The current state of physician practice consolidation

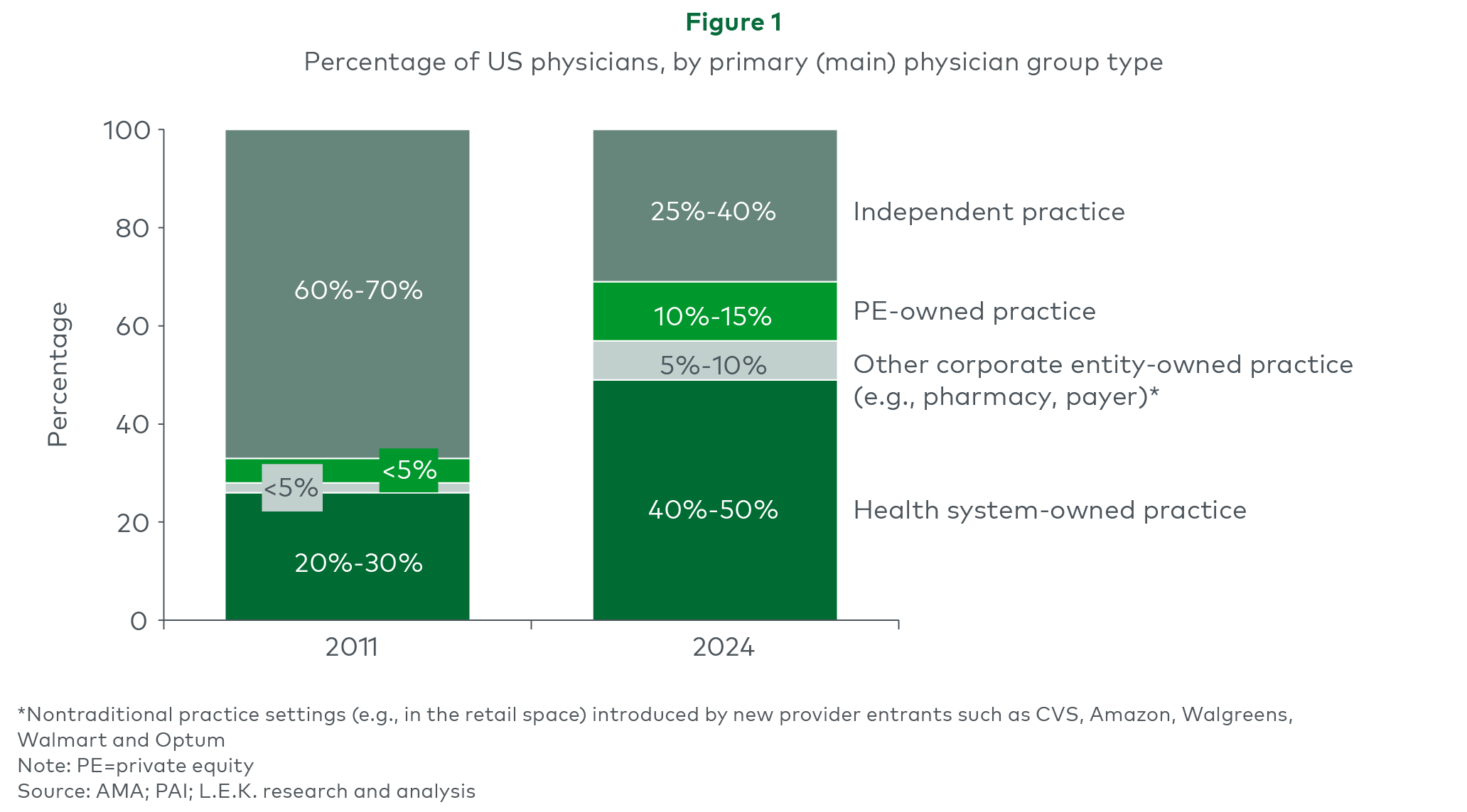

Over the past 15 years, the U.S. physician practice landscape has transformed. In 2011, more than 60% of physicians practiced in small, independent groups. In 2024, more than 60% of physicians were employed by a health system or a private equity (PE)- or corporate-owned group (see Figure 1).

