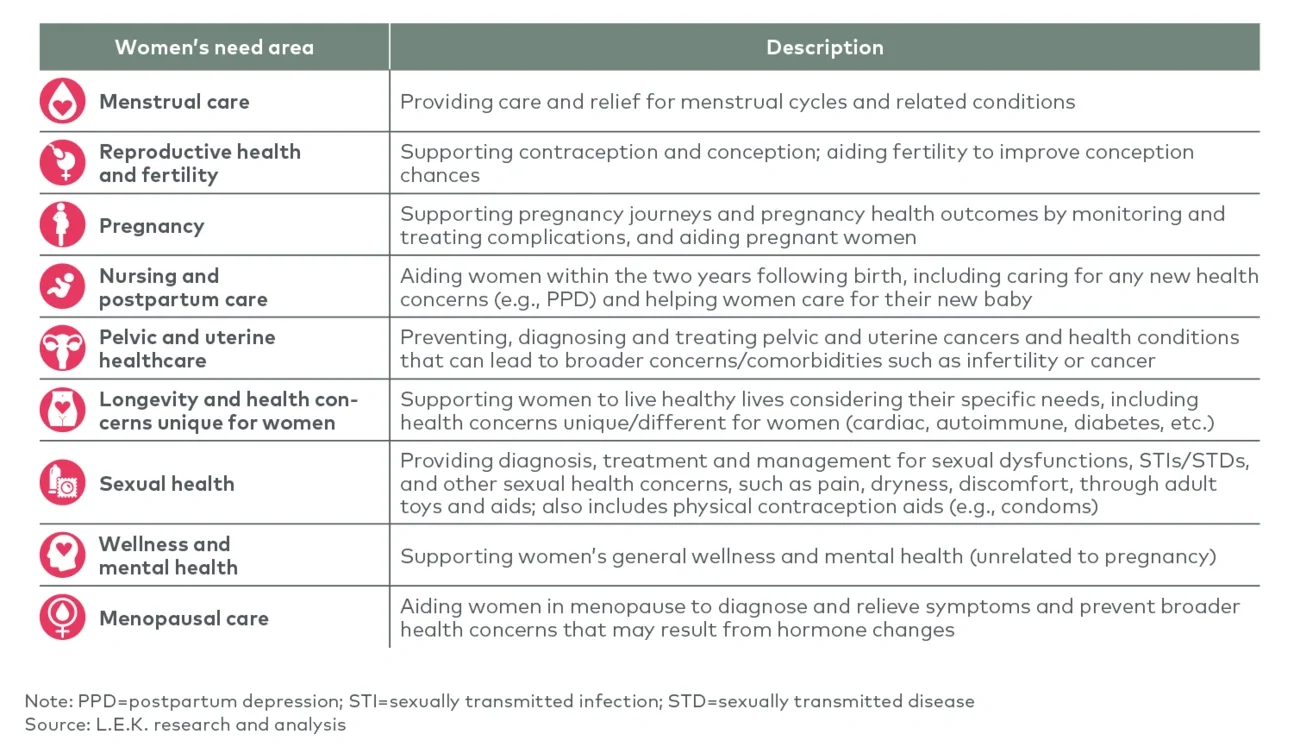

Women’s health is a broad area within healthcare and consumer health, encompassing all health concerns and conditions that affect women and those with a uterus throughout their life. Broadly, women’s health conditions and concerns can be grouped into nine key health needs, mapped across key points in each patient/consumer’s life span (see Figure 1).

Executive Insights

Decoding Femtech Consumers: Defining Needs and Segmentation in Women’s Health

Decoding Femtech Consumers: Defining Needs and Segmentation in Women’s Health

January 10, 2024

Key takeaways

Although Femtech is quickly driving towards innovating for women’s health consumers, unmet needs still exist, namely for pelvic and uterine care, maternal health and family building, and wellness/mental health; specific unmet needs exists for solutions that drive broader access to care, increase consumer knowledge about their health status and increase treatment efficacy, such as digital care delivery solutions and diagnostic tools/monitoring devices.

For maternal health and family building consumers, unmet need is highest within the postpartum period, specifically for solutions that support a consumers’ mental health; for consumers in the pregnancy segment, unmet need is highest for traditionally stigmatized conditions such as miscarriage and for high-risk pregnancy support; for consumers currently considering or attempting pregnancy (categorized as reproductive health and fertility consumers), unmet need is highest for egg freezing, surrogacy and donor services, and infertility treatments.

