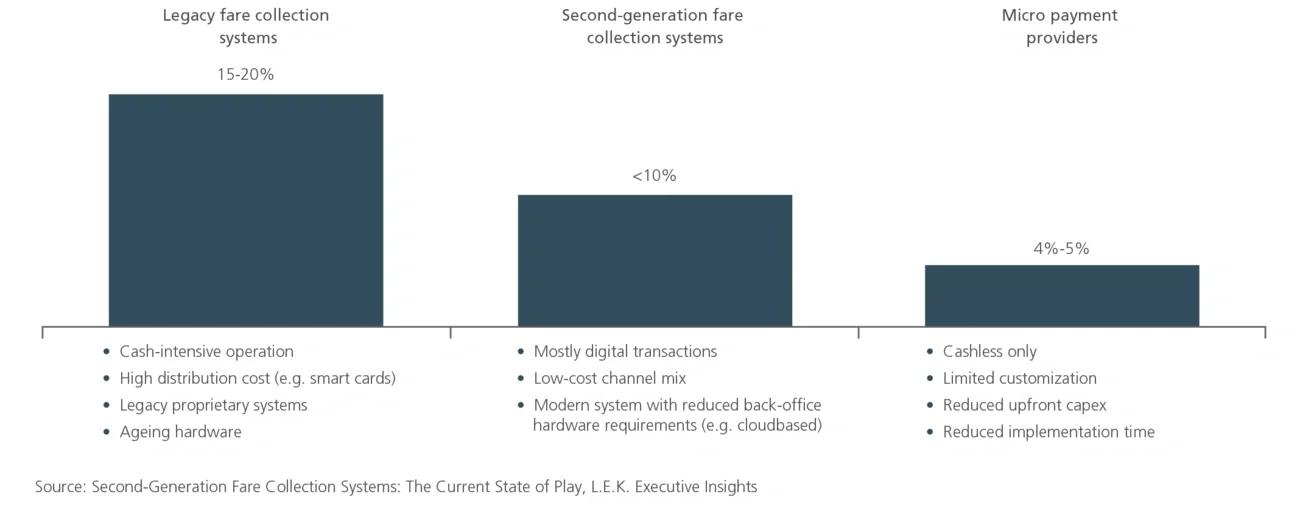

In a recent Executive Insights, Second-Generation Fare Collection Systems: The Current State of Play , we illustrated the progressive reduction in the cost of fare collection (COFC) tied to the evolution of transit payments (see Figure 1). One of the key considerations associated with minimising the COFC is understanding the ‘cost to serve’ across each of the available customer payment channels and the associated strategy to drive customer behaviour.

Executive Insights

Transit Channel Strategy and the Cost of Fare Collection

Transit Channel Strategy and the Cost of Fare Collection

November 24, 2021

Key takeaways

This Executive Insights explores contemporary considerations associated with unlocking further reductions in the cost of fare collection (COFC), specifically associated with channel management.

The article examines the ‘cost to serve’ across each of the available customer payment channels and the associated strategy to drive customer behaviour.

Consider how the procurement of second-generation (account-based) transit fare collection systems creates an imperative to carefully review customer channel strategy.

Figure 1

Evolution of Transit Cost of Fare Collection

Image

The early wins associated with channel management from a COFC perspective in a smart card world were relatively straightforward — remove high-cost payment channels such as rail station ticket booking offices and progressively remove or reduce ticket vending machines as customers migrated to smart cards and contactless payment. More recently, COVID-19 has provided the opportunity, in some cases, to do away with cash payment (e.g. on buses as a means of eliminating customer-driver interaction).

This paper explores contemporary considerations associated with unlocking further reductions in the COFC, specifically associated with channel management.

COVID-19 has accelerated the pace of cash’s decline faster than even the most bullish projections, with cash usage in 2020 broadly where it was expected to be in 2023. Cash was used for 20.5% of global point-of-sale transactions in 2020, a 32.1% reduction from 2019. This has enabled many transit operators to at least plan for the earlier-than-expected retirement of cash payment.

In August 2017, Singapore’s Land Transport Authority (LTA) announced its intention to eliminate all cash transactions by 2020. This coincided with the successful completion of the LTA’s account-based ticketing (ABT) trial and the associated roll-out of contactless payment channels. However, the LTA has yet to realise its objective of going cashless. Other transit authorities trialled the elimination of cash payment following the 2020 onset of the COVID-19 pandemic (e.g. many bus operators moved to cashless and rear-door boarding to eliminate close contact between passengers and bus operators).

From a transit agency perspective, the motivation to remove cash is clear — cash handling is costly, and operational benefits can be realised through faster bus boarding times, for example.

Despite the strong and accelerating global trend towards cashless payment, the challenge for transit agencies is that cash usage remains sticky for a relatively small group of customers, including some transport-disadvantaged groups that have a strong dependence on transit. It is important to recognise that this is about the strength of preference for cash payment amongst such customer groups and not about whether customers are unbanked. Across developed countries in the Asia-Pacific Economic Cooperation forum, the proportion of adults with an account at a financial institution ranged from 93% (United States) to 100% (Australia, Canada) in 2017.

