The medtech industry’s operating environment has encountered unprecedented volatility and disruption over the past several years, and executives throughout the industry are being forced to address a host of new, pervasive challenges and accompanying trade-offs that companies inevitably face.

In the following Q&A, L.E.K. Consulting partners address the eight most common questions medtech executives have raised recently, ones that are top of mind as we move toward the end of 2022 and into 2023.

This Q&A was previously published in MedTech Strategist on Sept. 13, 2022.

Q1: We are hearing more and more about supply chain issues being a problem for medical device companies. Are you hearing the same thing in your practice? And what form are those problems taking? Can you offer some examples of how the problems are manifesting themselves?

L.E.K. perspectives:

-

Supply chain issues are materially impacting not just the medical device sector, but also healthcare more broadly. Shortages first appeared during the early stages of COVID-19 and the “reopening” period, and personal protective equipment (PPE) became a severe scarcity segment. As the period of irregular supply – and demand – has extended, supply chain challenges have continued to expand and add up, and their breadth as well as intensity now may even overshadow those of the PPE shortage earlier.

-

Today, PPE constraints have eased and most challenges across medtech stem from component and materials insufficiencies, staffing shortage uncertainty, freight/logistics challenges such as port congestion and transportation inconsistencies, persisting lockdowns in China, the global energy crisis, and impact from the Russia-Ukraine conflict.

-

These disruptions extend along the supply chain across multiple junctures, e.g., contract manufacturers serving original equipment manufacturers (OEMs), and OEMs serving hospitals/providers.

-

Demand volatility over the past 2.5 years, with shutdowns impacting elective procedures during major variant waves, followed by pent-up demand affecting the system after these waves, has created bottlenecks that are likely to continue well into 2023 and add to the above challenges.