Maternal health and family building consumers fall into 4 key segments based clustering across 11 key behavioral and demographic criteria: the wellness seeker, the fertility maven, the loyal postpartum parent and the patient; each segment has unique needs and implications for customer lifetime value.

To drive forward maximum impact for women’s health and femtech solutions, bespoke consumer decoding, including targeting, messaging and value proposition definition within each segment is crucial; successful innovations tailor solutions to consumers’ psychological profiles, draw connections between groups of unmet needs and prime end to end solution development through strategic segment overlap.

Figure 1

Overview of areas of women’s needs

Image

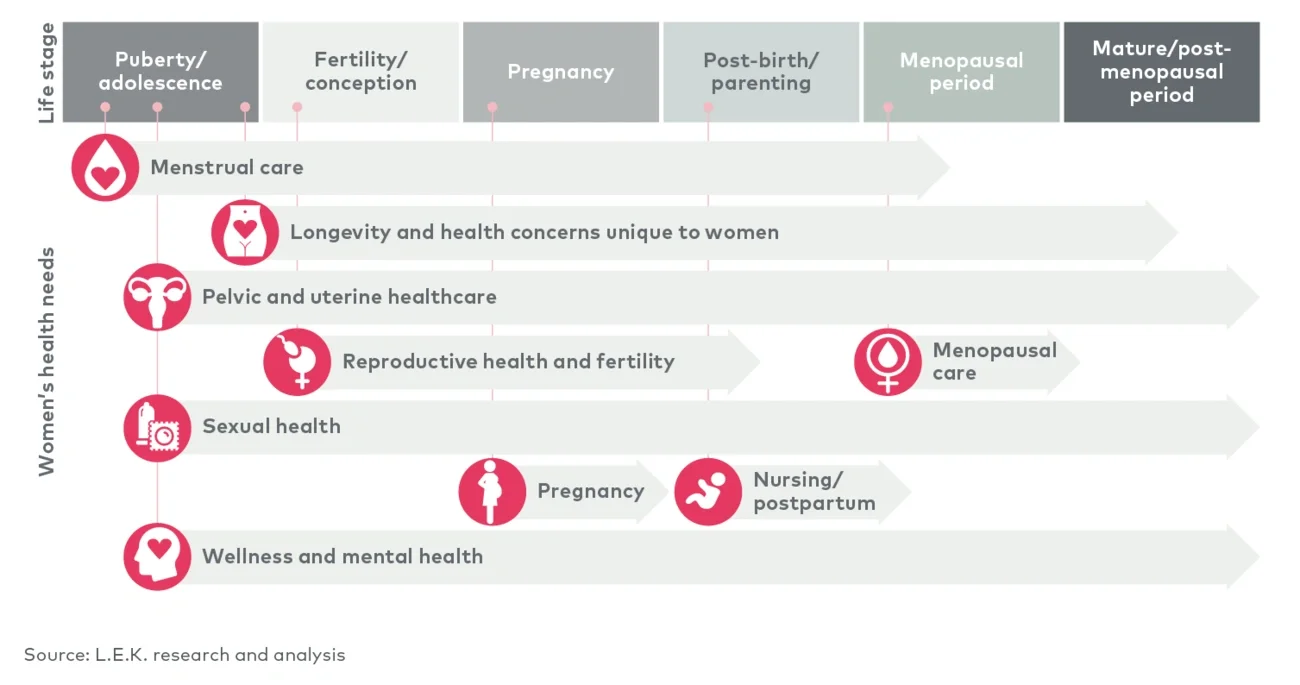

Across these health needs, the target patient/consumer and unique challenges of treatment and unmet needs of women differ. For example, some of these conditions are female or uterus specific, such as menstrual care, menopausal care and pelvic health (see Figure 2).

Figure 2

Mapping key women’s health segments to life stages

Image

Some of these conditions are specific to women but often also involve a partner or child, such as the maternal health and family building (MHFB) segments (defined as reproductive health/fertility, pregnancy, and nursing and postpartum). Some of these conditions affect both genders but have an outsized or differential effect on women; for example, autoimmune disease, severe obesity and chronic conditions such as migraine all disproportionately affect women, while cardiac disease and sexually transmitted infections display different indicators among women.

Finally, women’s mental health clearly faces unique challenges: Women have higher rates of depression, panic disorders, phobias, post-traumatic stress disorder, obsessive-compulsive disorder, major depression and eating disorders than men, and they are more likely to attempt suicide.