The message here is clear: Despite the obvious benefits from an operational and COFC perspective, it will be important to move carefully with respect to any proposed total removal of cash payment, although the opportunity and demand to use cash on-system is likely to quickly decline in favour of other payment channels in the short to medium term.

The customer rationale for contactless payment has been very well documented.

From a transit agency perspective, however, the positioning of contactless payment has varied somewhat. For example, Transport for London has sought to aggressively drive contactless take-up at the expense of the Oyster transit smart card. In 2019-20, two-thirds of non-cash payments were made using contactless channels, with the balance made using Oyster. By way of contrast, Sydney also introduced a contactless payment channel alongside the Opal smart card but has positioned this as an additional payment channel to improve customer choice and convenience, alongside physical and digital versions of the Opal smart card. Some 31% of Opal adult trips are made using contactless, and 55% of these use a digital wallet.

While the introduction of new contactless payment channels has clearly unlocked customer convenience benefits, it also requires customers to ensure that they avoid ‘card clash’. This can occur when customers are carrying multiple physical cards in their purse or wallet (i.e. contactless debit or credit and bespoke transit cards). There are multiple issues associated with potential card clash:

- Payment can be taken from a card other than the one intended by the customer

- Customers could be charged two ‘default’ fares (i.e. one to the card used to validate system entry and one to validate system exit)

- A fare might not be charged to a card, leaving the customer exposed to being considered a fare evader

- A fare gate might not open

There are additional considerations for customers using contactless cards.

Firstly, a customer may be able to retrieve only a limited trip history (e.g. if they are using an unregistered contactless card). In Sydney, for example, a customer using contactless payments must register their card to obtain up to 18 months of trip activity. A customer with an unregistered card can only obtain details of the last 10 trips. In London it is possible to retrieve seven days of trip data for an unregistered card and a year of data for a registered card.

Secondly, closed (i.e. ‘touch in, touch out’) first-generation card-based systems provided customers with visibility on the fare paid on the card reader in real time when touching out of the system. The move to second-generation ABT systems has taken transaction processing — and the capacity to confirm the fare paid when touching out of the system — away from the reader, with processing of all contactless transactions now occurring more typically at end-of-day. However, there are examples emerging where transit agencies are developing system requirements that require real time transaction processing in an ABT environment.

It is debatable how important it is to be able to access payment history at or close to real time. Transit agencies around the world have sought to reassure customers with ‘best price’ guarantees for the full range of available fare products. In addition, trip history and associated payments can always be subsequently reviewed and queried with the transit agency if required.

At the time of the initial roll-out of contactless payment channels, there was a general expectation in some quarters that credit cards would continue to be the dominant card used for payment. However, a strong generational shift to debit has become increasingly apparent. As suggested by Visa’s chief financial officer, “Debit is clearly the gateway to cash digitization.” In Australia, the market share of debit cards increased from 15% of transactions in 2007 to 44% in 2019. In the 2021 March quarter, Visa saw 24% worldwide growth in debit volumes versus flat performance for credit, while Mastercard saw 27% growth in debit and a 1% decline in credit.

From a COFC perspective, the key issue here is the difference in merchant service fees between credit and debit card transactions. These fees are reflected in specific agreements between transit agencies and the financial institutions.

The functionality of a transit card changes from a chip with an e-purse holding funds, with the fare transaction processed at the card reader (first-generation ticketing), to a token with a primary role of providing an interface to a customer account held in the back office where the fare transaction is completed (second- or next-generation ABT environment).

Although the functionality of a transit card changes with the migration from first- to second-generation fare collection systems, there remains a strong rationale to retain a transit card. Even in those systems seeking to drive contactless payment as the primary payment channel, a significant proportion of adult customers will prefer to use a pre-paid transit card. The need for pre-paid options is even more obvious with respect to meeting the requirements of the concession market.

In terms of supporting other tokens in an ABT environment, there is a clear and strong case for supporting contactless payments (as described above) in accordance with EMV standards.1 Significantly, this means that the financial services sector is responsible for maintaining technical standards around transaction processing in a transit environment.

In contrast, should a transit agency choose to adopt other tokens supporting debit transactions in an ABT system — which could be any card or product with a chip, such as a driver’s licence, smartwatch, gym pass or university ID card — the onus falls on the transit agency to provide certification of the token against its own technical standards. This not only has cost implications for the transit agency but also could become very difficult from a customer management and communication perspective (e.g. student ID card from university X is supported as a transit token, but not the student ID card from university Y).

Although contactless payments have been introduced in many jurisdictions, this has not precluded ongoing investment in transit products. For example, Transport for NSW has been trialling an Opal digital card stored in a customer’s digital wallet.

The benefits of using a virtual card over a physical card are somewhat nuanced. Customers using their smartphone to browse the web or answer emails while completing a journey, for instance, will already have their virtual card in their hand. Similarly, some customers will enjoy the convenience of touching in and out of the system using a smartwatch rather than accessing a physical card from a wallet or purse.

From a customer perspective, it is important to avoid card clash issues with other digital or physical cards. Again, if multiple cards are stored in the digital wallet, then the transit card needs to be nominated as the default card. The same suite of issues identified above with respect to physical card clash apply.

