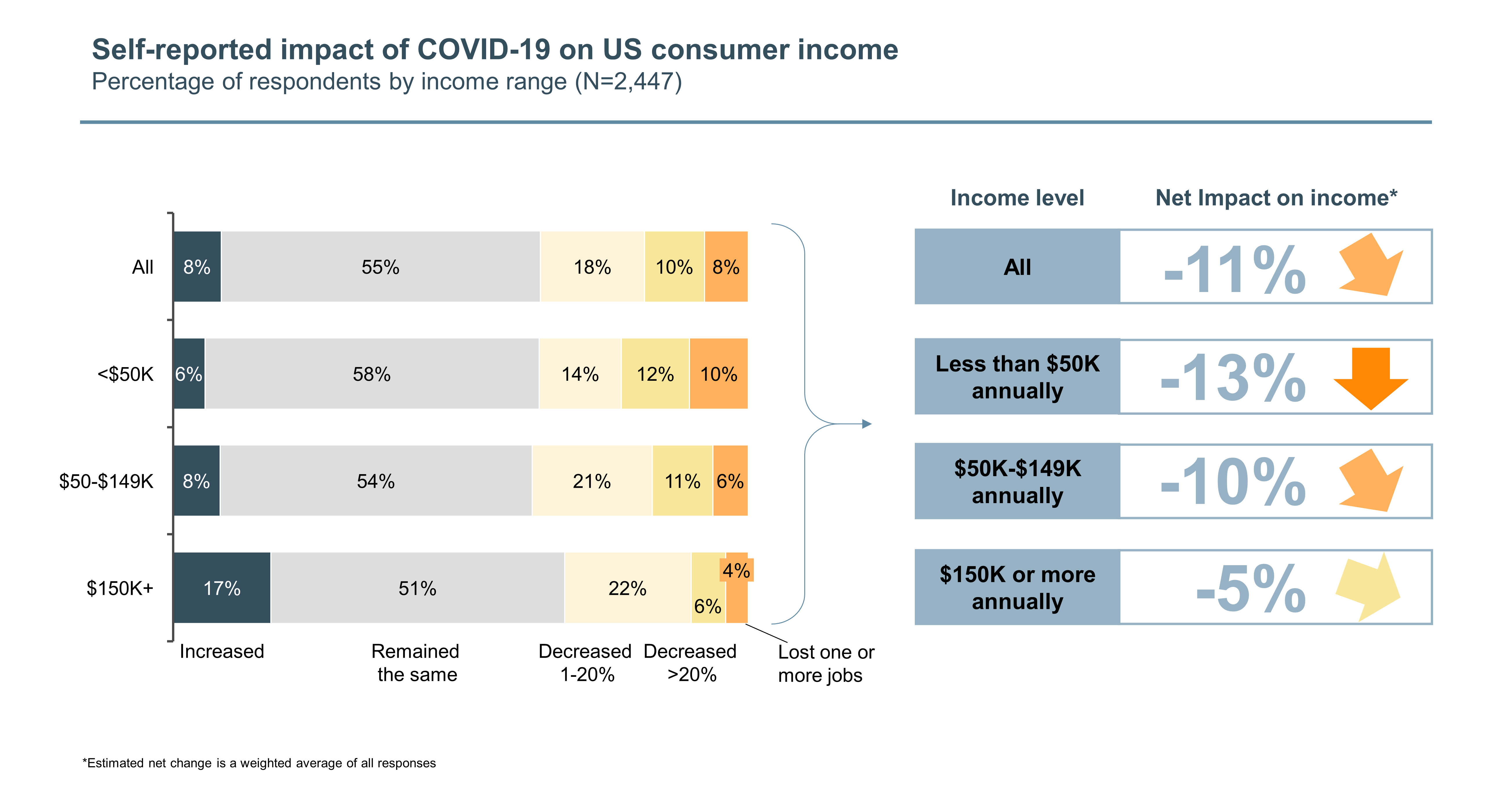

These variable declines in gift spending align with the broader income impacts of COVID-19, with less affluent consumers reporting greater shares of income lost due to the outbreak. Approximately 22% of consumers with annual household incomes under $50K report losing greater than 20% of their income versus ~17% of those between $50K and $149K and only ~10% of those at $150K or more.