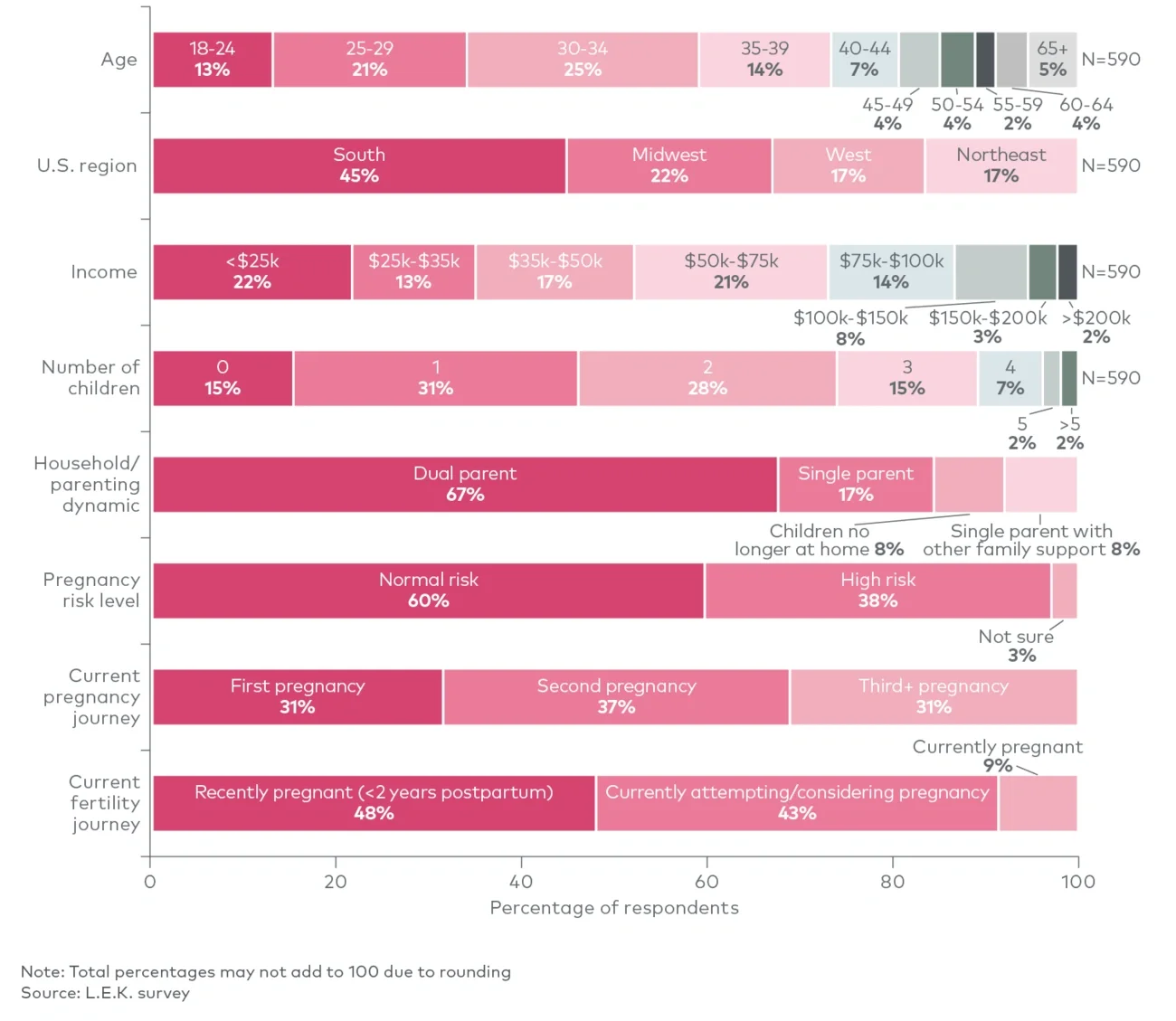

Intense innovation in the women’s health and femtech space is quickly moving forward to address these challenges. However, many solutions struggle to, first, truly identify the women’s health unmet need and pain point that needs to be solved and, second, to strategically target solutions to customer segments that resonate most with those needs. In order to better localize and understand the extent to which unmet needs exist within the women’s health landscape, develop a women’s health consumer segmentation scheme, and ultimately drive forward maximum impact in the women’s health space, L.E.K. Consulting surveyed a group of 590 U.S. women’s health consumers across ages, income brackets, regions and various family groupings (see Figure 3).

