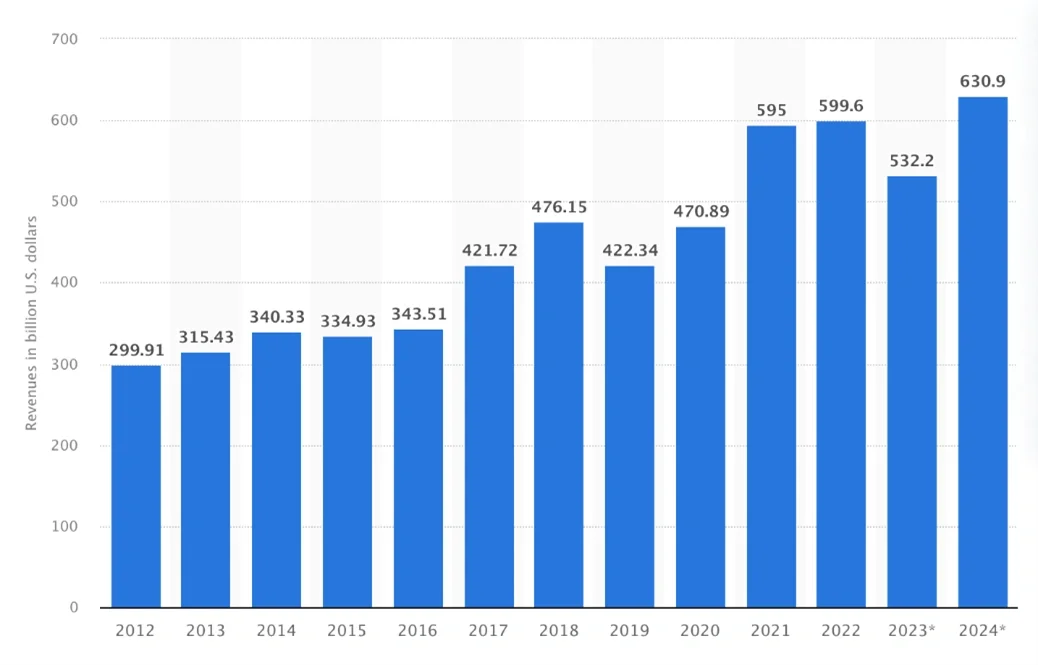

Source: Statista

In this edition of Executive Insights, we will delve into the intricacies of the chip shortage, explore the competitive landscape of the industry and examine how NVIDIA has navigated these challenges and emerged as a key player in the GPU market.

The roots of the chip shortage

The global chip shortage is rooted in a blend of intertwined factors, painting a picture of an unprecedented supply-demand imbalance.

The digital transformation wave that began gaining momentum in the 2010s amplified the demand for semiconductors, with sectors from automotive to healthcare becoming increasingly reliant on chip-enabled technologies. The COVID-19 pandemic in 2020 created an unexpected surge in chip demand as businesses shifted to remote working and consumers increased their reliance on personal electronics. Simultaneously, the pandemic disrupted global supply chains, leading to severe production constraints.

Geopolitical tensions further complicated the situation. Tensions, particularly between the U.S. and China, have stoked fears of restricted access to semiconductor technology, leading companies to stockpile chips. Moreover, rapid advancements in chip manufacturing technologies have rendered older production lines obsolete, contributing to the chip shortage.

Industry analysts believe the chip shortage may be starting to ease. As the post-pandemic supply chain continues to stabilize, semiconductor production is catching up with demand. However, semiconductor procurement timelines suggest that the industry is not out of the woods yet; lead times for basic semiconductors still exceeded 40 weeks in early 2023, with high-end components pushing 50 weeks.

Competitive landscape

The chip market is fiercely competitive, with key players striving for dominance and technological superiority. Let’s explore the competitive landscape and some of the prominent companies in this space.

AMD

A significant competitor to Intel in high-performance computing, AMD strengthened its position with the acquisition of Xilinx in 2021. This expansion allows AMD to offer integrated solutions combining high-performance central processing units (CPUs) and programmable logic devices.

Intel

Intel remains a major force in the traditional CPU market, known for delivering reliable and powerful processors for PCs and server systems. Intel is investing in research and development to address competitive gaps and explore emerging technologies like AI, edge computing and autonomous systems. Furthermore, its plan to decouple from its historically integrated manufacturing model is expected to unlock more innovation.

Qualcomm

A leading provider of processors for mobile devices, Qualcomm extends its reach from the mobile chip market to other sectors such as automotive, Internet of Things (IoT) and networking. Its focus on connectivity and low power consumption positions it well for the growing demand for connected devices and the IoT.

TSMC

The world's largest independent semiconductor foundry, TSMC manufactures chips for companies like AMD and NVIDIA. With advanced fabrication processes, TSMC enables customers to design high-performance chips for various applications, from consumer electronics to data centers.

Broadcom Inc.