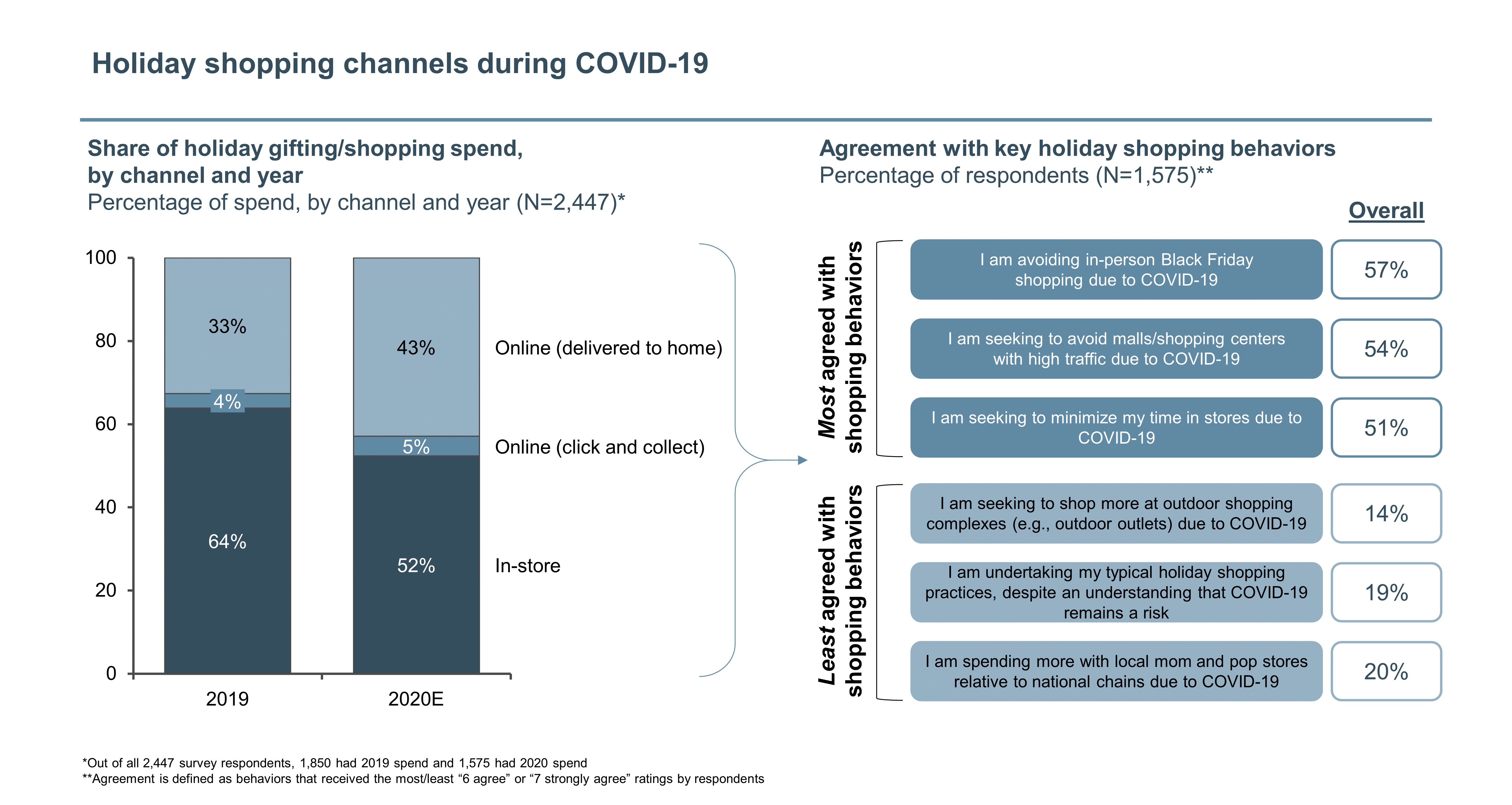

COVID-19 is limiting consumers’ in-person shopping trips for gifts and other holiday supplies.