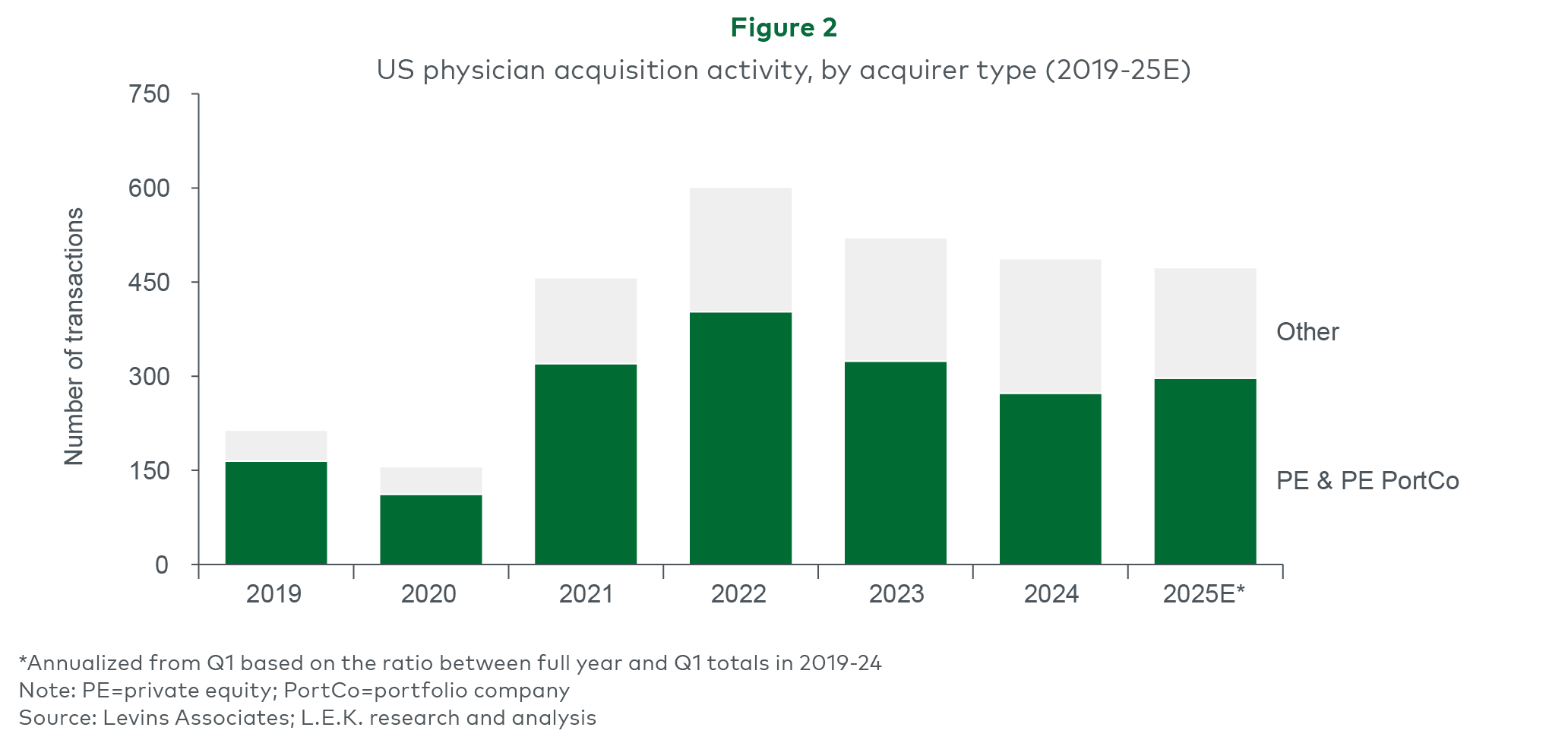

Acquisitions by PE-backed PPM platforms and other strategic acquirers of multi-site providers (e.g., insurers, distributors) have accelerated this trend. From 2019 to 2024, there were more than 2,400 physician group transactions in the U.S. (see Figure 2).

