With the holiday market in remarkably good shape, the forecast is fair for travel in 2023.

Decline in the travel industry was a very clear and obvious symptom of the Covid-19 pandemic. Closed borders and locked-down households disrupted holiday plans, leaving travel businesses across the industry struggling in 2020 and 2021.

Fortunately, 2022 featured a welcome recovery in spending, with Barclaycard data showing growth at 116% of the previous year’s spending. Reopening borders was a major impetus for this recovery, but inflation clearly played a part too, and overall volumetric levels do remain below pre-pandemic levels in 2019.

See our UK Travel Trends Infographic for greater insight into the positive outlook for the 2023 UK holiday market.

This reality leaves recovery fragile and potentially hostage to the impact of the ongoing cost-of-living crisis. Rising prices are forcing consumers to make significant cuts to both discretionary and essential spending, and non-essential travel is under pressure as a relatively large discretionary spend category. Recent data from an October 2022 Post Office poll highlights a noteworthy 42% of consumers believing that the rising cost of living will impact their holiday plans with cuts to their budgets and bookings to cheaper destinations.

Nonetheless, sentiment is changing fast, and newer data paints a more encouraging picture, with a survey commissioned by Hilton indicating that a sizeable majority of Brits — 59% — plan to travel more in 2023 than they did in 2022. At the close of 2022, TUI forecast sales for 2023 would hit 2019 levels. A poll by EasyJet indicates that 70% of UK consumers are ready and willing to prioritise vacations over other spending, signifying a growing trend for consumers to regard holidays as an increasingly essential part of their discretionary spend.

This re-prioritisation of holidays is occurring across the industry, where strong trading data supports the trend. UK travel company Travel Counsellors reported January 2023 sales of £114m, its highest ever for the month and a noteworthy 50% increase on pre-pandemic levels in January 2019. Ryanair delivered similarly positive news for the sector, reporting profits of €211m for October to December 2022 — almost three times the 2019 level — and a 7% rise in passenger numbers for Q4 versus the same period in 2019.

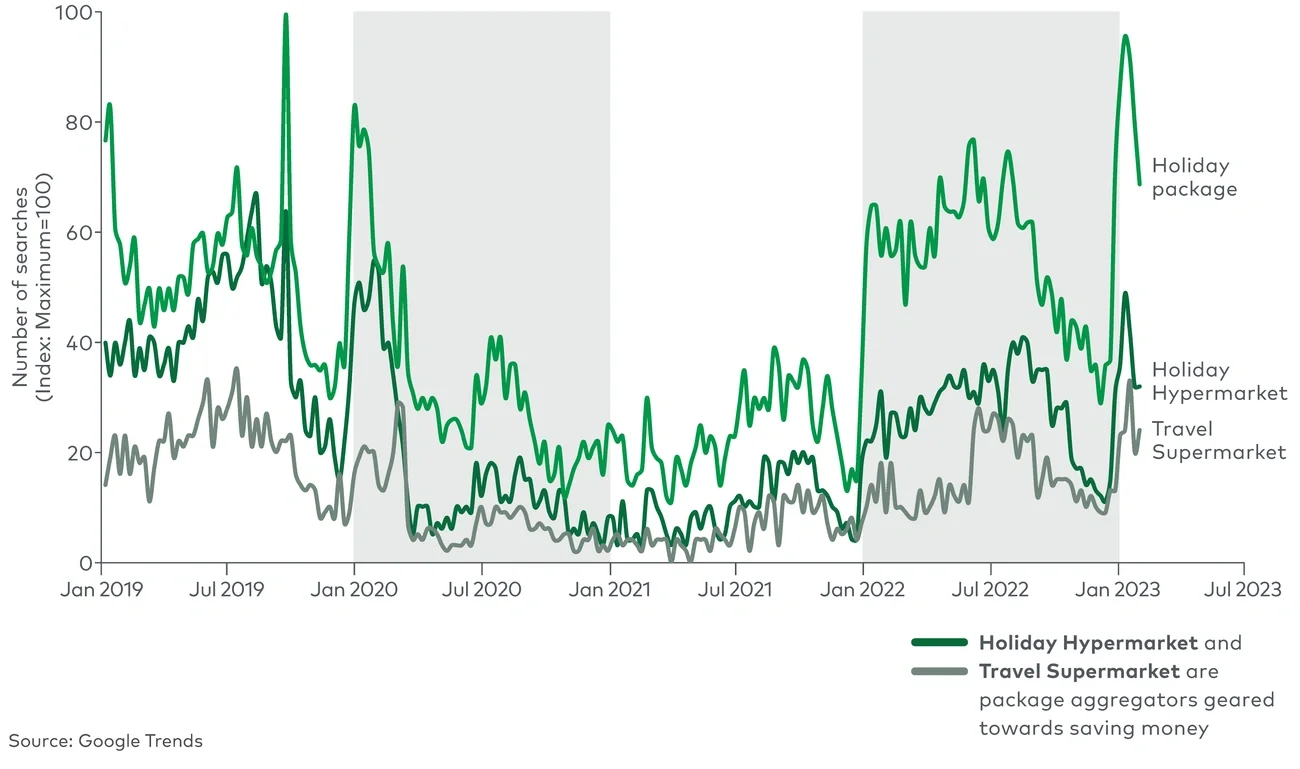

There is good news online too, with Google searches for key holiday terms such as ‘Holiday package’ and ‘Travel supermarket’ both exceeding 2020 levels with increases of 16% and 57%, respectively (see Figure 1).