When asked about their planned holiday shopping behaviors this year, shoppers noted that they will adjust their typical holiday shopping practices in a number of ways: avoiding in-person Black Friday shopping, reducing trips to high-traffic malls and minimizing time spent in stores that they enter.

As a result, the online share of consumers’ holiday shopping spend (including click and collect) will grow significantly, from ~37% in 2019 to ~48% this year.

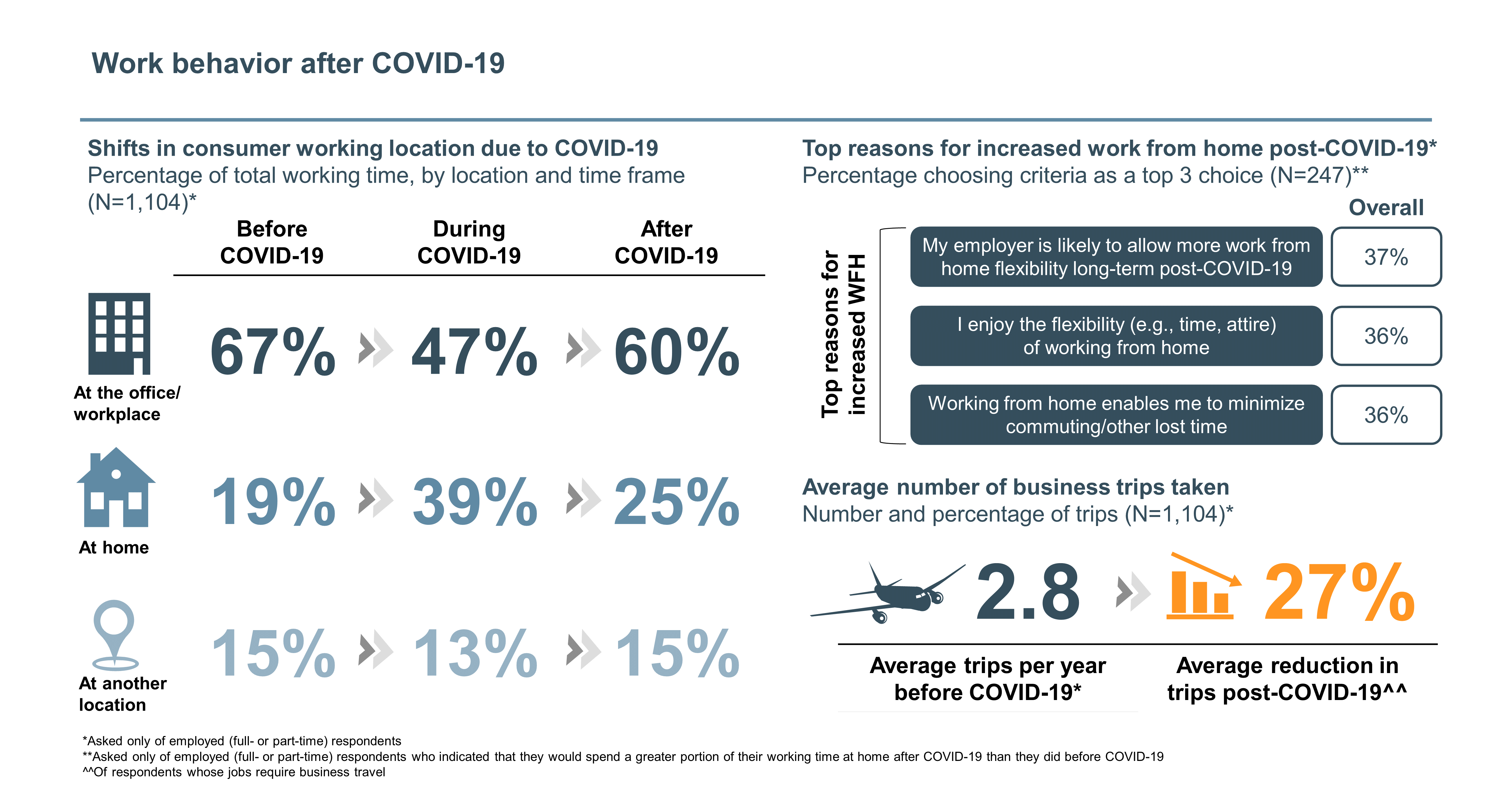

As consumers look to a post-COVID-19 future, they expect the pandemic to permanently change their work and work travel behaviors.

Employed consumers expect a ~1.3x (~6 percentage point) increase in the share of time they work remotely once the outbreak is contained (from ~19% pre-COVID-19 to ~25% post-COVID-19). Business travelers also expect a ~27% decrease in the number of trips they take each year, with these in-person trips replaced by videoconferencing or other virtual meeting options.

These shifts are primarily driven by expectations of greater employer enablement of remote work as well as worker preferences for the flexibility and lack of commute associated with working from home and holding remote meetings.