With the proliferation of smartphones, mobile ticketing has emerged as an important customer payment channel in many jurisdictions. In 2021, an estimated eight in every 10 Australians used a smartphone. The progressive shutdown of the 3G network will further encourage the take-up of the latest generation of smartphones.

In many cases, mobile ticketing will clearly be part of the solution in terms of supporting the removal of cash on-system and supporting irregular customers without a physical contactless card. In some transit systems, mobile ticketing has been stood up as a replacement for paper tickets, with simple visual inspection; however, the migration to next-generation fare collection systems provides the opportunity to leverage barcodes and on-system optical readers for ticket validation.

As part of the transition to first-generation smart card systems and the associated withdrawal of on-system payment channels such as rail ticket booking offices, it was necessary to stand up significant retail networks with bespoke terminals supporting top-ups to the smart card e-purse. There will be an ongoing need in many systems to continue to support e-purse top-ups of transit cards and/or the purchase of other fare media where, for example, all on-system cash payment channels are removed.

Given the general imperative to maintain retail networks, it will be highly desirable for transit agencies to take the opportunity to leverage third-party devices as opposed to maintaining a network of bespoke transit-specific terminals. The need to provide bespoke retail devices inevitably saw transit agencies seek to limit the scale of the retail network to minimise both capital and operating costs. Solutions have emerged to address this issue. For example, an app is being developed as part of the Queensland ‘Smart Ticketing Project’ that can be downloaded to third-party terminals. Accordingly, there is no longer a need to artificially cap the number of retail outlets supporting transit payments as was the case with the first-generation solution.

It has now become commonplace in many retail settings for businesses to highlight and pass on the costs of using different payment channels. To date, transit agencies have generally tended to absorb these costs, hence creating a material differential between the market-facing (gross) fare and the net revenue received by the transit agency. In Australia, the Reserve Bank of Australia standard allows businesses to charge their customers a cost-based surcharge on card payments, but any surcharge is limited to the amount it costs the business to accept that type of card for that transaction.

It is interesting to note that, in some cases, transport authorities do apply and pass on cost-based surcharges (e.g. payment of motor vehicle registration). With the increasing significance of contactless payments and the convenience benefits afforded to customers, there could be a case for passing on these costs in the future. There is an interesting analogy here with toll road use, specifically the availability of a free alternative road offering lower amenity. In the transit payments space, this alternative could be the agency pre-paid transit card. The merits of this approach clearly depend on the relative cost to serve each channel.

Recent customer research conducted in New Zealand provided a range of valuable insights, particularly with respect to the transition from a first-generation card-based system to a second-generation system supporting contactless payments.

By way of context, it is worth noting that New Zealanders exhibit a strong preference for digital banking and contactless payments. Cash is the main/preferred method of payment for less than 10% of surveyed New Zealanders.

Only 6% of customers indicated a preference for continuing to use single-trip paper tickets. If the option to purchase a single-trip paper ticket were withdrawn, 76% of these customers indicated they would use a pre-paid transit card or a contactless debit/credit card. The remaining 24% indicated that they would stop using public transport altogether. In the New Zealand context, this 24% represents 3% of regular public transport customers.

The New Zealand research also highlighted the continued strong preference for using a pre-paid transit card. Nearly five in 10 customers (48%) expressed a preference for this payment channel, with around four in 10 customers (41%) expressing a preference for contactless debit/credit card payment.

The research also specifically provided some key insights into the capacity to drive take-up of contactless payments:

-

Just over one-third of customers are ‘ready to go’ (i.e. are familiar with and prefer contactless payment)

-

Another third will need some reassurance (i.e. are familiar with and prefer contactless payments but require reassurance around security/privacy and capacity to assess trip history)

-

Around 10% are ambivalent (i.e. do not have a contactless debit/credit card or smartphone but are open to using this payment channel)

-

The remaining 15% are characterised by a range of barriers to using contactless payments in public transport and will be difficult to engage (e.g. have security concerns/fears, perceive that credit cards are not for ‘everyday’ transactions, dislike using credit and lack familiarity/comfort with contactless payment generally)

The procurement of second-generation (account-based) transit fare collection systems creates an imperative to carefully review customer channel strategy. Specific channel issues that need to be addressed include:

- The potential to go ‘cashless’

- The merits of pursuing the aggressive take-up of contactless payments

- The retention and positioning of the transit card (including the need for, and role of, a virtual transit card)

- The case for supporting non-transit tokens for debit payment (other than EMV-supported debit transactions)

- The role of mobile ticketing

At a broader strategic level, there are additional considerations such as:

-

Providing customers with transparency regarding merchant services fees and potentially passing these charges on to customers directly (i.e. over and above the fare paid)

-

Specifying the real-time processing of transactions to overcome one of the perceived losses of customer amenity associated with the migration to ABT processing (i.e. the inability to display the fare value when payment is made)

-

The breadth of channels offered and the positioning of each to support the realisation of transit agency objectives with respect to the overall COFC

Related insights

You might also be interested in these insights.

English