After seeing a rapid increase in deal activity over the past three years, the energy sector in 2023 offers tremendous opportunity for even more.

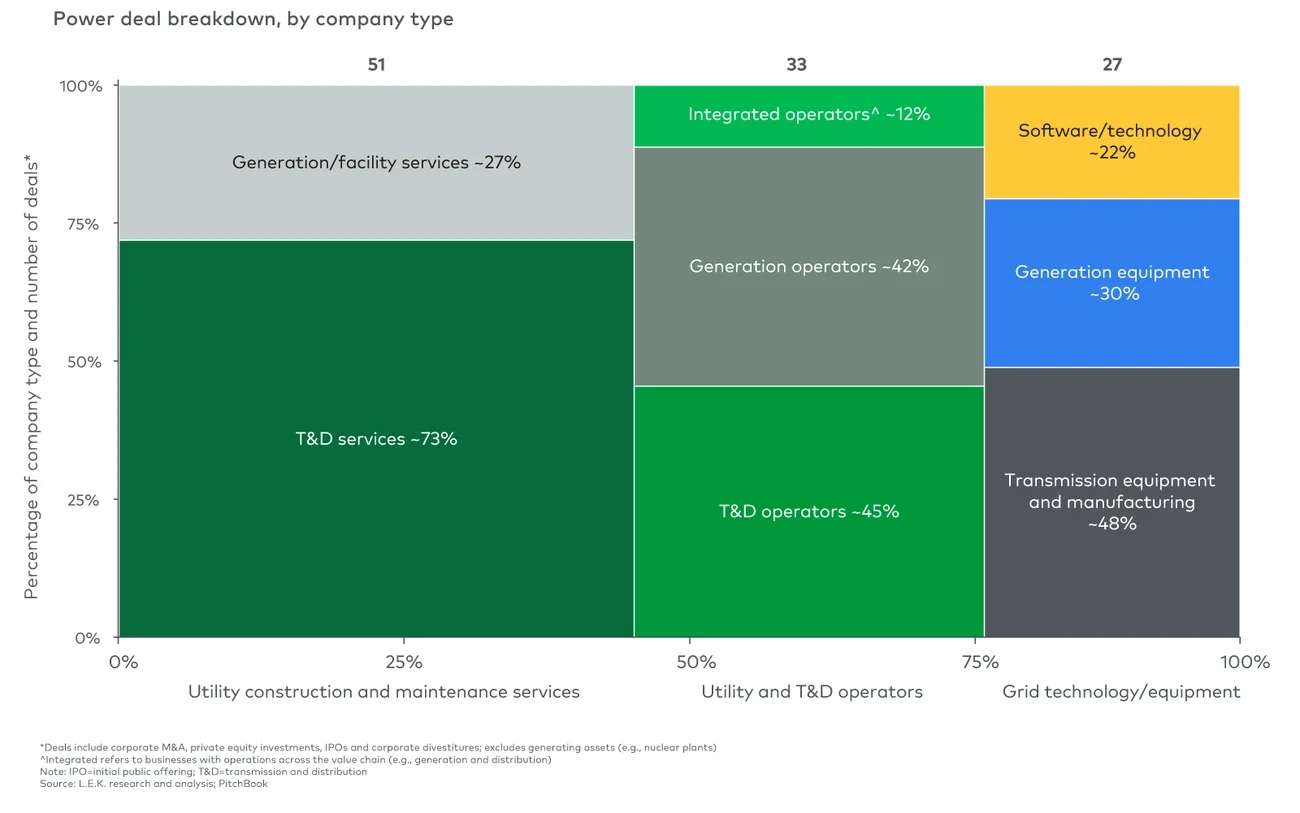

Starting in 2020, at a high level, energy security, decarbonization and value-based growth dynamics began powering the energy deals space. And from corporate M&A to private equity investments to initial public offerings, deal activity remained resilient through 2022, even in the face of macro uncertainty and the higher cost of debt. Notably, the number of power-focused deals in 2022 rose over 2021, while those in oil and gas (O&G) and renewables were flat.

