Distributors can extend their value offerings to customers in the form of incremental contractor support, product training and purchasing recommendations. As customers become more reliant on the expertise of their distributors, the relationship between the two becomes stronger, increasing margin levels.

Environmental pressures

Industrial firms are feeling pressure from heightened regulatory and public scrutiny around climate and environmental issues, forcing them to reevaluate their approaches to emissions and climate impacts.

One result of that reevaluation is a stronger focus on Scope 3 emissions — increasing attention on emissions up and down the value chain that a company is indirectly responsible for. Using this concept, distributors have an opportunity to differentiate themselves as partners by aiding customers in reaching emissions- and climate-related goals. Some ways to do this include minimizing packaging, reducing man-hours and energy consumption, and optimizing shipping and last-mile delivery routes.

Determining strategic responses to market challenges

To address these myriad challenges, distributors should reflect on a number of questions to develop strategic responses to oncoming industry changes. These include:

-

Value-added strategy: Are we adding sufficient value to avoid disintermediation by and competition from low-cost players?

-

Commercial excellence: How do we improve the performance of commercial functions from the go-to-market model through sales force effectiveness?

-

Operational excellence: How do we ensure our organization has the appropriate structure, capabilities and resources?

-

Opportunities for growth: Where can we find opportunities in adjacencies or other parts of the value chain?

-

Digital strategy: Which digital capabilities will be required to be relevant and successful in the future?

The answers to these will vary based on individual and market circumstances, though L.E.K. Consulting’s experience across multiple assignments in this space allows us to determine some common themes. We expect significant interplay between these trends, with all of them contributing to the evolving and growing industrial distribution space.

Through insights gathered while working with clients in the industrial distribution industry, L.E.K. has compiled the following examples of potential responses to key market trends that may be considered by strategic companies:

Proliferation of digital solutions

- Identify high-impact areas of opportunity for investment in process optimization technologies

- Align with manufacturers’ omnichannel distribution strategies and ensure differentiation in light of proliferation

Supply chain constraints

- Build up redundancy of supply to enable distributor nimbleness in the dynamic supply chain environment

- Enhance information sharing across full value chains, increasing efficiency and avoiding disruptions

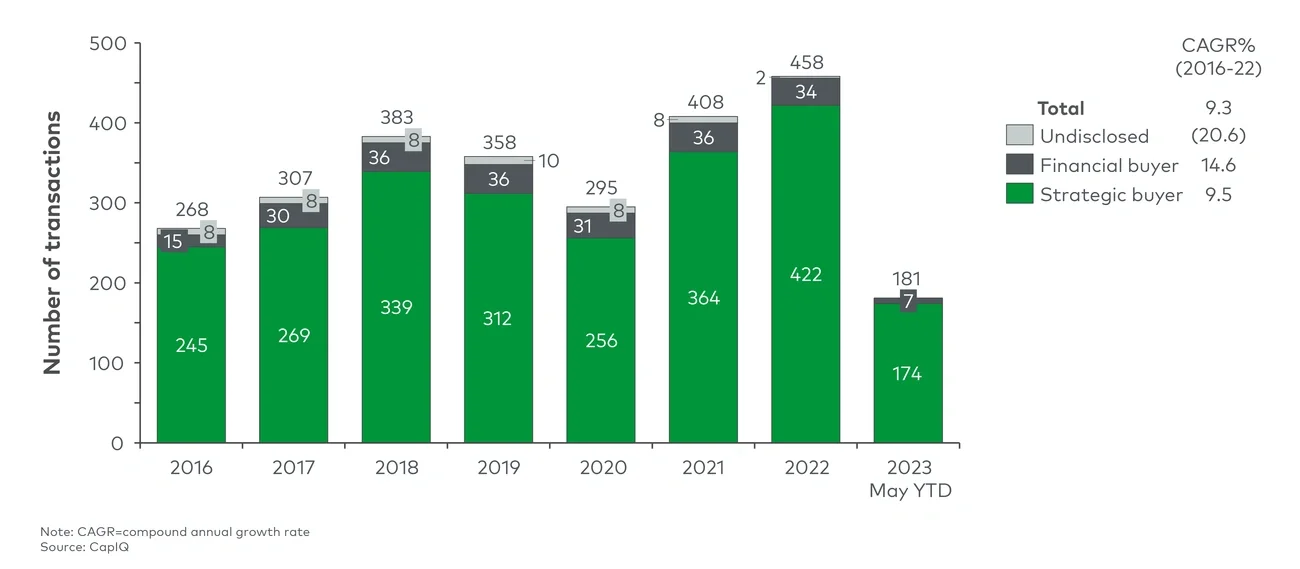

Industry consolidation

- Pursue either a broadline or a specialist approach to distribution to avoid being stuck in the middle

- Seek companies with which to partner or companies to acquire to build out respective offerings and expertise

Growth of value-added services

- Optimize service offerings to increase customer and partner touchpoints by providing value-added services

- Invest in technologies that enable a wider range of value-added service offerings to partners and customers

