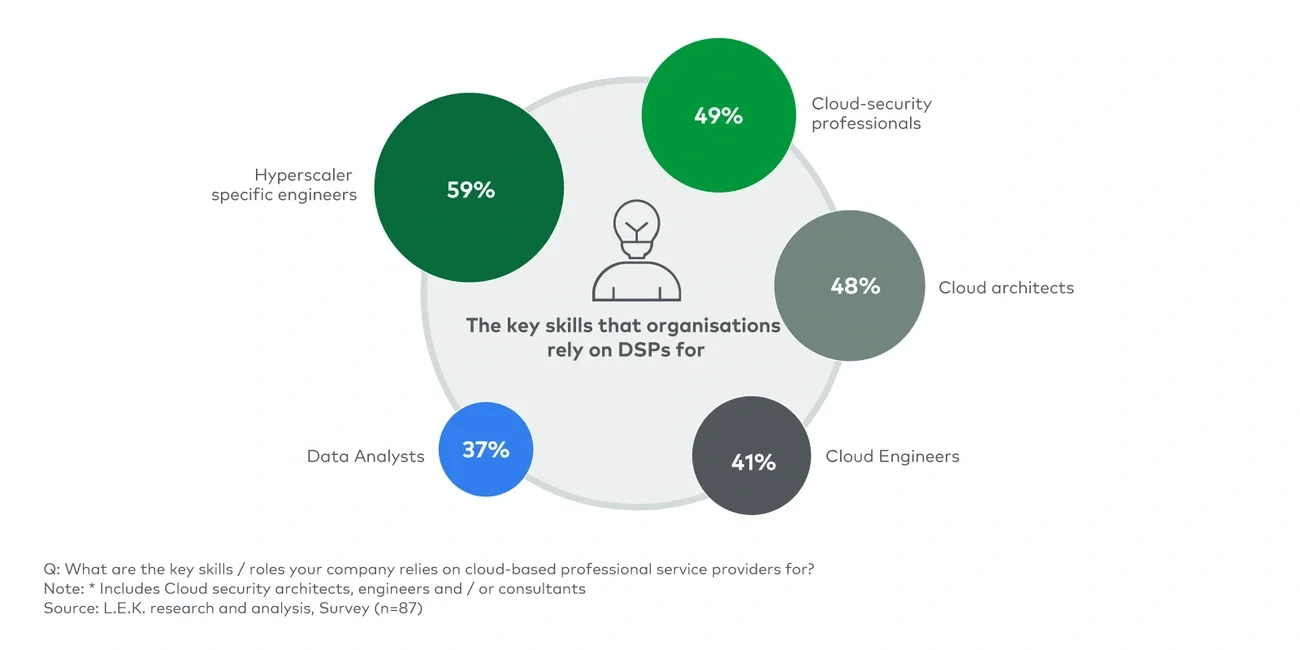

Specialist DSPs have had ongoing challenges in finding and retaining high-quality digital talent, particularly cloud, data and security experts. Although specialist DSPs are attractive employers for many of these professionals, global Big Tech companies and local digital leaders have invested heavily over the past few years in building and expanding their own digital specialist teams, while start-ups and institutional corporates have also competed for top talent.