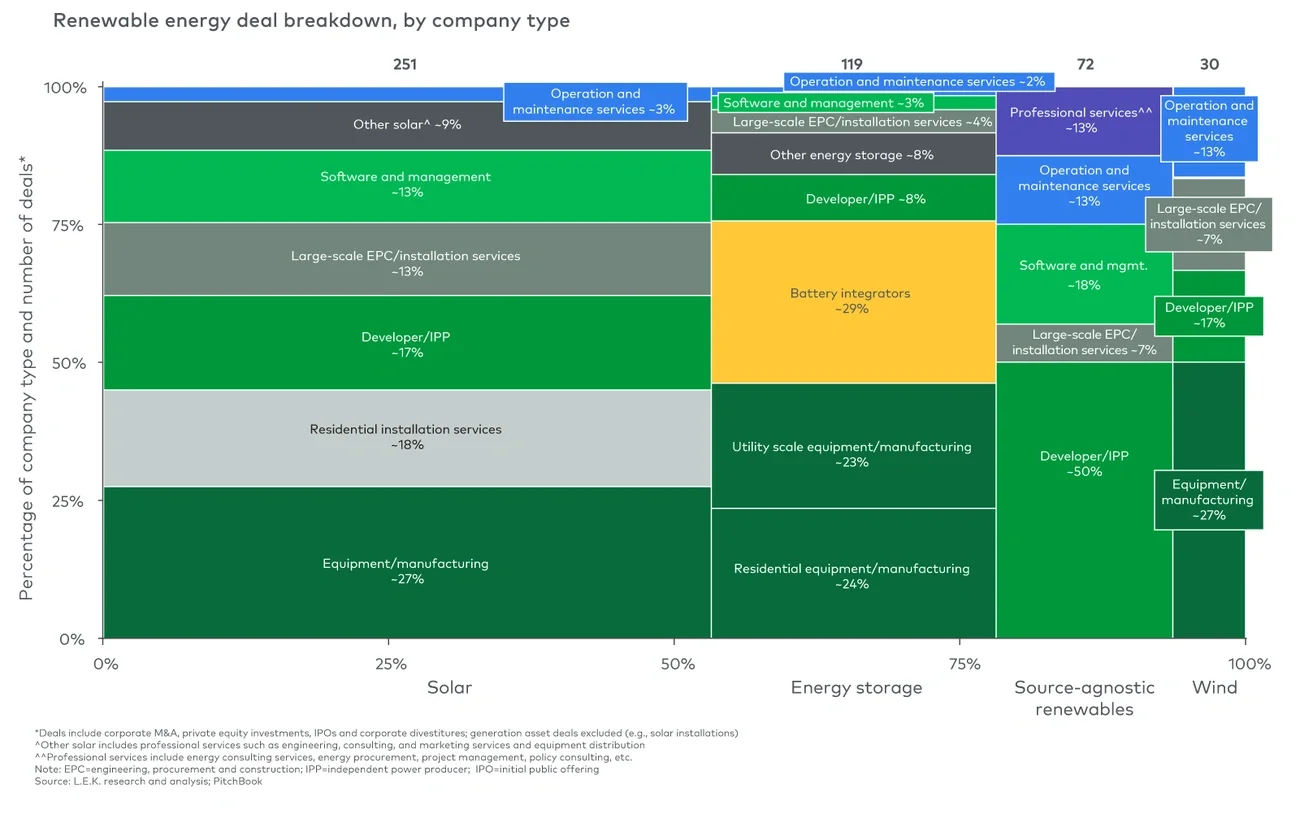

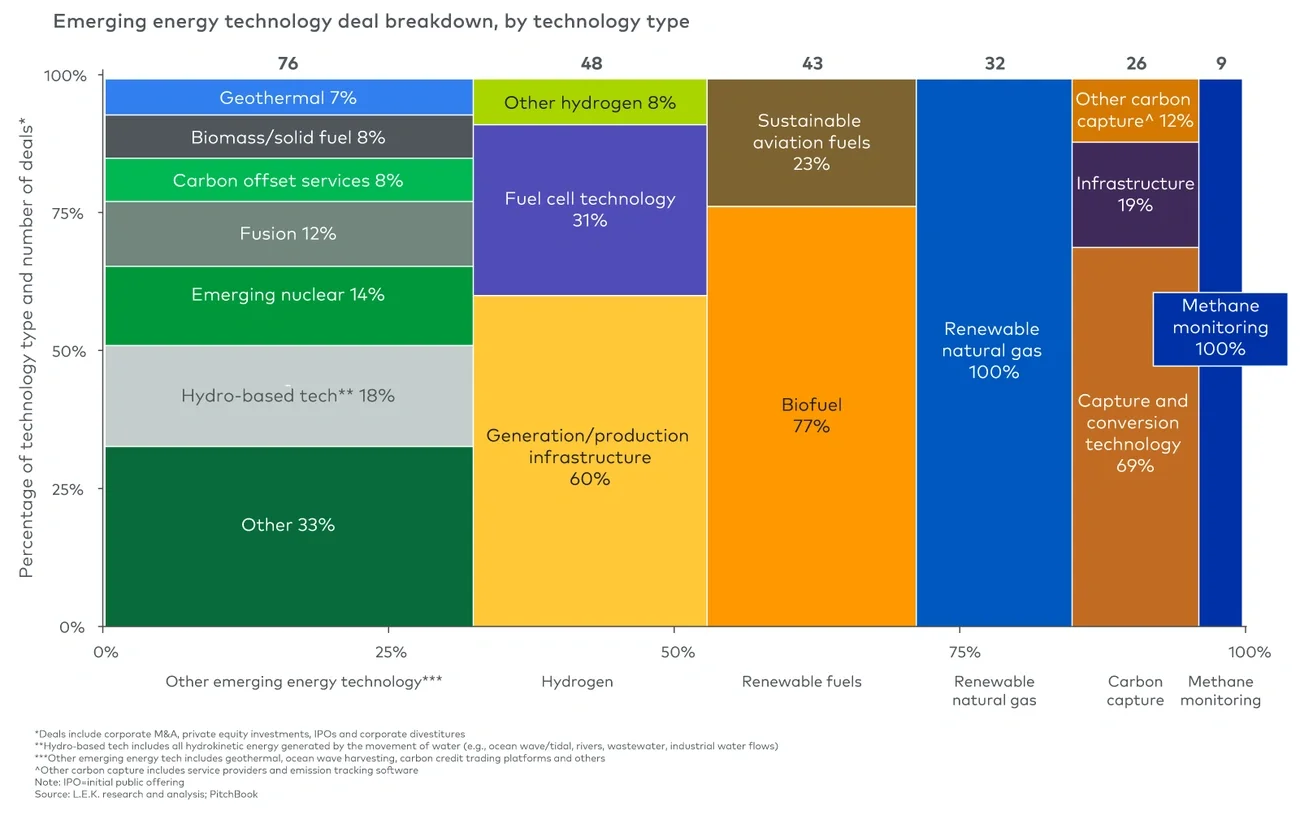

But now, in 2023, all three of those subsectors along with two others — emerging energy technology and energy management and mobility — are poised to see significant deal activity. And as with 2020-22, each sector’s deal activity will be driven by a unique set of circumstances.

