Hurricane Ian, which hit Southwest Florida in September 2022, caused a devastating loss of life and the dislocation of hundreds of thousands of Floridians. It was the fifth strongest hurricane to make landfall in the mainland U.S., heavily impacting population-dense counties such as Lee, Collier, Charlotte and Sarasota. With Category 4 winds and a destructive 10-to-15-foot storm surge reaching far inland, damage to homes and communities came not only from wind and rain but also flooding. On average, Hurricane Ian is estimated to have caused $50 billion-$75 billion worth of insured damages and may ultimately be the costliest storm in state history.

With communities still mourning casualties and facing mass dislocation as a result of the storm, the responsibility to prioritize rebuilding falls on companies and individuals who will drive reconstruction of homes, businesses and infrastructure to clear a path toward recovery.

Assessing the situation

Generally, reconstruction costs can be much higher than the headline insured estimated figures for a storm like Ian, due to uninsured damages, reconstruction premiums and other factors.1 L.E.K. Consulting calculates that the $50 billion-$75 billion in estimated damage may total roughly $50 billion-$80 billion in reconstruction value over the next five years, and up to $60 billion-$110 billion in total rebuild value.2

In total, L.E.K. estimates that Hurricane Ian could add growth to existing construction demand, with variation depending on rebuild scenarios and the products and services involved. On top of that, Florida construction companies will also be addressing the incremental construction demand unrelated to Ian.

Forecasting the type of construction

The first construction efforts prioritized after a storm like Ian tend to be infrastructure-based, repairing or rebuilding railways, roadways, causeways and other structures that enable the transportation of people and supplies. We expect to see the same prioritization in this case.

Here, the majority of new construction activity is expected to be concentrated on coastal locations, which have seen the most damage due to the combination of high-strength winds and extreme storm surge. Not only did Ian cause immense structural damage — more than 5,000 homes and almost 300 businesses in Lee County alone were completely destroyed, requiring a total rebuild — but satellite images show it also may have even changed Florida’s coastline. An additional consideration regarding coastal reconstruction is that many homeowners will choose premium construction, as did homeowners after Hurricane Michael in Mexico Beach, Florida, which saw the average home price rise from $271,000 in 2019 to $453,000 in 2021, although some of this increase in price is due to the general increase in house prices. At the same time, some new construction demand in the most extreme-weather-prone areas may be tempered by a higher rise in insurance costs.

Though inland locations like Cape Coral sustained less damage from Hurricane Ian than coastal locations such as Fort Myers Beach, they were hard hit by flooding from the storm surge and rainfall. After experiencing multiple feet of standing water for nearly a week after the storm, these locations are expected to see a large amount of construction needs to repair or rebuild existing structures. The widespread lack of flood insurance held by inland property owners may tip construction needs away from rebuilds and towards “remove and replace”.

