Natural capital — the stock of natural resources that yield a flow of benefits to humans, companies and economies — is under pressure. Globally, we use volumes of renewable natural capital resources such as timber and fish equivalent to those provided by approximately 1.8 Earths every year.1 Additionally, we are reaching or have reached the maximum production rate in terms of additional units mined for certain non-renewable natural capital resources, such as gold, silver and copper. This overexploitation, alongside other factors such as climate change and pollution, has driven us into a state of natural capital deficit.

Why does this deficit matter? It is easy to see what may be at stake when natural capital diminishes: natural capital is a source of inspiration, relaxation, spirituality, education and aesthetic pleasure. Beyond these social benefits, natural capital is a crucial economic resource, and its decline will have far-reaching consequences for businesses and economies.

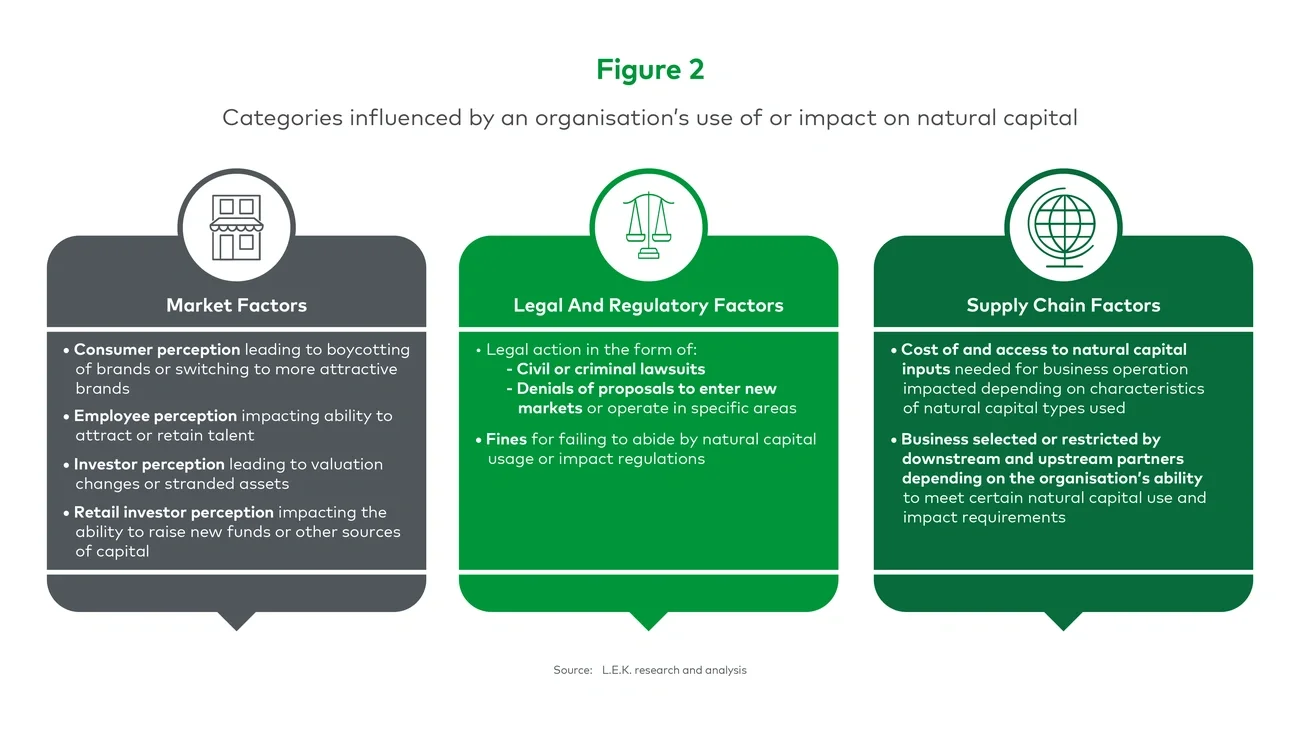

But natural capital risk is also inherently a business risk. According to the World Economic Forum, around half of the world’s gross domestic product is highly to moderately dependent on nature either directly or indirectly. Given supply chain dependencies on natural capital, the World Bank estimates that organisations will face significant operational risks, such as increased costs or the inability to access inputs of production, as a result of a diminishing natural resource base.

Beyond operational risk, organisations can also be susceptible to reputational and regulatory risks, from both their use of and their impact on natural capital. On the flip side, organisations may find opportunities through successfully mitigating their natural capital use and impact. Focusing on these risks and opportunities will become increasingly important to ensure a long-term competitive advantage. As scrutiny from scientific, public and regulatory stakeholders grows, expectations about the responsibility organisations have towards natural capital are also set to increase.