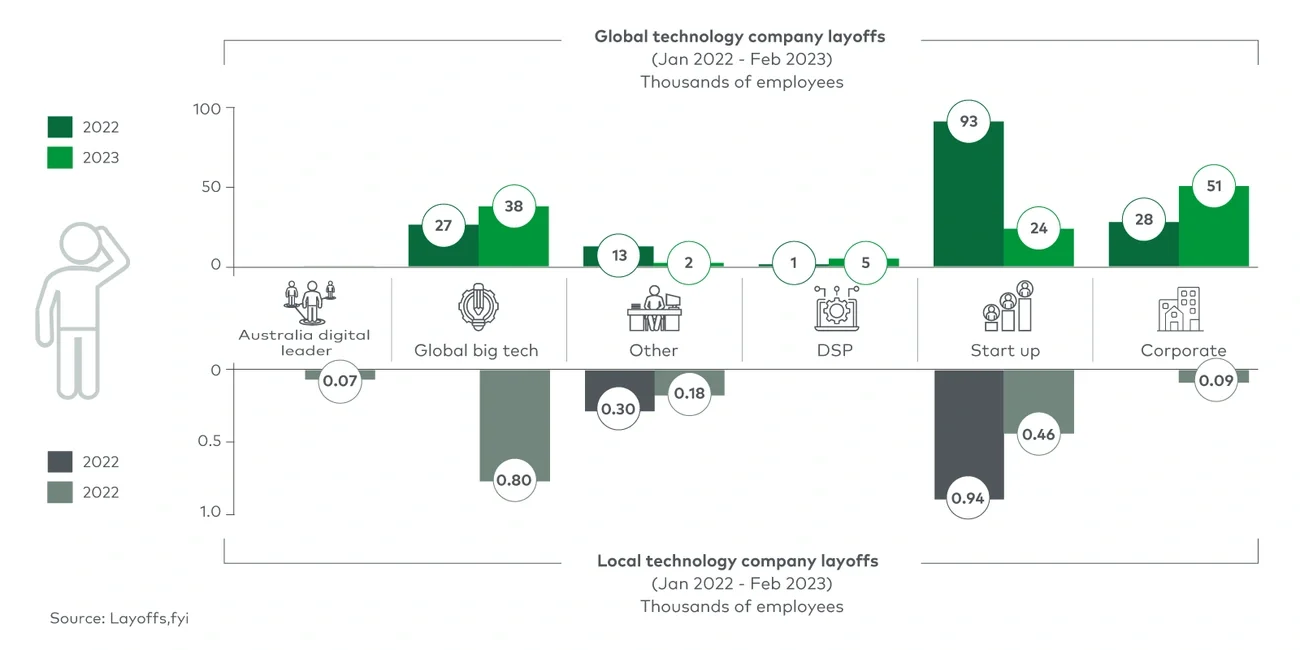

Covid-19 created a spectacular talent shortage in 2020 and the two subsequent years, driving up employment costs for many specialist DSPs. However, recent months have seen technology organisations shake up their operations in the post-Covid world, with many reducing the staff numbers they had at the height of the pandemic.

Can this new talent surplus in the market help specialist DSPs improve their position as employers of choice, to attract and secure the very best employees? How can they differentiate themselves to these candidates in a still-competitive hiring market? And what do they have to do inside their organisations to present their best face to this talent?

In this, our second article on specialist DSPs, we review the current digital talent landscape in Australia. In particular, we examine the wave of recent layoffs across the sector and discuss the potential implications for those specialist DSPs that are looking to build up their own teams, and for the investors funding many of these businesses.