Calculating construction timing

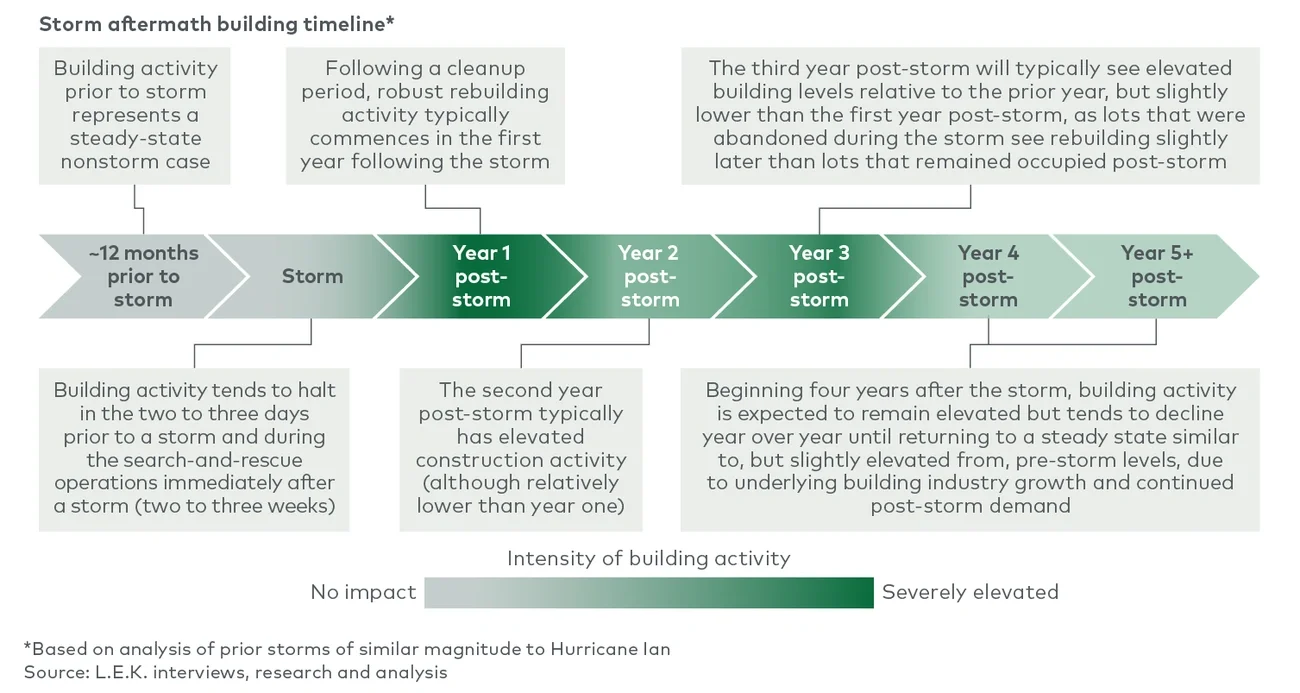

The experiences from prior storms can inform recovery timelines for Hurricane Ian (see Figure 1).

- Initial demand and six-month surge: There are certain needs that occur immediately after a hurricane, such as debris cleanup, search and rescue, and restoration of utilities. After these priorities are addressed, the state will see a high-demand period of construction activity at about the six-month mark — in this case, March 2023.

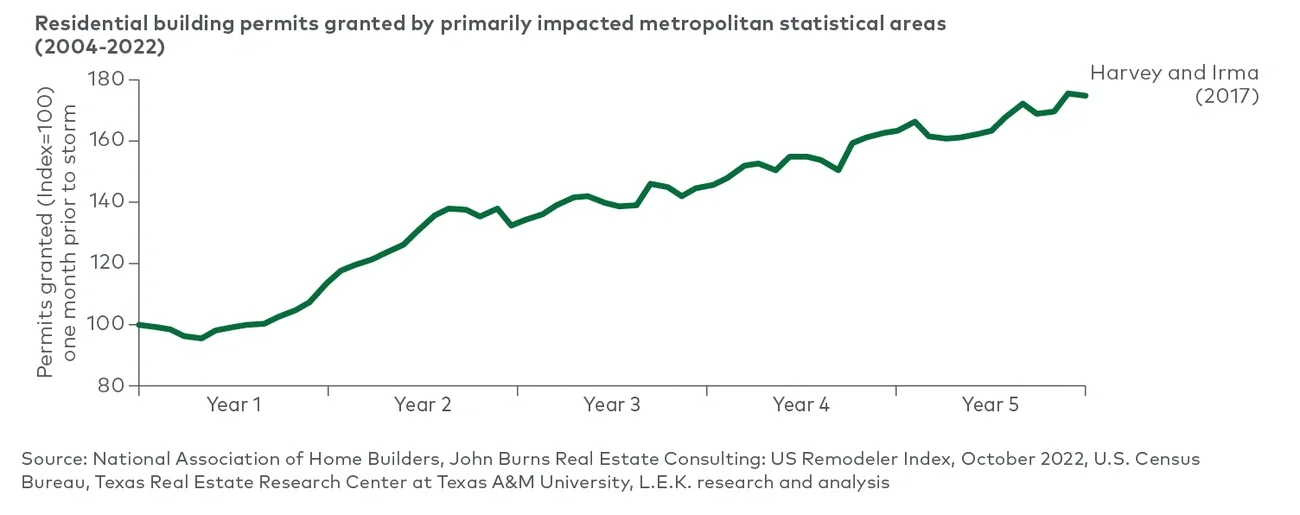

- First-year high: Construction demand can be expected to be at its highest level in the first year after a storm, after the four-to-six-month cleanup period. After the similar hurricanes Harvey and Irma, residential building permits saw a jump in the short term “catch-up” period before growing significantly (see Figure 2). Permits for Hurricane Ian are already being expedited to speed up recovery.