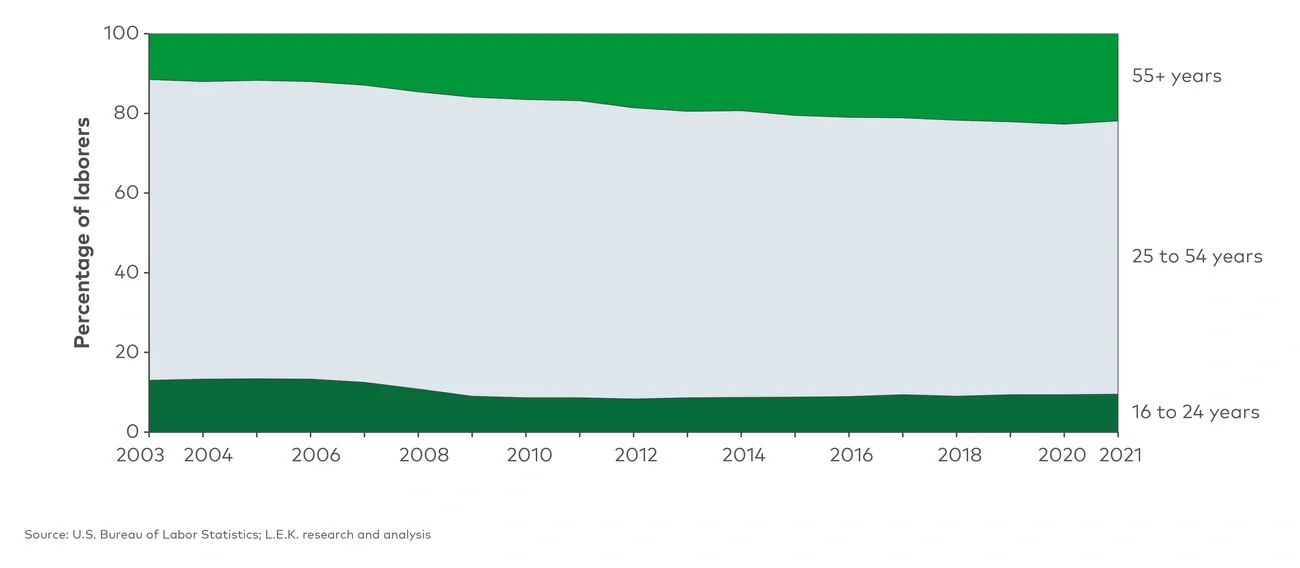

Aging of the workforce

- Enhance the value proposition to employees and those of distributor customers by increasing range and depth of talent and training resources

- Invest in automation technologies that reduce labor requirements and provide long-term cost advantages

Environmental pressures

- Collaborate with key customers and manufacturers to understand environment-related goals and targets

- Align strategies to clearly define how distributors can provide leverage for partners reducing Scope 3 emissions

For more information, please contact industrials@lek.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting LLC

Endnotes

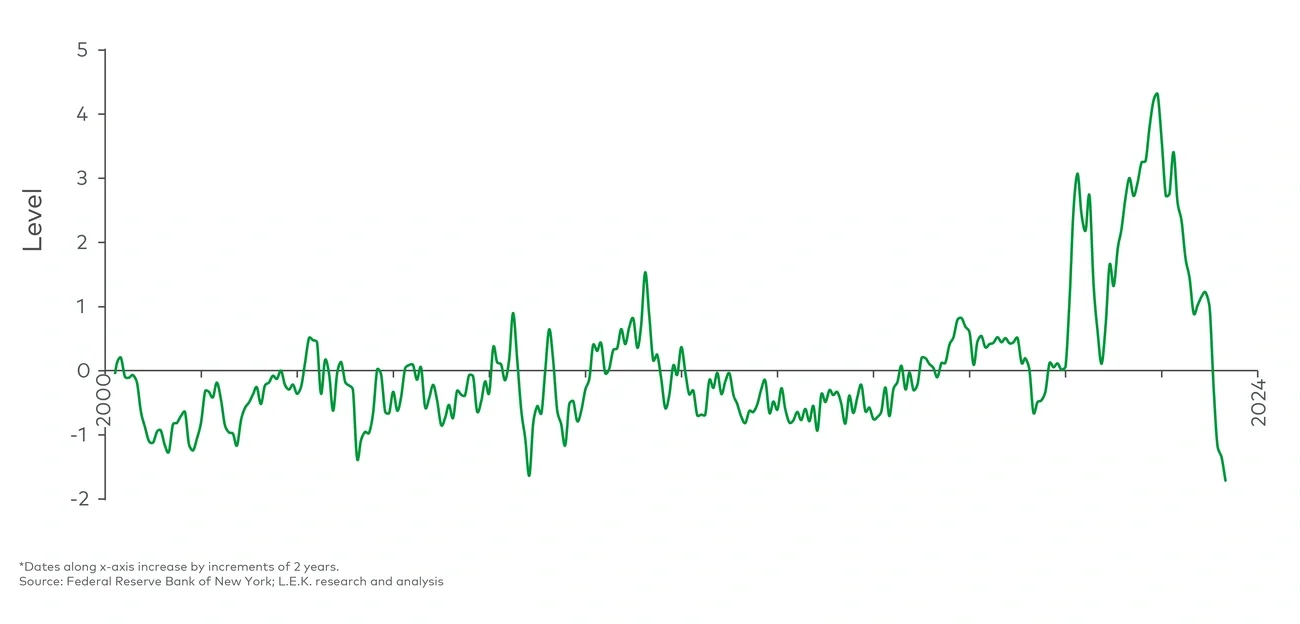

1The index considers transportation costs using data on ocean shipping costs and supply chain-related components from the Purchasing Managers’ Index surveys for China, the Euro area, Japan, South Korea, Taiwan, the UK and the U.S. Each index is scaled by its standard deviation — a zero indicates that the index is at its average value, positive values represent how many standard deviations the index is above this average value and negative values represent the opposite.

Editor's note: this article appeared in Industrial Distribution.