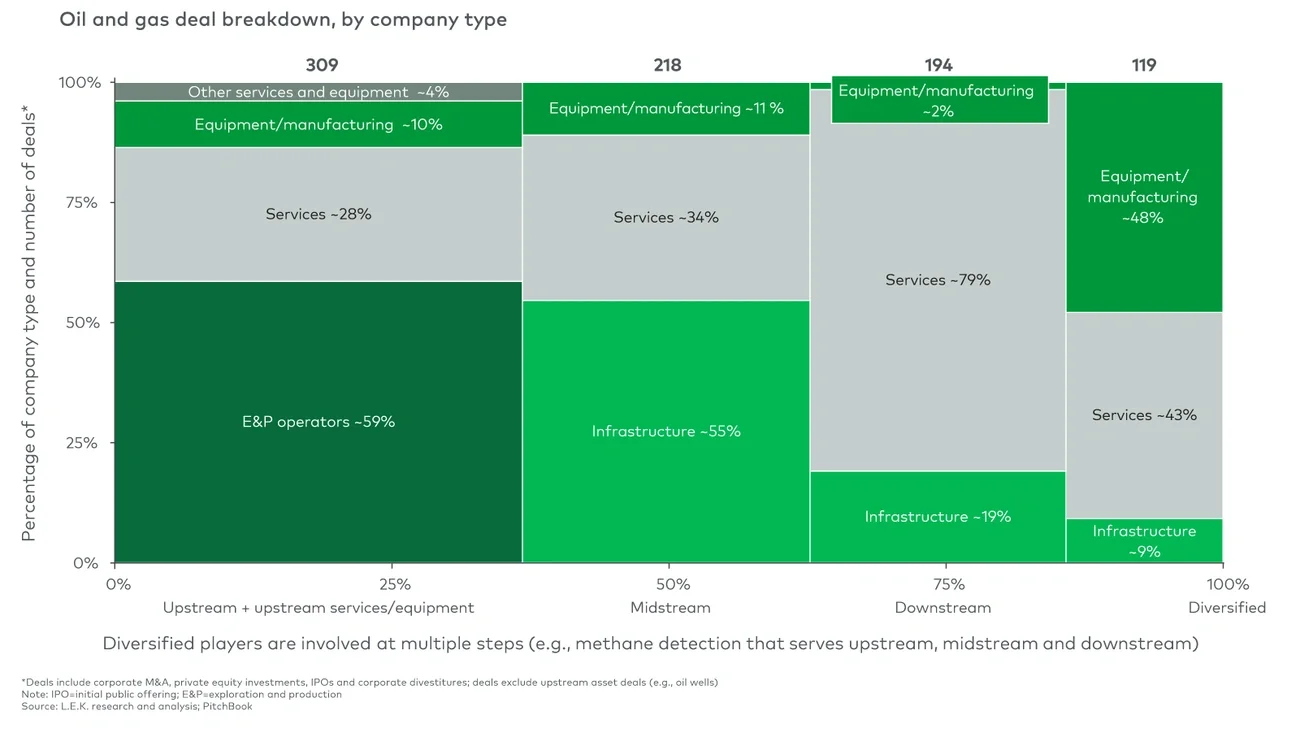

Oil and gas

In O&G, deals over the past three years were driven by corporate-level activity aimed at consolidation that would allow individual segments to remain competitive via cost savings so they could stave off market headwinds. Energy security needs in light of Russia’s invasion of Ukraine was another significant factor (see Figure 1).