With expertise in semiconductor design and infrastructure software solutions, Broadcom serves diverse markets, including data centers, networking and wireless. Its focus on high-performance and energy-efficient solutions has earned it a strong market presence. Broadcom is known for acquisitions that expand its capabilities, such as the $18 billion purchase of CA Technologies in 2018.

Micron Technology Inc.

A leader in producing semiconductor devices, Micron specializes in NAND, DRAM and NOR flash memory. Its memory solutions power a wide range of applications, meeting the increasing demand for high-capacity and high-speed memory in various industries. Micron manufactures memory chips at fabrication plants in the U.S., Asia and Europe.

ARM Holdings

Known for designing energy-efficient processors that power many smartphones and mobile devices, ARM is known for licensing its chip architecture designs. ARM’s reduced instruction set computer (RISC)-based designs are valued for their power efficiency, making them ideal for mobile applications. The company continues to innovate in areas like AI, 5G and autonomous vehicles.

RISC-V

Originally developed at UC Berkeley, RISC-V is an open-source hardware instruction set architecture and is freely available under open-source licenses. RISC-V was recognized by the MIT Technology Review as one of the 10 breakthrough technologies of 2023 for its potential to democratize chip design through its open standard architecture, which makes chip designs inexpensive and easy to license.

The rise of NVIDIA

NVIDIA, founded in 1993, began its journey as a provider of graphics accelerator cards, becoming renowned for its expertise in GPUs. Recognizing the potential of parallel processing in GPUs to accelerate general computation, NVIDIA made a pivotal strategic move in 2007 with the launch of CUDA, a software platform that allows developers to use NVIDIA’s GPUs for general-purpose processing. This shift allowed GPUs, traditionally used for rendering images, to become powerful parallel processors capable of handling complex mathematical computations and machine learning tasks.

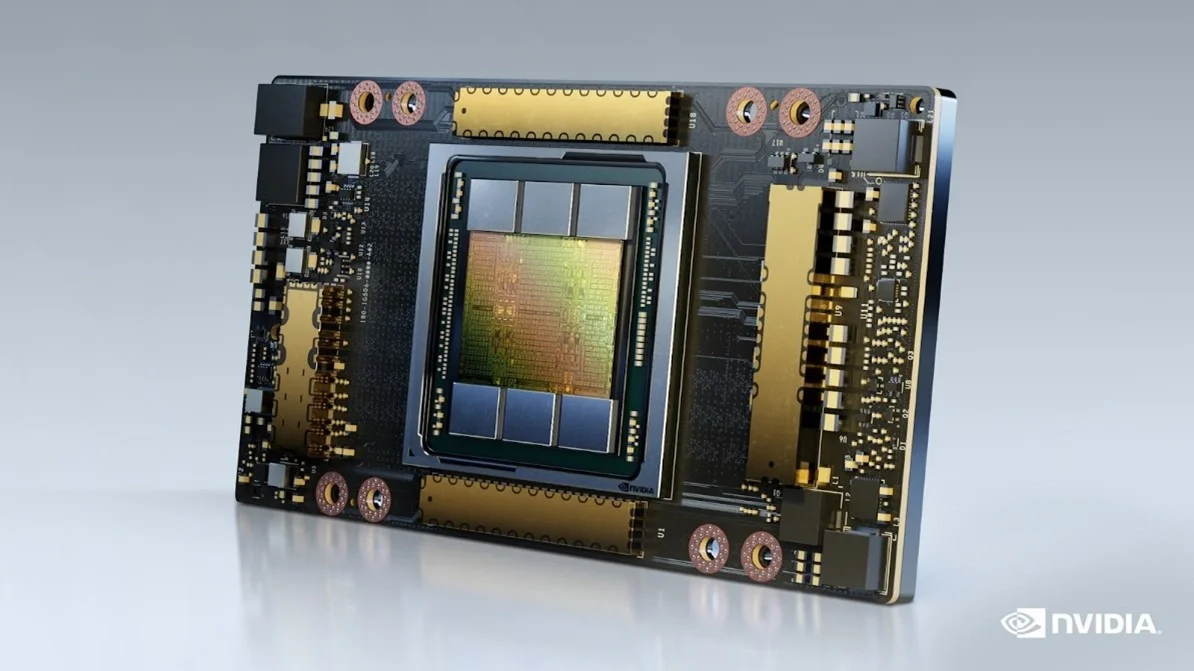

In recent years, NVIDIA has established its GPUs as the preferred hardware for AI workloads, capitalizing on the parallel processing capabilities of these chips for machine learning applications. The company’s comprehensive ecosystem of software and tools further facilitated the utilization of its GPUs by developers in AI workloads. In May 2020, NVIDIA introduced the A100 GPU, a powerful and versatile chip that revolutionized the landscape of high-performance computing and the rapidly expanding field of AI and machine learning (see Figure 2). With its groundbreaking capabilities and unprecedented performance, the A100 propelled NVIDIA to the forefront of the AI space, solidifying its position as a pioneering force in the industry.