Pre-Covid, a tight talent market

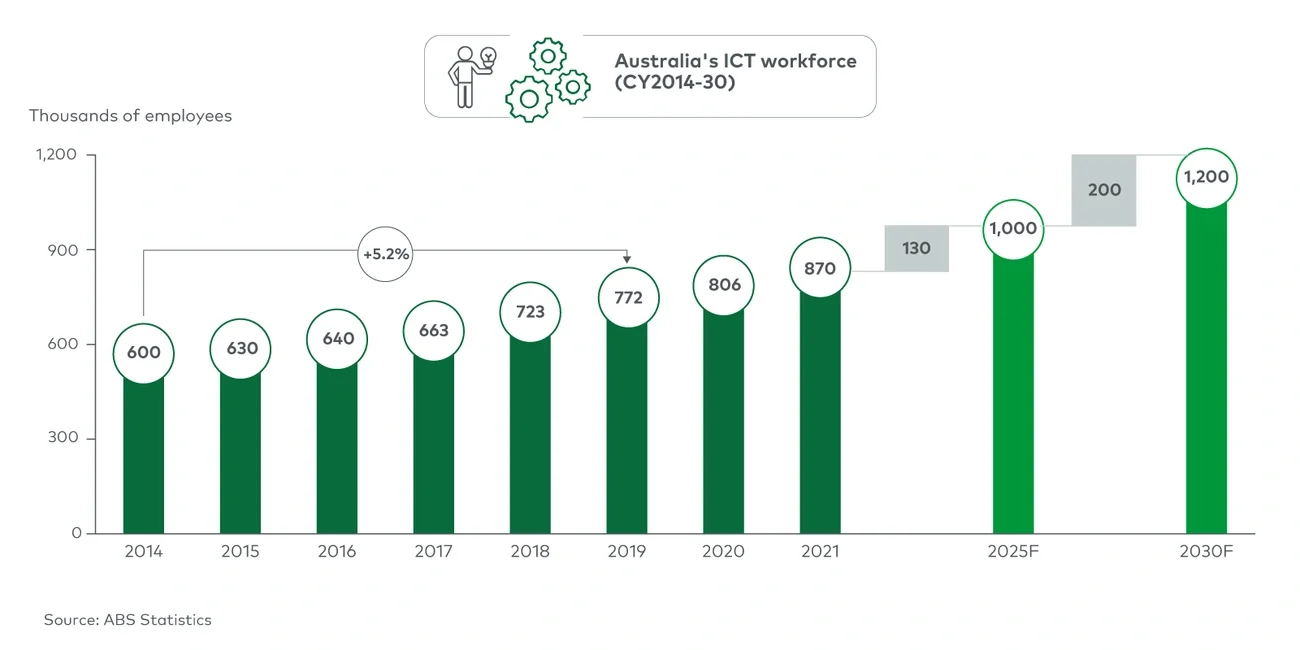

Even before the Covid-19 pandemic, Australian businesses found it hard to attract and retain high-calibre digital talent. This was despite Australia’s information and communications technology (ICT) workforce growing at an annual rate of 5.2% between 2014 and 2020; by 2019, the ICT workforce was over 772,000 strong,1 consisting of a mix of local talent and skilled immigrants.

Alongside the annual growth of national ICT talent, the IT sector has accounted for about 20% of Australia’s tertiary graduates in the science, technology, engineering and mathematics (STEM) disciplines. Meanwhile, the digital services sector has been growing at 10%-20% per annum, as have other markets such as the Infrastructure as a Service (Iaas) and Platform as a Service (PaaS) sectors.

