Qualcomm stands at a strategic inflection point. The mobile chipmaker relies on Apple for nearly 20% of its revenue, but Apple is developing its own modem and will likely stop using Qualcomm chips by 2026. With its core smartphone business stagnating amid Apple’s dominance, Qualcomm must identify new avenues of growth. The company sees edge computing as its bridge to the future. In this article, L.E.K. Consulting explores Qualcomm’s history, the potential of edge computing, and whether a pivot can allow Qualcomm to continue its growth trajectory.

Qualcomm’s history: From wireless pioneer to mobile chip dominance

Founded in 1985, Qualcomm pioneered code division multiple access (CDMA) technology, allowing multiple cellular users to share spectrum bandwidth efficiently. This breakthrough enabled the transition from analog to digital networks and laid the foundation for the mobile revolution.

Throughout the 1990s and 2000s, Qualcomm continuously innovated in wireless technologies like 3G, 4G and 5G. It also established a lucrative patent licensing business, charging royalties on its intellectual property. By the 2010s, Qualcomm was the clear leader in mobile processors. Its Snapdragon chips powered premier devices across Android smartphone makers like Samsung, Google and Xiaomi.

However, Qualcomm also became embroiled in multiple legal skirmishes over its licensing practices. Companies argued that Qualcomm abused its dominance in critical wireless patents. Most notably, Apple sued Qualcomm in 2017 for charging excessive patent royalties. The companies ultimately settled in 2019, but the rift remained.

The core mobile chip business, which counts Apple as a major customer, generates over half of its profits. This heavy Apple reliance puts Qualcomm in a precarious strategic position. Qualcomm’s stock price has reflected these concerns, with its valuation declining over 30% from its 2018 peak amid stagnating growth.

Meanwhile, Qualcomm has doubled down on its investments in the connected intelligent edge. The company has focused on building core businesses in the automotive industry, networking infrastructure, the Internet of Things (IoT) and the personal computer market.

Earlier this year, Qualcomm unveiled its new Snapdragon Elite X processor for PCs, which stems from its 2021 acquisition of Nuvia. Qualcomm claims this product outperforms the fastest laptop chips from Apple and Intel and may help Qualcomm take more share in the PC processor market. With offerings like the Elite X, it’s only a matter of time before OEMs and independent software vendors (ISVs) broaden their processor options beyond Intel and AMD. This is important so that OEMs and ISVs gain more control over their innovation cycles for future product releases.

Qualcomm must find its next act to reignite growth and satisfy shareholders seeking improved returns. But does edge computing represent the opportunity Qualcomm needs?

The edge computing revolution

Edge computing refers to processing data near the “edge” of the network, close to the user and the originating devices, rather than sending vast amounts of data to distant centralized data centers. Edge computing enables real-time insights and actions, reduced costs, enhanced security and lower latency.

What’s driving the edge computing explosion? Several interconnected technological and business trends:

-

The rollout of 5G networks (and eventually 6G) with higher speeds and lower latency that can support edge computing use cases

-

Advances in Wi-Fi standards pushing more toward lower-latency machine-to-machine communications requirements

-

Proliferation of SDx that simplifies deployment of advanced enterprise networking solutions through separation of control and data planes

-

Billions of new connected IoT devices generating data that needs local processing

-

Artificial intelligence (AI) and machine learning applications that crunch data and deliver intelligence in real time

-

Cloud computing limitations like bandwidth constraints, latency and privacy concerns

-

The need for instant insights and actions in industrial environments or augmented reality

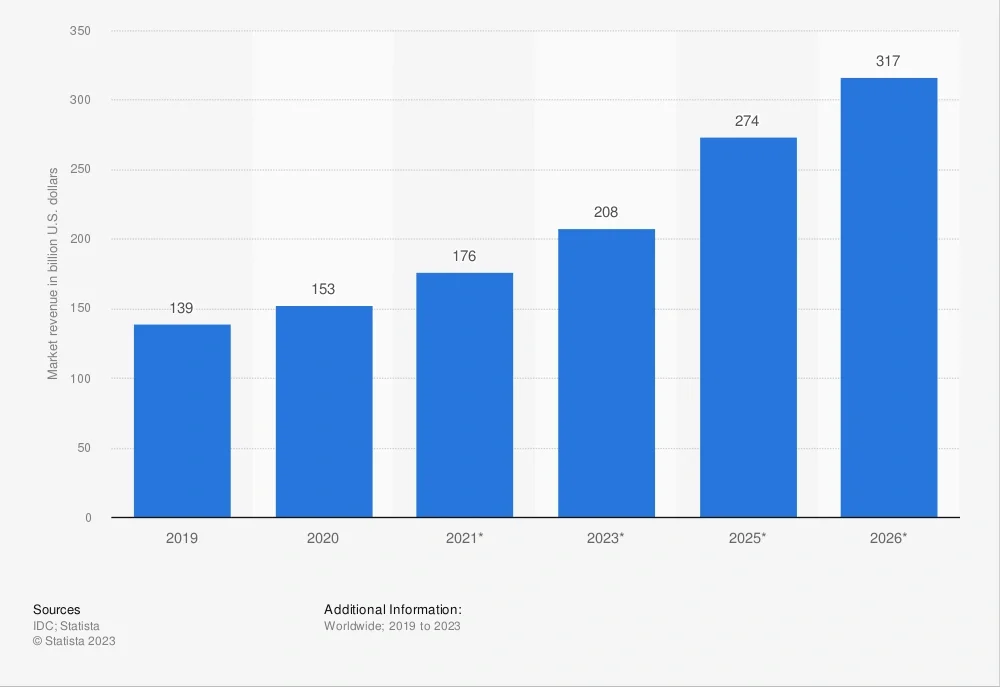

According to IDC, the edge computing market will reach $250 billion by 2024. Nearly every industry from manufacturing to retail to healthcare can benefit from decentralized computing power. Edge resources can complement cloud computing in a hybrid architecture tailored for different application requirements (see Figure 1).