Scaled providers can benefit from a shift toward more centralized purchasing

For all but the smallest organizations (i.e., fewer than six locations), speed, consistency and national reach are crucial as the company continues to shift toward centralized purchasing. That’s why going forward, scale is expected to become an increasingly important differentiator when it comes to choosing a service provider.

Unsurprisingly, it’s all relative. Larger organizations tend to be more interested in national scale as it offers them greater potential for realizing benefits across a larger number of locations. Smaller organizations, on the other hand, have less upside — and less incentive — to standardize across their network, and instead tend to be more interconnected among their individual locations relative to their larger peers.

So when considering salesforce structure, service providers are likely best positioned to win with national/key account managers focused on large customers. The more localized the customer, the more they favor localized providers, ideally those with local/regional sales representatives who prioritize customers that have five or fewer locations. Of course, there are exceptions to these broad rules of thumb, but these guideposts can provide a starting point of focus.

Digital has become a core retainment and growth tool

Providers that make tools such as online work order management, digital inspection reports and automated billing part of their core service model are better positioned not just to win clients, but also to retain them.

Digital offerings for work order management and billing/payments, as well as inspection and reporting tools such as apps and photo-based inspection capabilities, are already common and are highly valued by customers. To remain competitive going forward, service providers need to continue investing in these features.

Client portals, digital communication and scheduling tools are less frequently offered today but are of interest to commercial building managers. As such, these options present a way for service providers to differentiate themselves.

With trust comes cross-selling potential

Facilities managers are now willing to consider multiple services from providers who are able to reliably deliver said services — so long as they have shown they can deliver. Indeed, the trust-in-delivery factor seems more important than the level of expertise.

Our previous research on residential cross-selling opportunities, Bundling Opportunities in Residential Services, showed that in addition to trust, convenience and expertise were also factors. This suggests that while there is a cross-selling opportunity in residential services, the opportunity is arguably even greater in facilities services.

Challenges remain

As our survey makes clear, scale offers providers a host of advantages. But they’re still faced with a number of challenges.

Sales reps are reactive.

Facilities managers report being generally happy with their sales reps, but those reps tend to be reactive, which leaves the door open for a commercial excellence-driven competitor to succeed.

Digital differentiation is increasingly difficult.

Differentiating through digital is becoming harder now that basic digital features have already been widely adopted. But other, less developed digital offerings such as client portals and real-time scheduling aren’t as frequently offered by providers despite being viewed as high value.

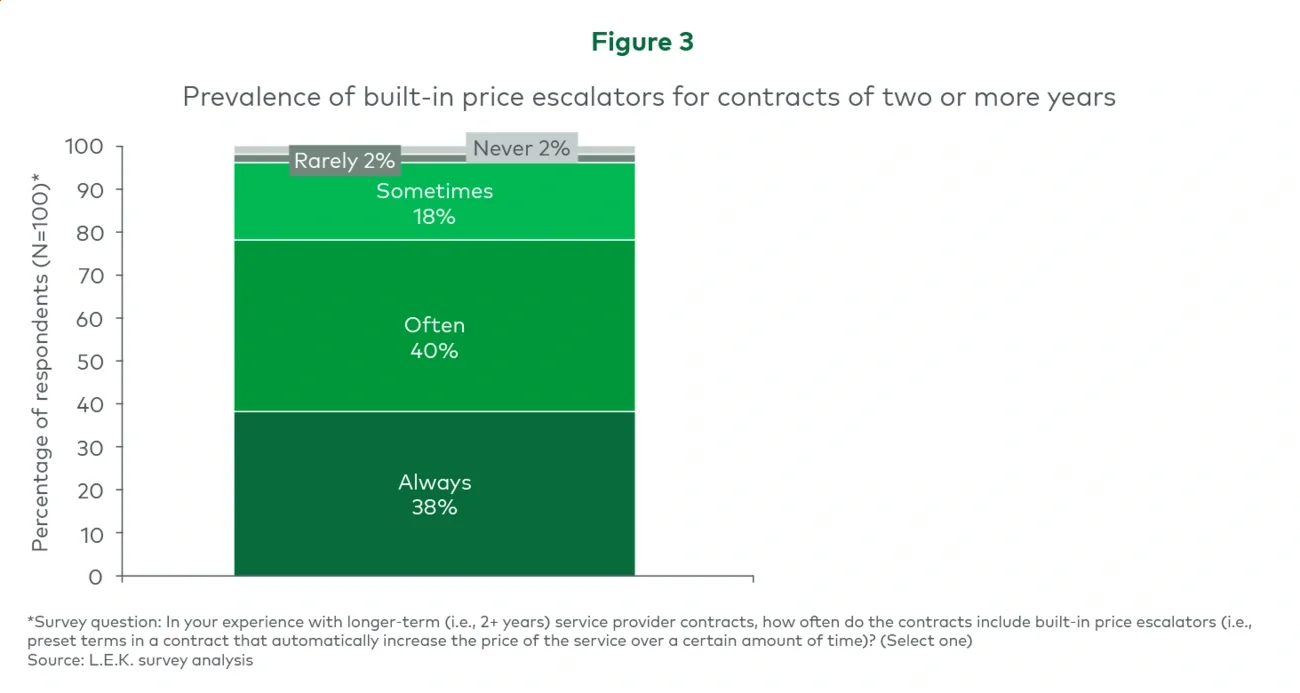

Broader business risks persist.

Rapid price changes are always possible due to tariffs and immigration/labor shortages, for example. Geopolitical uncertainties aside, escalators are a recommended best practice. Many providers, though by no means all of them or for all of their contracts, already have these in place (see Figure 3).