In the past three years, the second charge lending market has grown substantially. Yet as consumer indebtedness begins to exceed pre-crisis levels, many investors, funders and market participants are beginning to question whether the second charge market’s recent success is merely a bubble rather than a genuine indication of prolonged sustainable growth.

L.E.K. Consulting believes that the second charge lending market now shows fundamentally different characteristics compared to the pre-financial crisis period, as a result of regulatory reform, changes to underwriting practices and product innovation, supported by renewed demand from a positive macroeconomic environment. This Executive Insights examines what the future may hold for second charge lending, reviewing the drivers of recent growth and highlighting the principal considerations for operators and investors.

The second charge market is growing

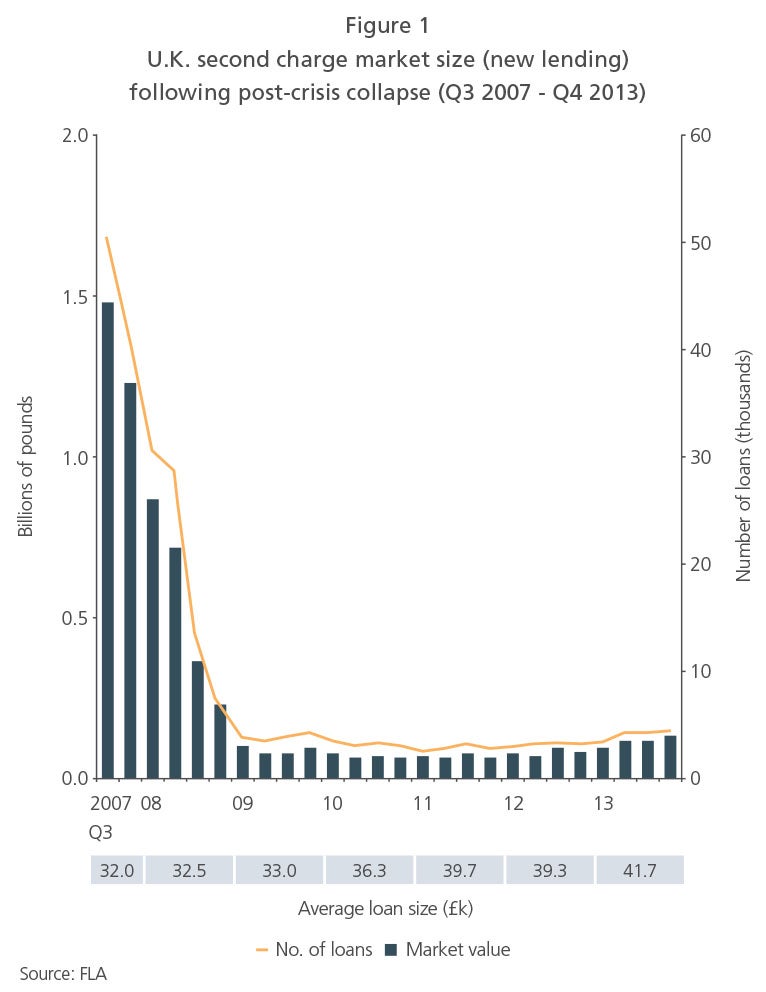

Historically, the second charge market was something of a reserve option, serving the borrowing needs of a predominantly sub-prime audience seeking debt consolidation and large loans for home improvement or one-off purposes. When the credit crunch hit, the market collapsed as it struggled to survive in the new economic climate, due to a combination of poor underwriting and realised losses. Between its peak in Q3 2007 and Q1 2009, the market contracted by c. 90% (see Figure 1), and a number of lenders, such as Welcome and Northern Rock, were forced to exit, leaving second charge with a sometimes still-lingering reputation as a risky sub-prime product.