Specialty-level PPM trends and headroom

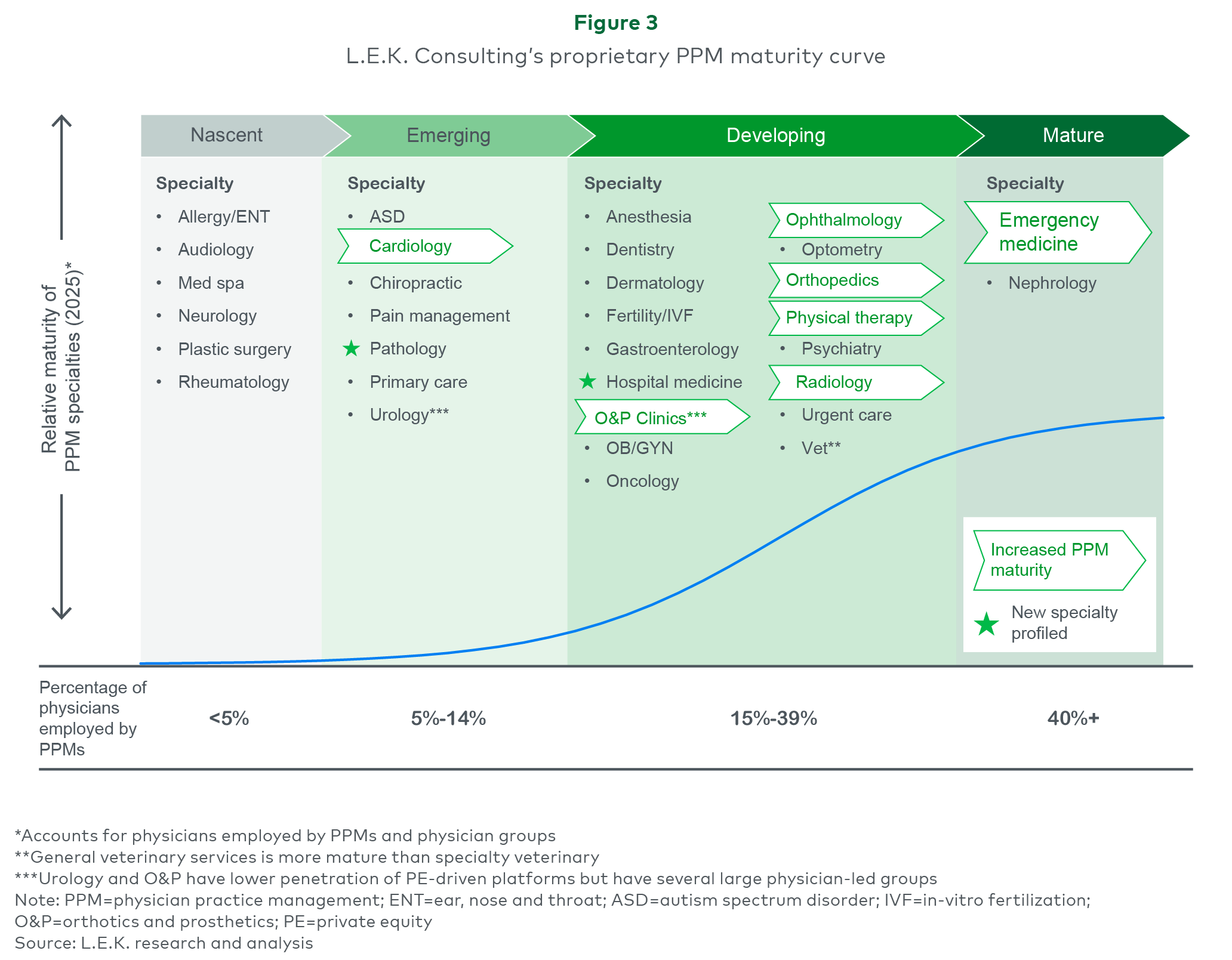

Given significant PPM deal activity over the past four years, L.E.K. Consulting has updated its proprietary PPM maturity curve (see Figure 3). No specialties have reverted to a lower “maturity” category, but several have seen significant activity in recent years and moved up:

- Nascent to emerging: Cardiology has seen accelerated rates of consolidation, with an increase from one PE-owned group with seven locations in 2019 to 50 PE-owned groups with 320 locations in 2023.