In this edition of Executive Insights from L.E.K. Consulting’s Sustainability Centre of Excellence, we highlight the risks that organisations face as a result of the decreasing quantity and quality of natural capital, as well as the opportunities that come from mitigating their natural capital use and impact. We also lay out key questions that organisations can consider to assess their exposure and to develop a natural capital strategy.

What is natural capital?

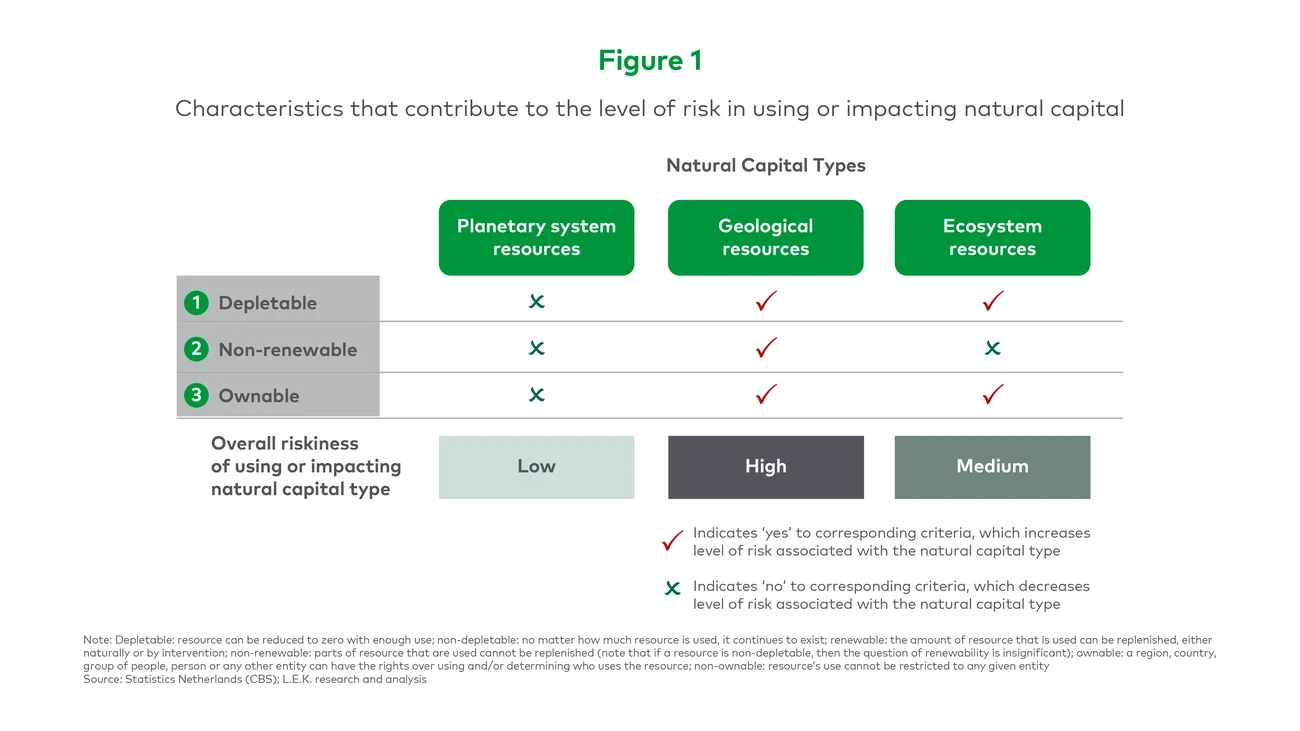

Figure 1 (below) depicts the three main types of natural capital: planetary system resources (e.g. sunlight, water, wind, air and fire), geological resources (e.g. minerals, metals and fossil fuels) and ecosystem resources (e.g. forests, coral reefs, coasts, lakes, open ocean and grasslands). Economic value can be derived from each resource group through means such as solar, wind and hydropower; oil; natural gas; batteries; plastics; wood; paper; food (e.g. plants or animal byproducts); natural medicines; pollination; and tourism, among other examples.

All organisations use or rely on these different types of natural capital as inputs to production, even though this may differ depending on their unique requirements and position along the value chain. Organisations may also impact natural capital as a byproduct of production or of other organisation activities (e.g. via disposal of waste). Furthermore, use and impact are almost always connected.

An organisation’s use of and impact on natural capital have inherent risks, such as negative public perceptions, lawsuits and disruptions to supply chains due to dependence. The extent of risk an organisation may face is in part determined by three key characteristics of the natural capital — whether it is (1) depletable, (2) non-renewable and (3) ownable.