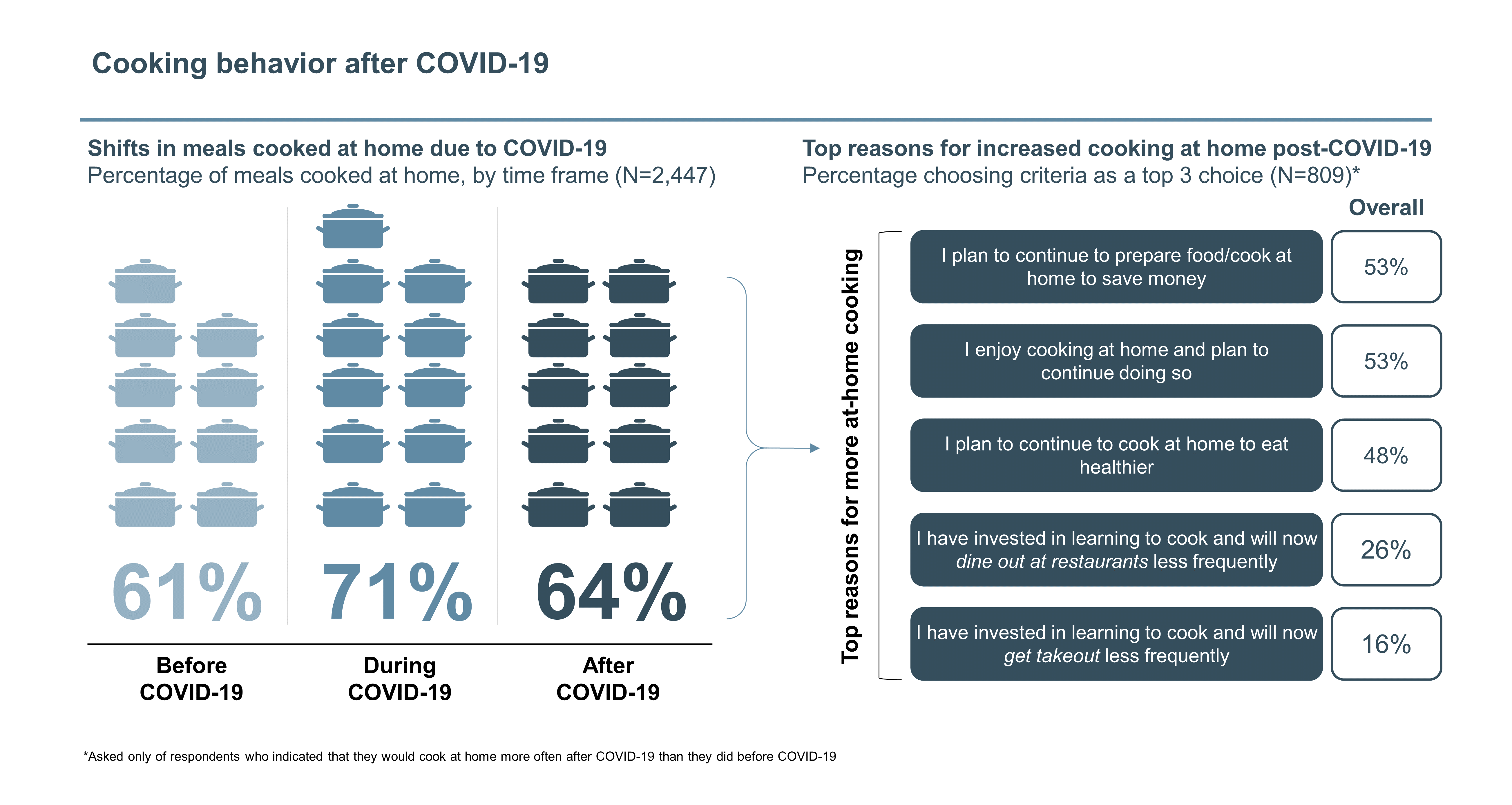

Beyond work, consumers expect long-term shifts in their day-to-day life.

For one, they expect to cook at home more. During COVID-19, consumers have been making ~71% of their meals at home, a ~10 percentage point increase from before the COVID-19 outbreak started. After the outbreak has been contained, consumers expect to make ~67% of their meals at home, retaining a ~6 percentage point increase relative to before the COVID-19 outbreak started.

Consumers suggest that this increase in the share of meals they cook at home in the long term is driven by the cost savings, enjoyment and health benefits that they have discovered in cooking at home during COVID-19.