- Emerging to developing: Ophthalmology, orthopedics, physical therapy, radiology, orthotics and prosthetics clinics have all experienced continued practice consolidation and growth in the number of physicians employed by large, scaled groups.

- Developing to mature: Emergency medicine is the only specialty to move to the mature category, joining nephrology. Emergency medicine is increasingly concentrated with large groups like Team Health, Sound Physicians and SCP Health.

We have also added two new specialties to our PPM curve analysis, denoted with a green star: pathology (emerging) and hospital medicine (developing).

Significant consolidation opportunities remain across specialties. In 13 of 32 specialties we tracked, less than 15% of physicians are employed by a PPM or large group platform. Of the remaining specialties, 17 are still developing and present additional roll-up opportunities for investors, health systems and other strategic buyers.

Looking ahead: consolidation endures

We believe physician practice consolidation remains a long-term, secular trend in U.S. healthcare. The advantages of scale are clear. PE investors and strategic consolidators will continue to find opportunities as one of America’s last great cottage industries matures toward sophisticated, integrated models.

To succeed during the next chapter of consolidation, however, U.S. PPM platforms, investors and strategic consolidators will need to navigate an evolving set of trends and challenges:

Strategic implications and imperatives

The next wave of value requires corporations and investors to combine specialty-specific expertise, value creation initiatives and data-driven market selection.

Key takeaways for PPM/MSO platforms and investors

- Ensure the model creates ongoing value for member physicians. With increased expectations and extended and uncertain hold periods, it is critical that PPM/MSO platforms create real value for member physicians, especially between transactions.

- Aim where white space and value creation potential combine. Identify practices in nascent, emerging and developing PPM specialties that have white space to pursue and would clearly benefit from value creation levers that an MSO can provide (e.g., ancillary revenue stream capture).

- Be mindful of roll-up challenges in less mature specialties. Although many specialties have low PPM penetration, capturing white space in some requires overcoming real structural hurdles (e.g., limited value of a conventional MSO).

- Use data to de-risk growth moves. Target platform/MSO growth with geographic precision — e.g., where share of independent/small practices remains high, competition is limited and payers favor scale. Retain expansion flexibility (tuck-ins, de novos).

Key takeaways for hospitals and health systems

- Modernize the menu of physician relationship models. Direct physician employment is one option, but health systems can develop joint venture frameworks, MSO models and other structures to increase alignment with PPMs and independents where these models increase chances of success.

- Ensure physician value proposition remains competitive. As scaled platforms enter a system’s markets and grow, expectations and opportunities to differentiate will evolve, and so should the system’s physician group models.

- Take a data-driven approach to applying the right model by market and specialty. Competitive dynamics, value to the system and physician needs will differ significantly by market and specialty. Data and effective analysis can identify the right model for each market situation.

- Use offense as the best defense to win where ownership is key. Identify must-win situations and apply the full toolkit — acquisition, ASC and other ancillary co-ownership with physicians, etc. — to secure the capacity that the system and its patients need.

- Partner deliberately where counterparties are better placed. Partner with scaled platforms that can better meet the system’s needs. In doing so, seek opportunities to align incentives and co-create enduring value for physicians and communities.

How L.E.K. delivers results

L.E.K. has decades of provider experience across a range of specialties, including engagements with high-performing PPMs and health systems. We build on this knowledge base to deliver a full range of services to our clients, including transaction support (e.g., buy- and sell-side due diligence) and value creation services.