Figure 3

Demographic breakdown of US consumer survey

Image

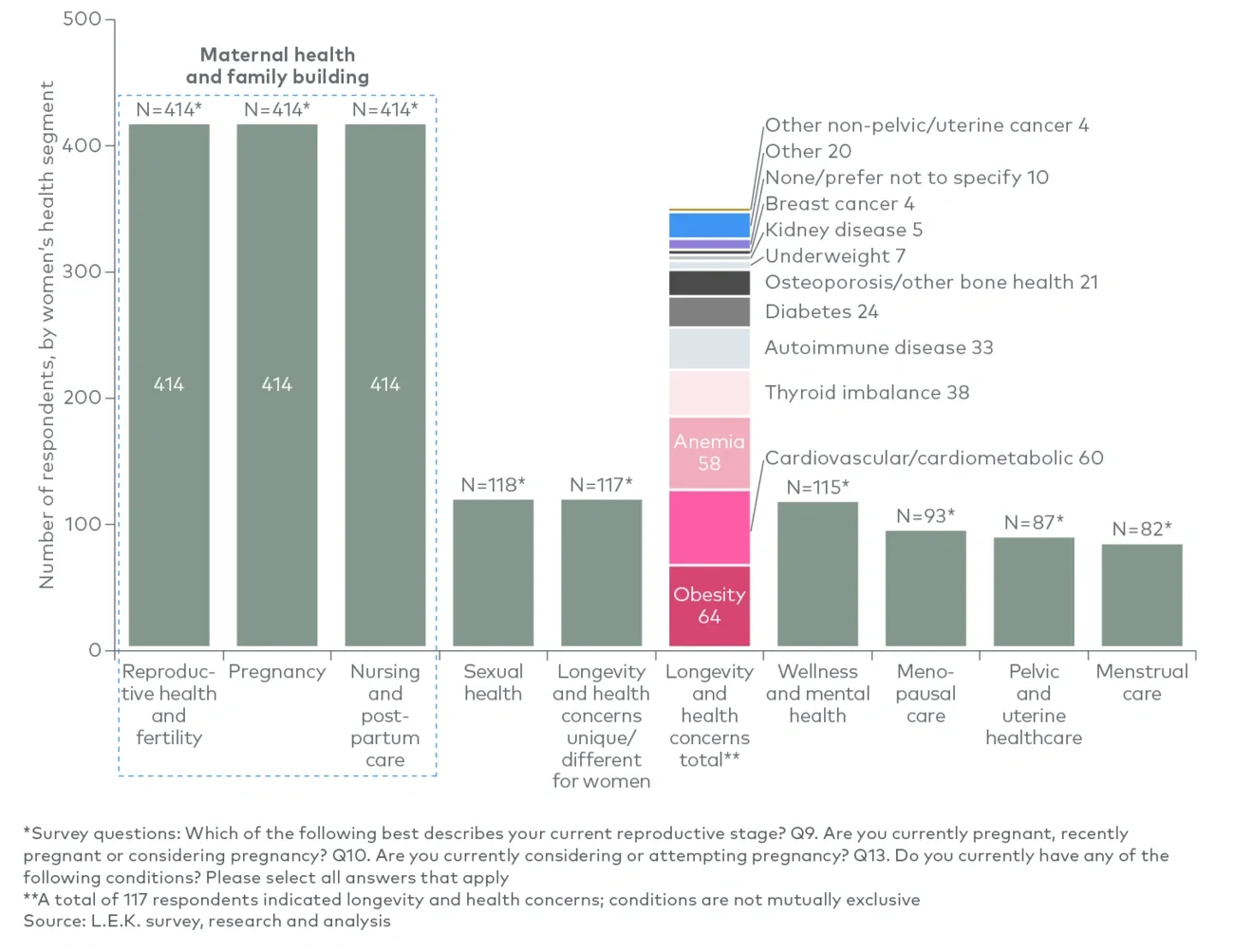

About 414 consumers fell into the MHFB segment, while sexual health, longevity and wellness/ mental health had over 100 responses. Within longevity, respondents spanned obesity, cardiovascular/cardiometabolic conditions, anemia, thyroid conditions and autoimmune disorders/diabetes, among other chronic conditions (see Figure 4).

Figure 4

Women’s health segment breakdown of US customer survey

Image

Beyond the obvious: What is an unmet need?

We asked consumers to think of unmet needs broadly as areas for which they perceived no solution to exist, either due to lack of access or lack of commercially available options. We explained to consumers that unmet needs are not necessarily needs consumers felt they would pay more to address, to ensure that the highlighted needs best represent market gaps vs. solely incremental value capture opportunities.