-

-

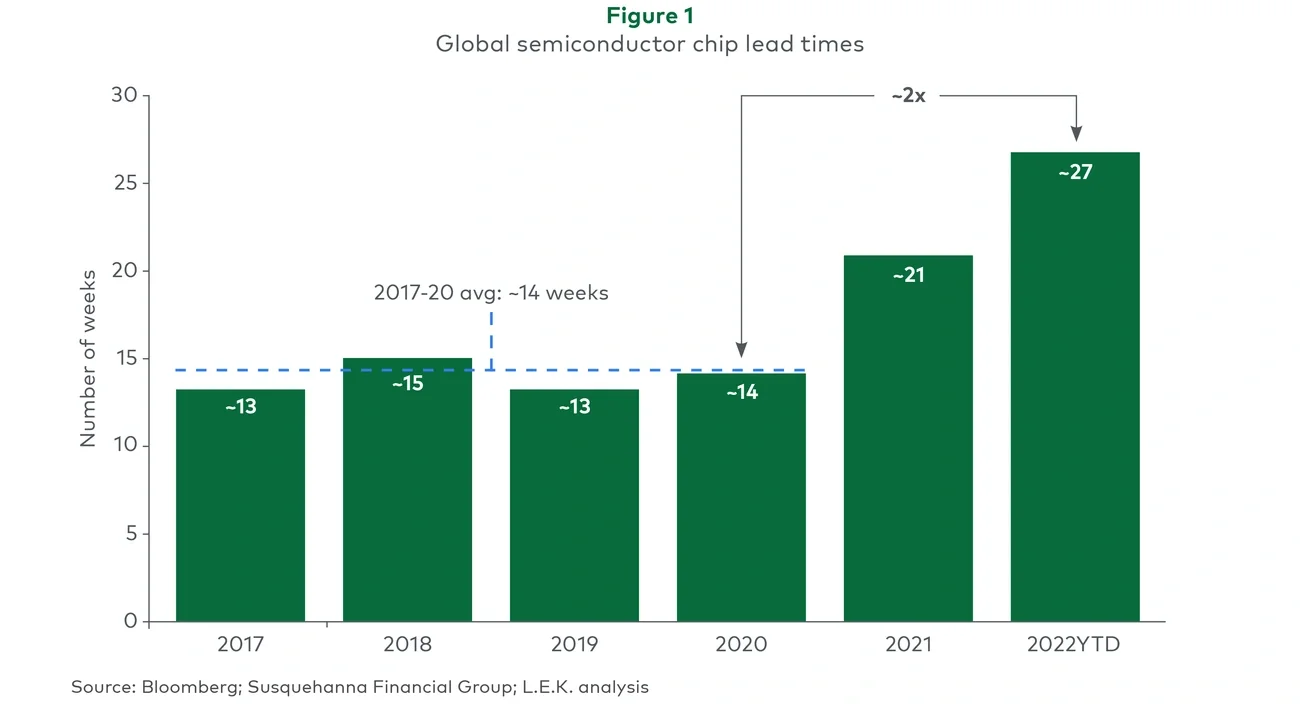

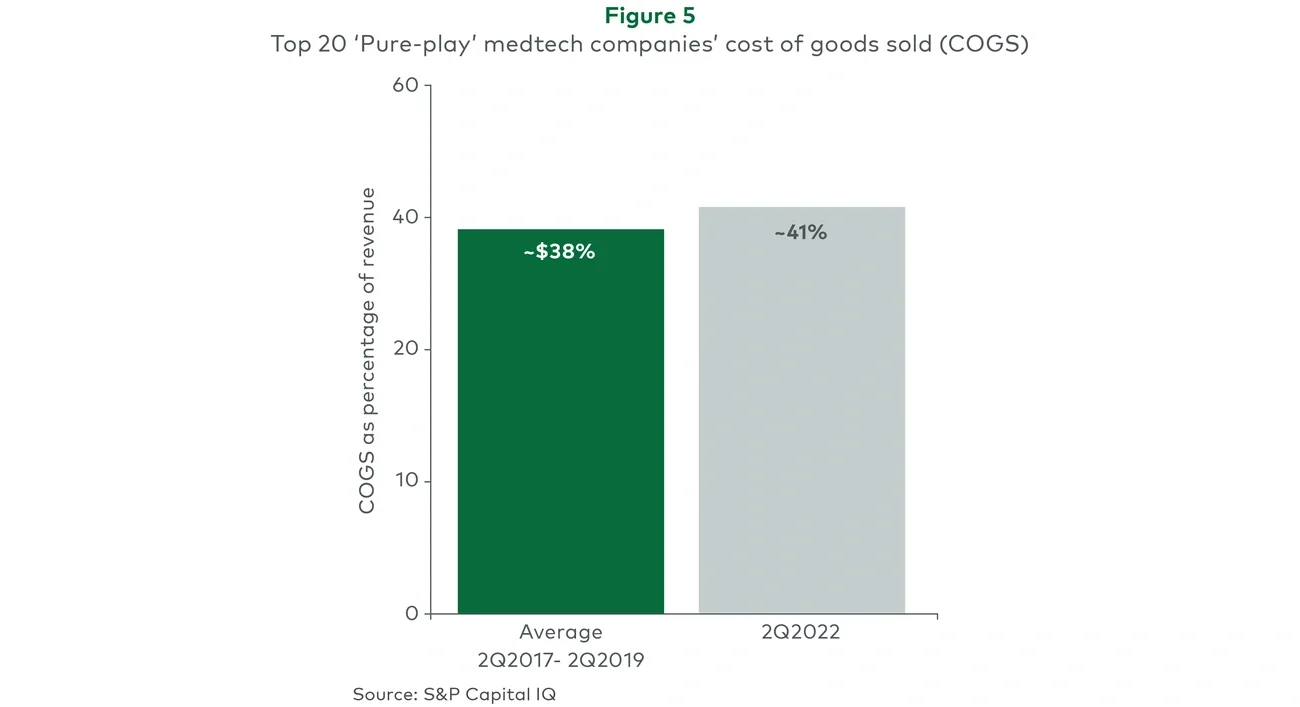

The acuity of these supply chain issues can be demonstrated by the example of semiconductor chip shortages: 2022 chip lead times are nearly 2x the average of those from 2017 to 2020. While chips appear to be a single component part, the vast majority of all medtech products leverage chips in some way, with two-thirds of all medtechs estimating that chips are used in over half of their products (AdvaMed, 2022). Further, almost every medtech product is produced using automated lines that require chips to operate. Chips are even used in products that help sterilize operating environments between medical procedures. Clearly, a shortage in chips has serious implications across every area of the healthcare system, threatening its very functioning.

-

Supply chain issues have clearly become a major source of disruption for medtech, and despite some recent improvements on the margins, instances of these challenges are likely to continue across medtech segments in the near future. This is driven by the facts that it takes a complex ecosystem like the medical supply chain time to fully mitigate challenges, that there are likely challenges that have not yet fully manifested and will emerge in coming months, and that the disruption was driven not just by external factors but also by underlying, pre-existing strategic and operational decisions that made the ecosystem susceptible to these shocks, and it will take time for the industry to assess, resolve existing issues, and refine and deploy a new approach.