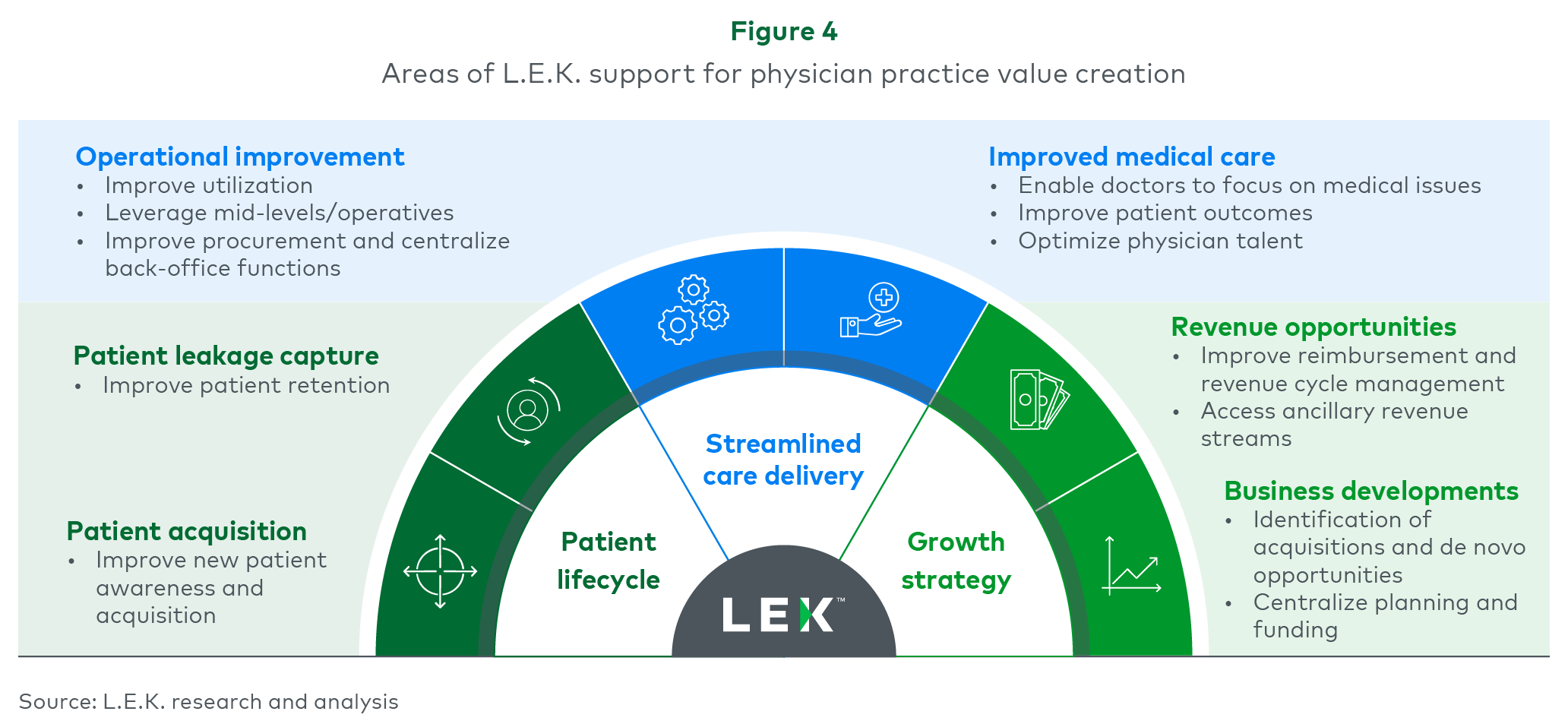

Value creation is critical for providers to improve profitability, grow their business and drive return on investment (ROI). We help optimize the patient life cycle, streamline care delivery/ operations and pursue growth initiatives (see Figure 4).

Seeking transaction support or ready to accelerate value creation for your business? Reach out to L.E.K.’s Healthcare Services practice for additional PPM insights or to discuss how we can unlock growth and efficiencies for your organization and increase ROI.

Contact us for more information.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

08152025090826