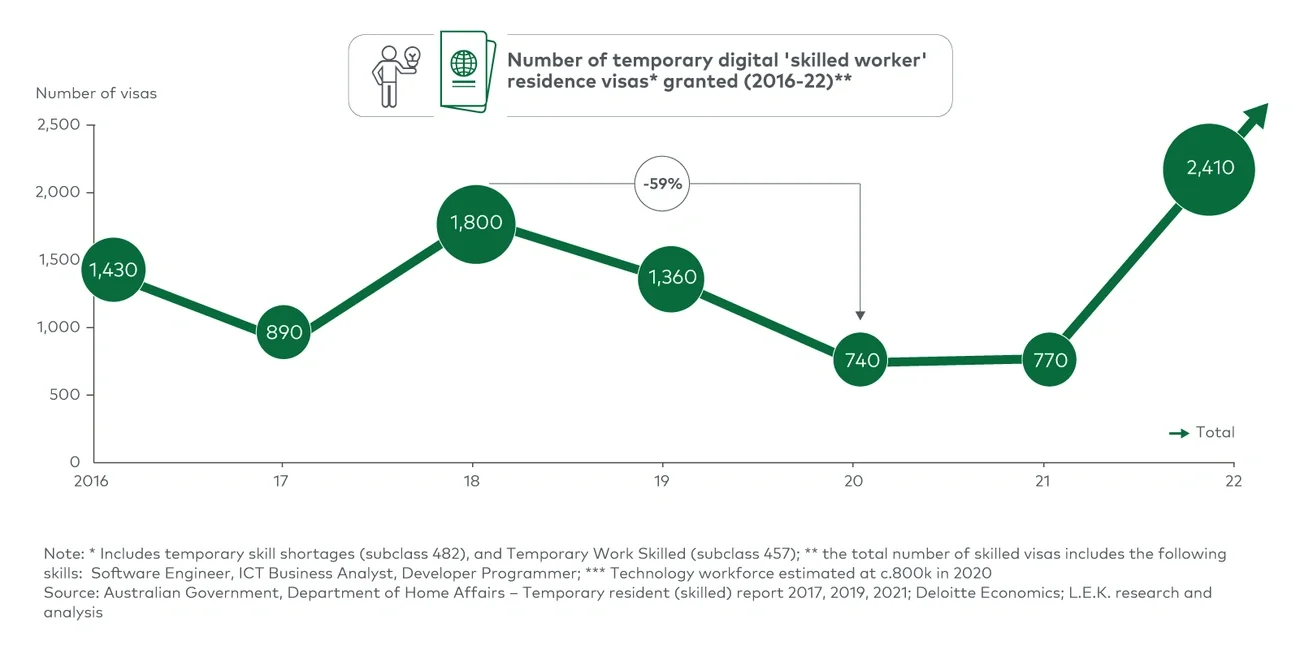

By the second half of the 2010s, this created a shortfall of local talent, along with an influx of skilled digital consultants entering Australia to fill the gap. In each of these years, nearly 1,200 ICT-specific staff entered the country to join the labour market, mostly software engineers, developers, programmers and ICT business analysts.

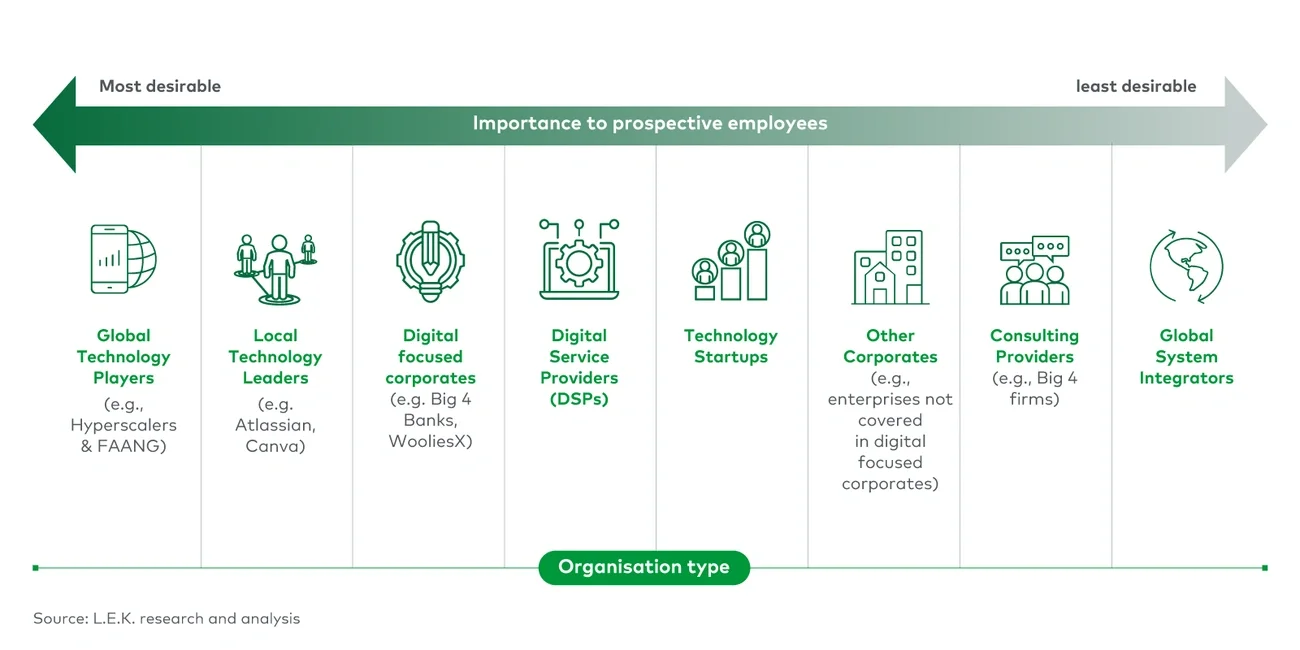

However, despite this influx, specialist DSPs were not the first choice for all prospective employees at an ‘expert’ level. Our research, summarised in Figure 1 below, shows that they ranked middle of the employer pack in candidates’ eyes, behind the Big Tech companies (for example, AWS and Google) and local tech leaders like Atlassian and Canva. These market leaders offered the allure of a strongly branded employer that could provide interesting work opportunities along with attractive compensation packages, equity (in some cases) and other competitive, non-remunerative benefits.

Specialist DSPs also sat just behind the digitally focused corporates such as leading national banks, but were still ahead of start-ups, larger ASX-listed corporates, larger broad-service digital consultancies and global systems integrators.