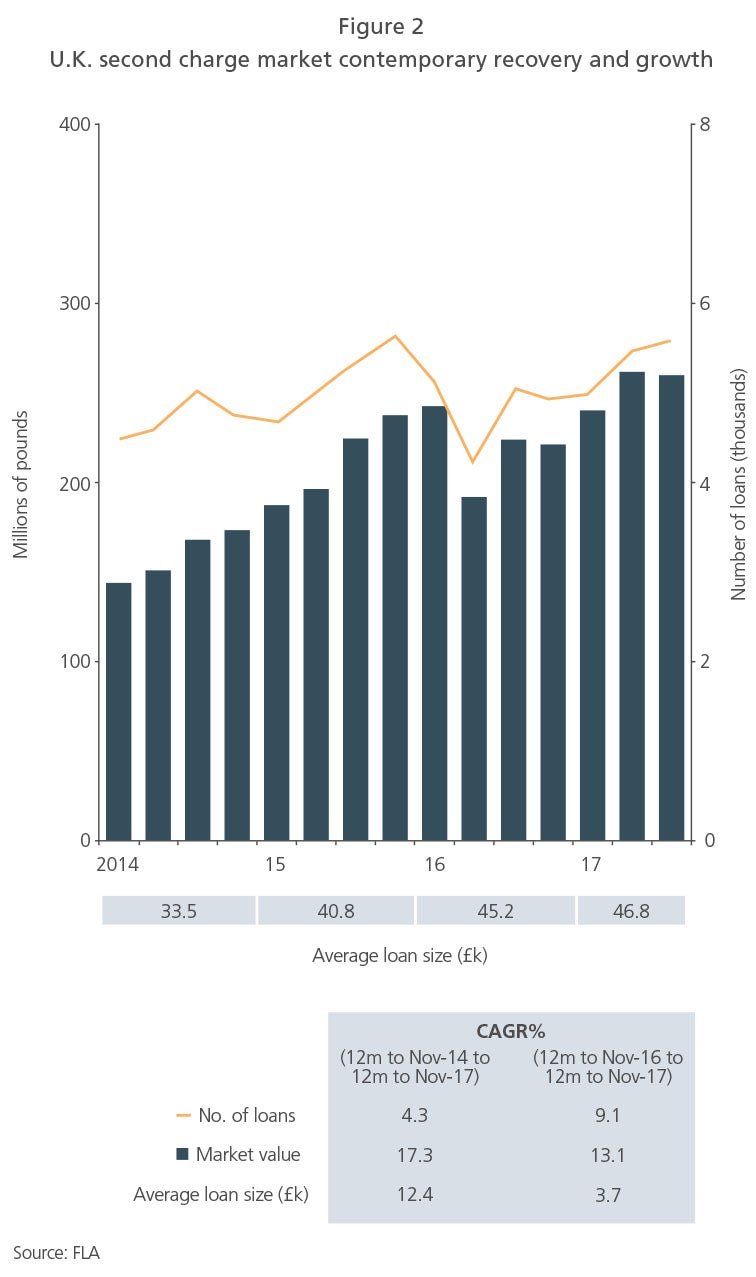

However, in recent years the second charge market has shown signs of recovery. Regulatory reforms, product refinement and innovation, and tighter underwriting have resulted in lower write-off rates and a far more stable market. This in turn has made it increasingly attractive to challenger banks and private equity firms (among others). The market was worth c. £1.1bn in gross new lending in the year to November 2017, growing at c. 17% p.a. between Q1 2014 and Q3 2017 (see Figure 2).

Five principal demand- and supply-side trends are behind this expansion:

1. Increased broker awareness due to regulatory reform

In recent years, consumer awareness of second charge mortgages has been low, resulting in the majority of second charge lending distribution being heavily reliant on referrals from intermediaries. Following the introduction of the Mortgage Credit Directive (MCD) in March 2016 (which stipulates that advisors must disclose limitations in the range of products they can offer as well as the availability of other options), awareness of second charge mortgages amongst first charge brokers and financial advisors has increased. This has led to a rise in referrals from first charge brokers, a trend we expect to endure as awareness of second charge products continues to grow.

2. Decrease in second charge interest rates

Previously, interest rates for second charge mortgages were relatively high, making them less attractive compared to alternatives, such as re-mortgaging. The decrease in second charge rates from typically >10% in 2015 to c. 6% in 2017 has increased the attractiveness of second charge, making large loans for a range of purposes more affordable and accessible to a wider audience. Rates in the market have decreased to such an extent that they are beginning to converge with first charge rates (particularly as competition increases). This means that many consumers are choosing to top up with a second charge rather than re-mortgage the entire sum at a potentially higher rate, and many more would logically do the same if they were aware of this option.

3. Product innovation

There is now a wider product range compared to the immediate post-crisis market, with the product set expanding to include longer loan terms (in some cases up to 35 years), higher maximum values and more products at a high loan-to-value (LTV) ratio (85%+). Lower prices are also broadening the potential uses of the product, including into prime and wealthier customer groups that would historically have been put off by high prices; for example, the idea of using second charge as a means of inter-generational wealth transfer is now viable and, in the right circumstances, potentially more attractive compared to other available options. These changes have resulted in a wider range of customer needs being met and therefore an expansion of the range of addressable consumers.