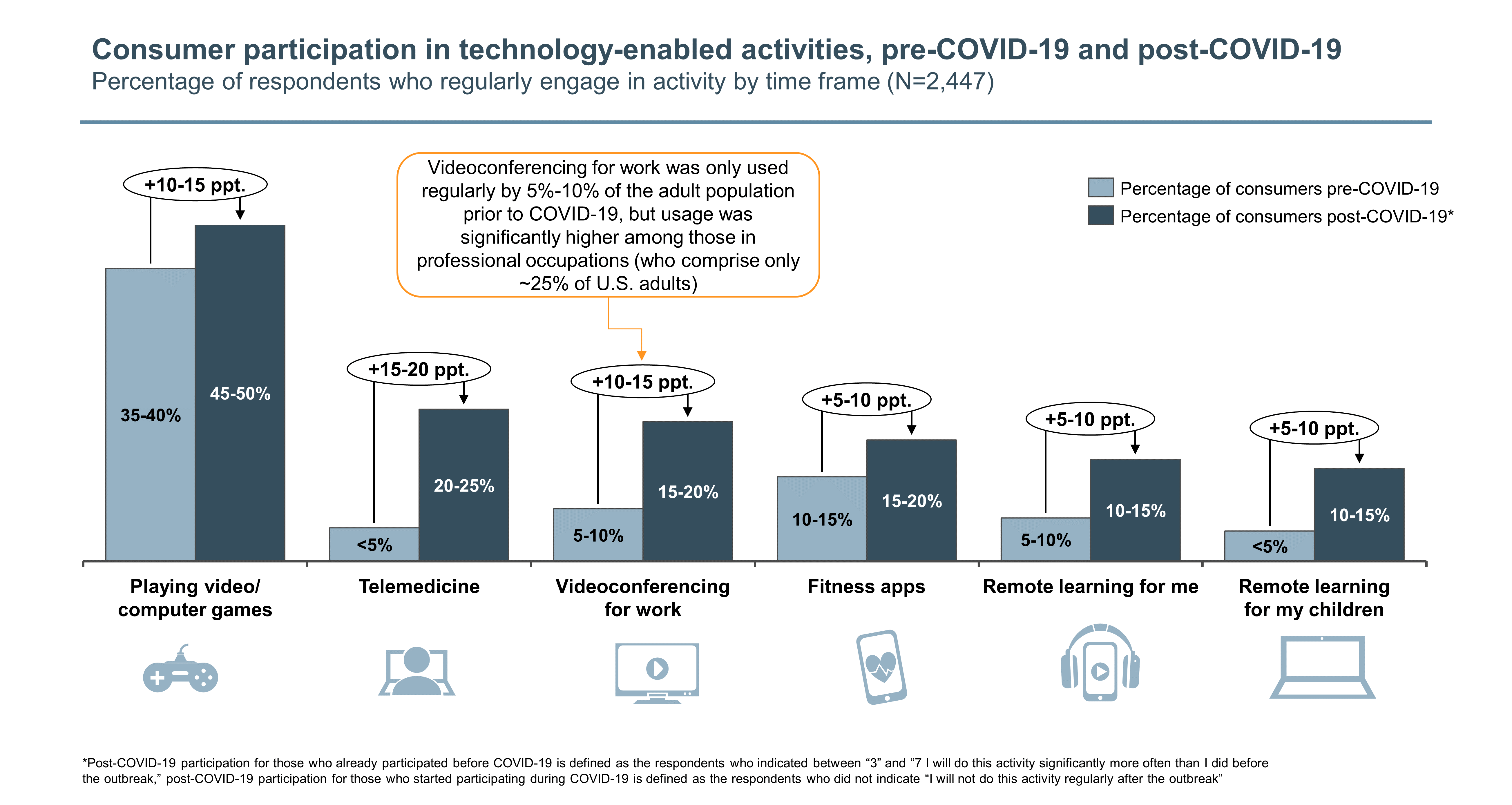

Consumers also see long-term shifts in their usage of technology, especially in the home. COVID-19 has driven new adoption of remote learning and videoconferencing tools, telemedicine, fitness apps and video/computer games that consumers expect to continue once the outbreak is contained. These technology-enabled activities are expected to see a ~10-15 percentage point increase in regular use, on average, relative to before the COVID-19 outbreak began.

