The rising need for OT cybersecurity

The convergence of operational technology (OT) and information technology (IT) has dramatically increased cybersecurity risks in critical infrastructure sectors such as energy, transportation, utilities, telecommunications and manufacturing. Once isolated from external networks, OT systems are now increasingly connected, exposing them to cyber threats — including power outages, production shutdowns, supply chain disruptions and safety hazards — that could have catastrophic consequences.

OT security refers to the protection of industrial control systems, supervisory control and data acquisition (SCADA) systems and other critical infrastructure technologies from cyber threats. Unlike traditional IT security, which safeguards data and networks, OT security focuses on securing physical processes and machinery in the aforementioned sectors.

Several factors are accelerating the demand for OT-focused cybersecurity services, making it an attractive investment opportunity:

- IT/OT convergence: As industrial systems integrate with corporate IT networks and cloud solutions, they inherit the vulnerabilities of digital networks, demanding sophisticated security measures.

- Regulatory pressure and compliance requirements: Governments worldwide are tightening cybersecurity mandates for critical infrastructure — such as through the NIS2 Directive (EU), EASA cybersecurity standards in aviation (EU) and NIST-CSF (US) — driving mandatory investments in cybersecurity services.

- Rising cyber threats: The increase in geopolitical cyber threats has elevated cybersecurity as a boardroom priority. Germany’s recent €500 billion infrastructure spending announcement directly amplifies the demand for OT-focused cybersecurity services, particularly in critical infrastructure sectors.

- Cyber insurance evolution: Insurers are enforcing higher cybersecurity standards for OT-heavy industries, requiring security assessments, incident response planning and ongoing monitoring as part of their underwriting process.

- Talent shortage in OT security: OT cybersecurity expertise remains scarce, pushing companies to outsource cybersecurity services, driving growth in professional and managed security service models.

This edition of L.E.K. Consulting’s Executive Insights highlights why this space presents a high-growth opportunity for investors. It also details why cybersecurity for industrial and critical infrastructure is not just a necessity but a regulatory and operational imperative.

Pockets of opportunity

Segments in the professional cybersecurity services market

The cybersecurity landscape is experiencing strong growth, presenting an £8-10 billion market opportunity in professional cybersecurity services in Western Europe alone — expanding at 10%-12% per annum. OT-heavy industries such as manufacturing, energy and critical infrastructure are driving 20%-30% of this total cybersecurity spend.