4. Housing market dynamics

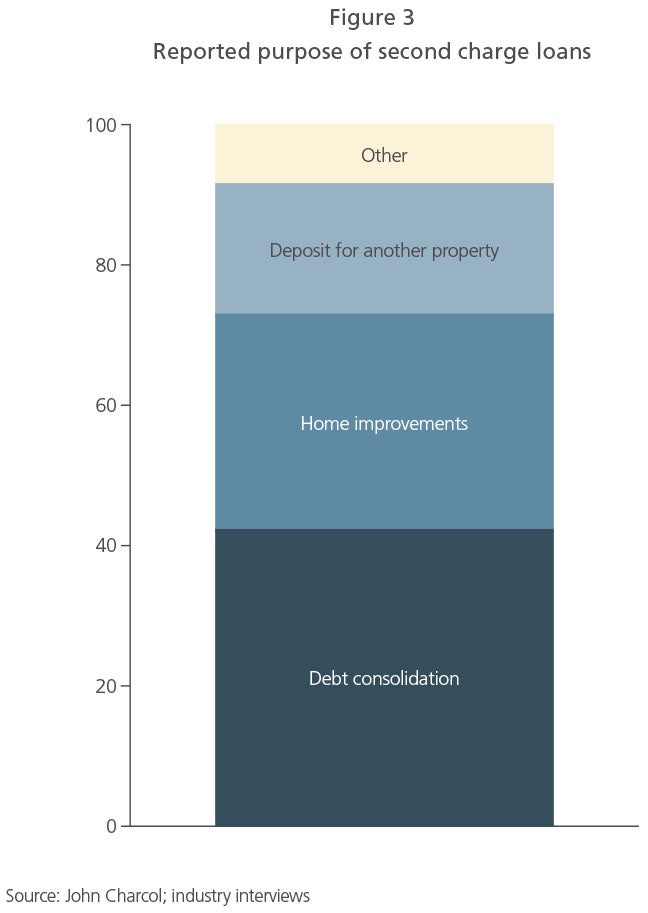

House prices have increased by c. 6% p.a. 2014-2017. This growth has reduced outstanding LTVs, leading to an increase in the capital available for release through second charge mortgages, and more consumers are choosing the option of second charge as a way to release equity from property assets. Furthermore, as house prices increase, so do demands for home improvement (see Figure 3), as rising consumer uncertainty sees homeowners choosing to stay put rather than move. Although there are regional disparities, these increases in prices are expected to continue.

5. Increased indebtedness

Growth in unsecured credit has resulted in greater demand for debt consolidation (see Figure 3). Unsecured consumer credit grew at c. 7% p.a. 2014-2017, with mortgagors accounting for c. 40% of unsecured consumer credit. As consumer debt increases, so does the demand for debt consolidation and therefore second charge mortgages.

All five of these drivers can be expected to support continued growth in the second charge market over the medium term.

Recent growth is not a repeat of the pre-crisis boom

It is evident that the second charge market is thriving, and some questions are being raised about similarities to the pre-credit crunch market. In L.E.K.’s view, rather than cyclical boom-and-bust, second charge has experienced a transformation and the emerging product has been redefined, leading to continued sustainable growth over the medium term.

Changes in regulation mean that second charge products are written fundamentally differently to how they were pre-crisis. Many previously allowable lending criteria are no longer possible, and with the introduction of more stringent checks, as well as the removal of very high LTV products (over 100%), access is restricted and loan sizes contained for some borrowers. As a result, the market is much smaller than it used to be — approximately £1.1bn of gross new lending in the year to November 2017 vs. c. £6bn p.a. at its pre-crisis peak — and it is unlikely that second charge lending will ever return to the size that it used to be without considerable expansion beyond the customer base and set of customer needs currently being addressed.

In addition, while there is demand for the product, consumer awareness remains low; only c. 15% of customers considering a mortgage profess to understand what a second charge mortgage is. The product continues to be heavily reliant on referrals and while the number of referrals from first charge brokers has increased following the MCD, spreading awareness and educating brokers takes time. At present, only c. 10% of first charge brokers refer customers to second charge master brokers, and very few package second charge themselves, due to the inherent complexity of the product. This, in the short term at least, will act as a brake on market growth.

Key investment considerations

It is unlikely that second charge lending will ever reach its pre-crisis size, but the market is expected to show continued growth over the next five years. This growth will include both the “traditional” uses of second charge, such as home improvement and debt consolidation, and newer uses, such as the genuine substitution of prime re-mortgages and the release of equity from property assets for inter-generational wealth transfer.

With a newly rejuvenated market comes plenty of opportunities for lenders, funders and equity investors alike, but a “shoot from the hip” approach is unlikely to yield positive results. There are several factors that will be key to sustainable differentiation and success in this market:

- Access to a loyal and satisfied broker base to help the flow of second charge referrals, and potentially a direct-to-consumer approach to augment this

- The ability to make well-informed commercial decisions through the proprietary use of technology and analytics, including increasing sophistication in underwriting to optimise conversion rates and yields

- The ability to compete with established bank lenders through carefully constructed funding structures

The second charge lending market is significantly more stable than it was previously, and the opportunities are substantial. Winning strategies in this rejuvenated landscape will be founded on a sound understanding of the market and consumer behaviour, and access to sector-leading analytical and operational capabilities.

09182018090920