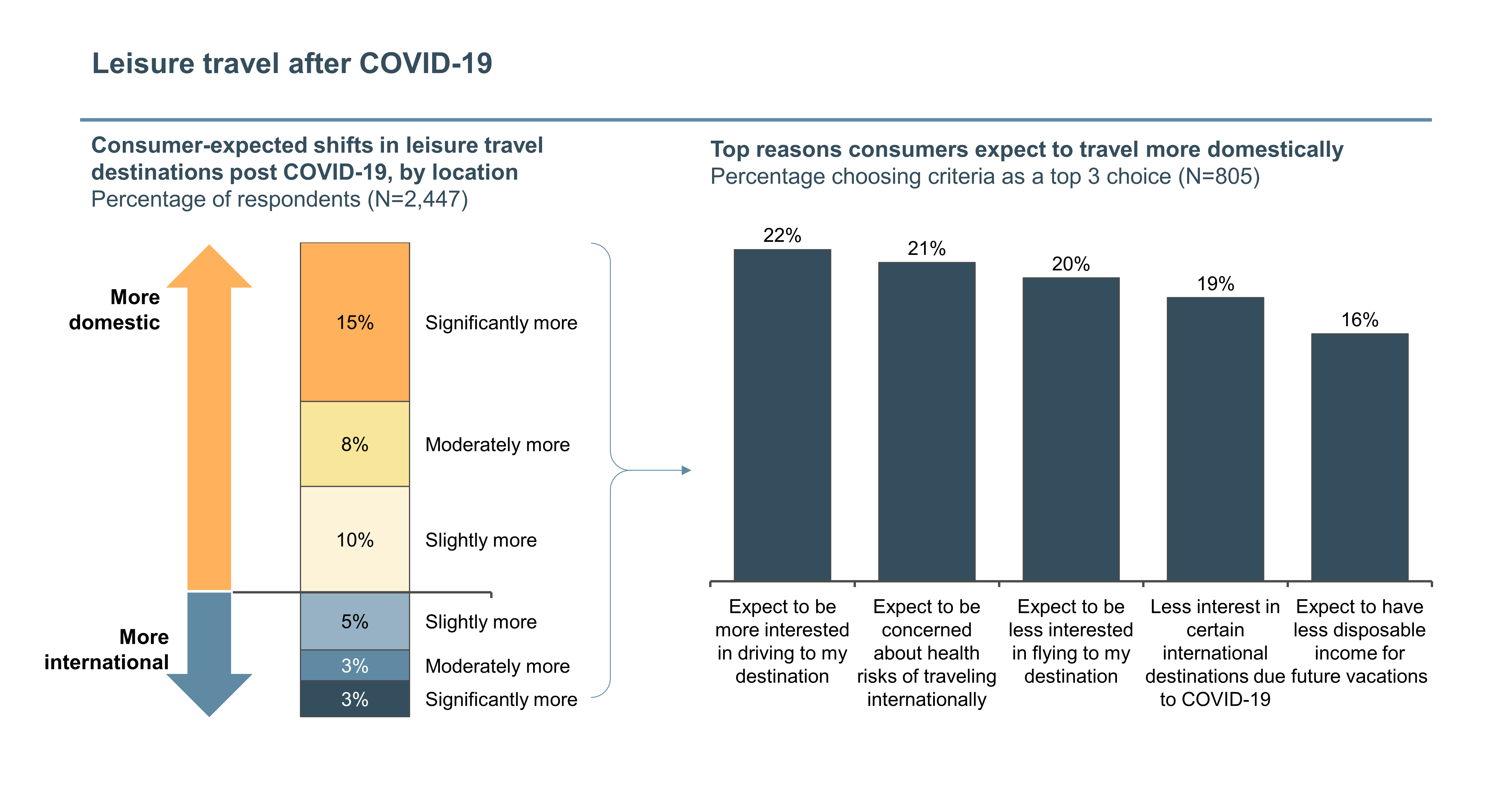

Finally, consumers expect COVID-19 to shift their long-term leisure travel behavior, both in where they go and what they do.

Approximately ~33% of consumers expect their travel to be more domestic post-COVID-19, most often because they expect to prefer to drive (rather than fly) to their destinations and will likely remain concerned about the health risks of international travel.