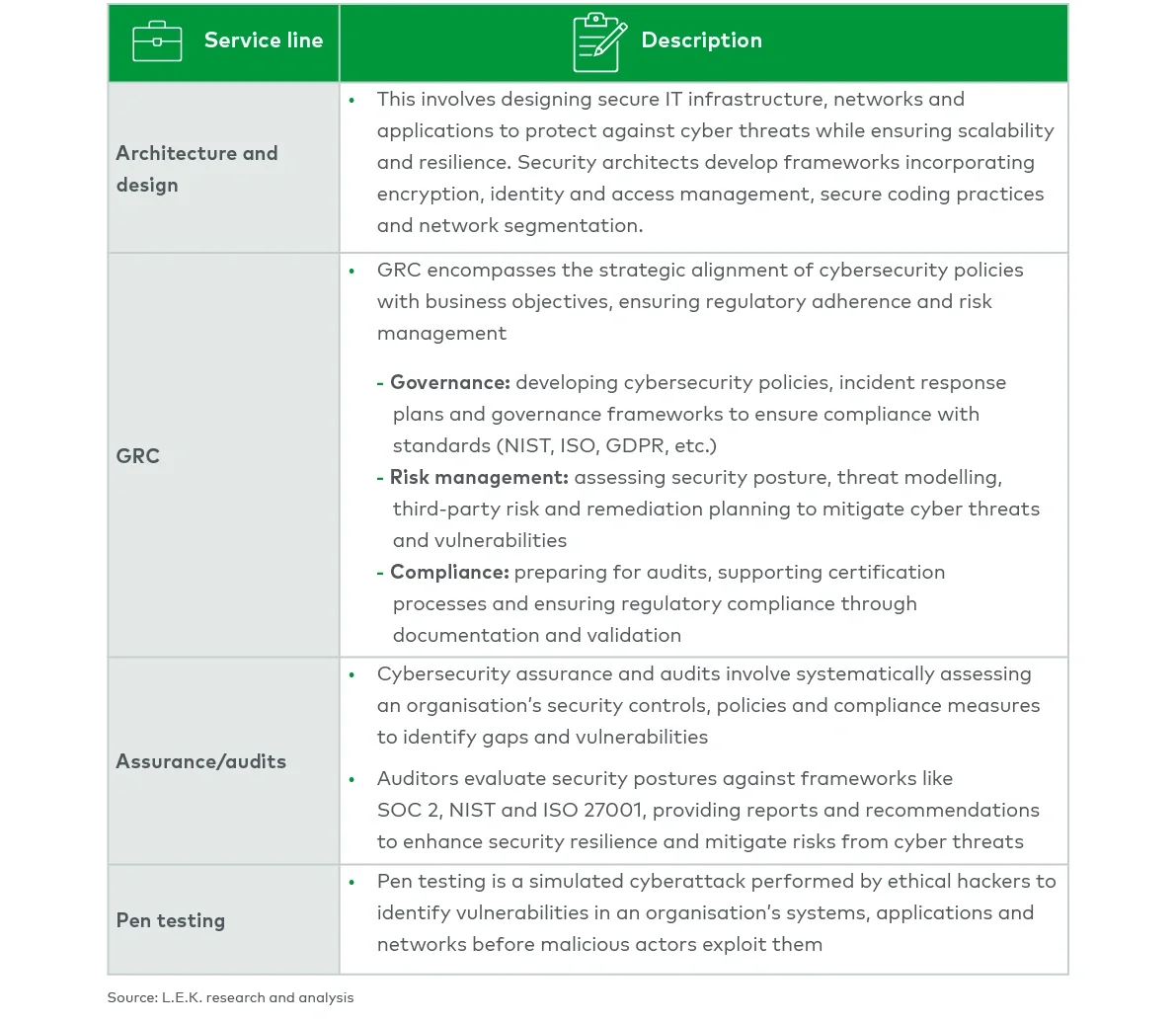

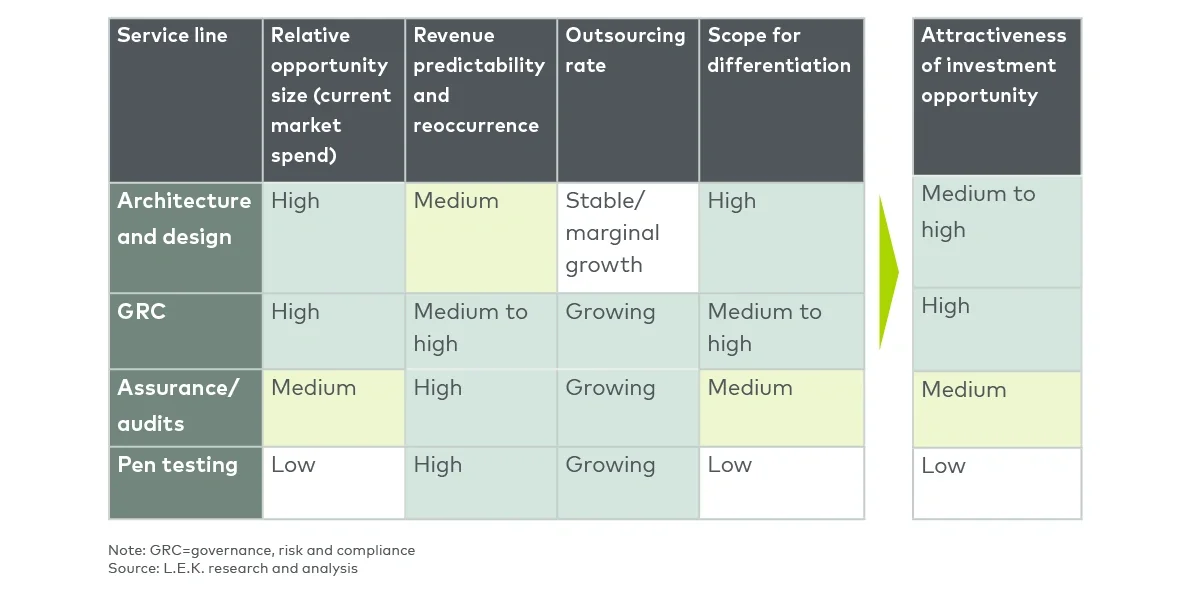

To better understand where the most attractive opportunities lie, professional cybersecurity services can be segmented into distinct service lines, each addressing critical aspects of cybersecurity risk management, compliance and resilience. Below, we break down the core professional cybersecurity service categories and their value propositions (see Figure 1).