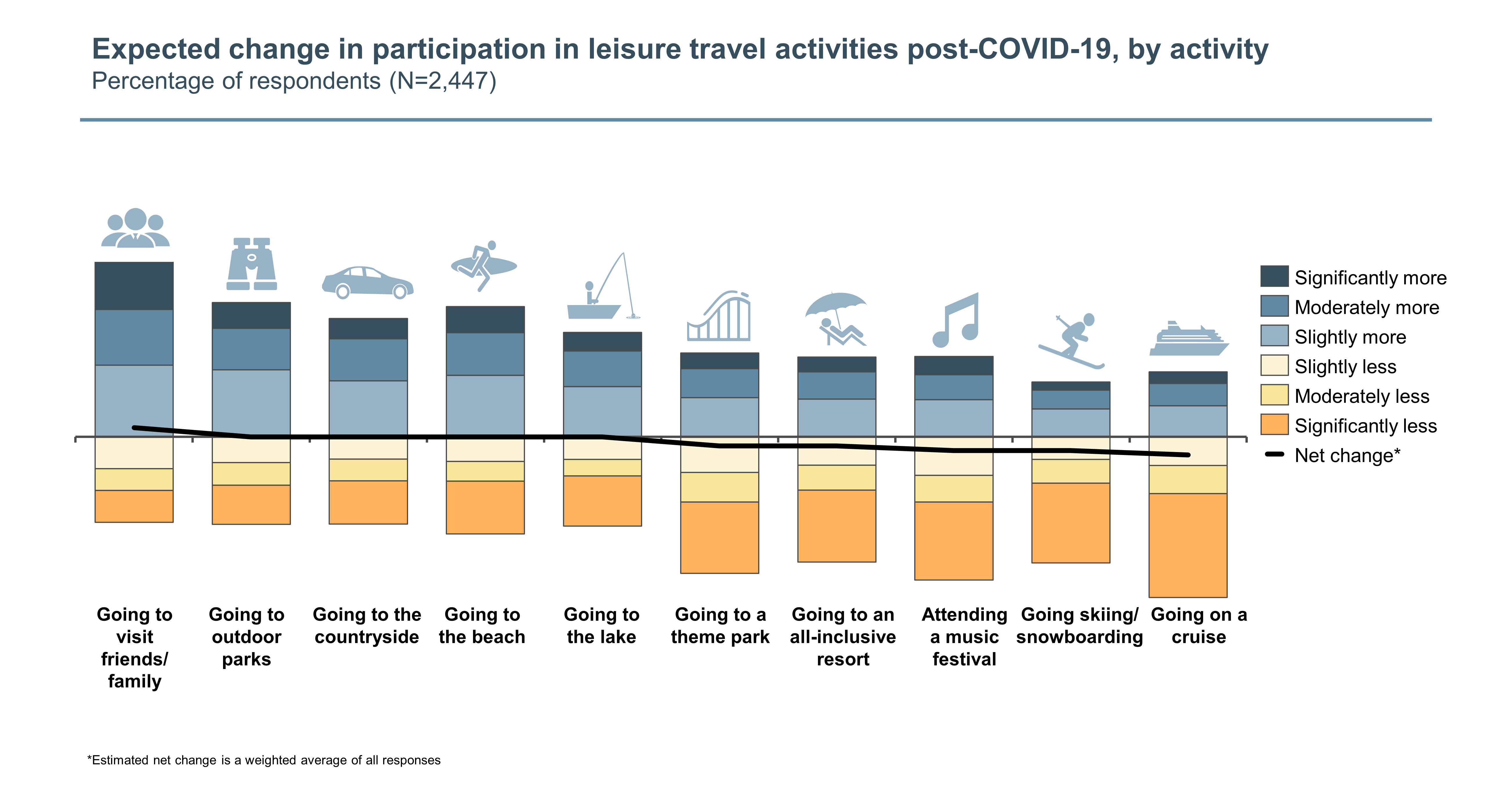

Health concerns are also expected to affect consumers’ long-term leisure travel activity choices, even domestically. Consumers plan to participate in “distance-able” leisure travel activities a similar amount or more often once the outbreak is contained, but expect to reduce frequency of travel to more crowded locations.

Participation in activities like visiting family/friends and going to parks, beaches, lakes or the countryside is expected to remain relatively consistent relative to pre-COVID-19 levels, while travel involving cruises, music festivals and all-inclusive resorts is expected to incrementally decline as consumers continue to seek out safer vacation options, even once COVID-19 is contained.

As a reminder, this is the final pulse survey in our COVID-19 Consumers Insights Series.

We understand that many of our clients are facing new disruptions and increased uncertainty in their business outlook. Some of these changes are likely to endure well beyond the end of the current pandemic. While many of these changes will create challenges, there will also be new opportunities that emerge. We will continue to share our ideas and insights through our website and other media over the coming months.

We wish good health and a happy holiday season to you and your loved ones, and we look forward to continuing to support our clients through this difficult time.

To continue the discussion, please don’t hesitate to contact us.

Lauren DeVestern, Principal at L.E.K. Consulting, co-authored this report.

Lauren DeVestern, Principal at L.E.K. Consulting, co-authored this report.