Clinical conundrums: Unmet needs across women’s health clinical segments and solution types

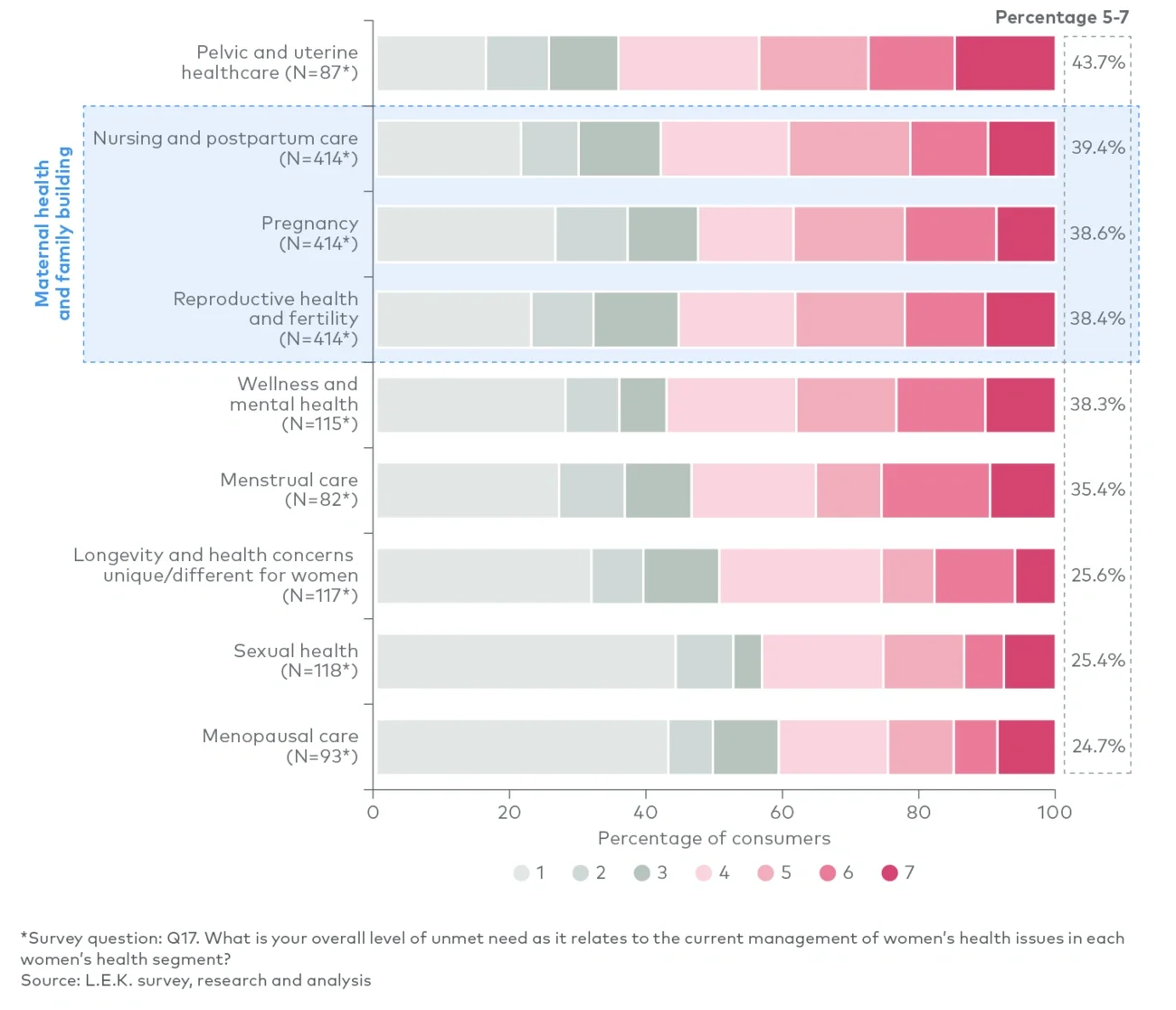

By women’s health condition/concern area, consumers indicate that the highest unmet need exists within pelvic and uterine care (including issues such as uterine, cervical and ovarian cancers; pelvic inflammatory disease; endometriosis; and polycystic ovary syndrome) and MHFB areas, closely followed by wellness and mental health (see Figure 5).

Figure 5

Consumer feedback on key unmet needs across women’s health segments

Image

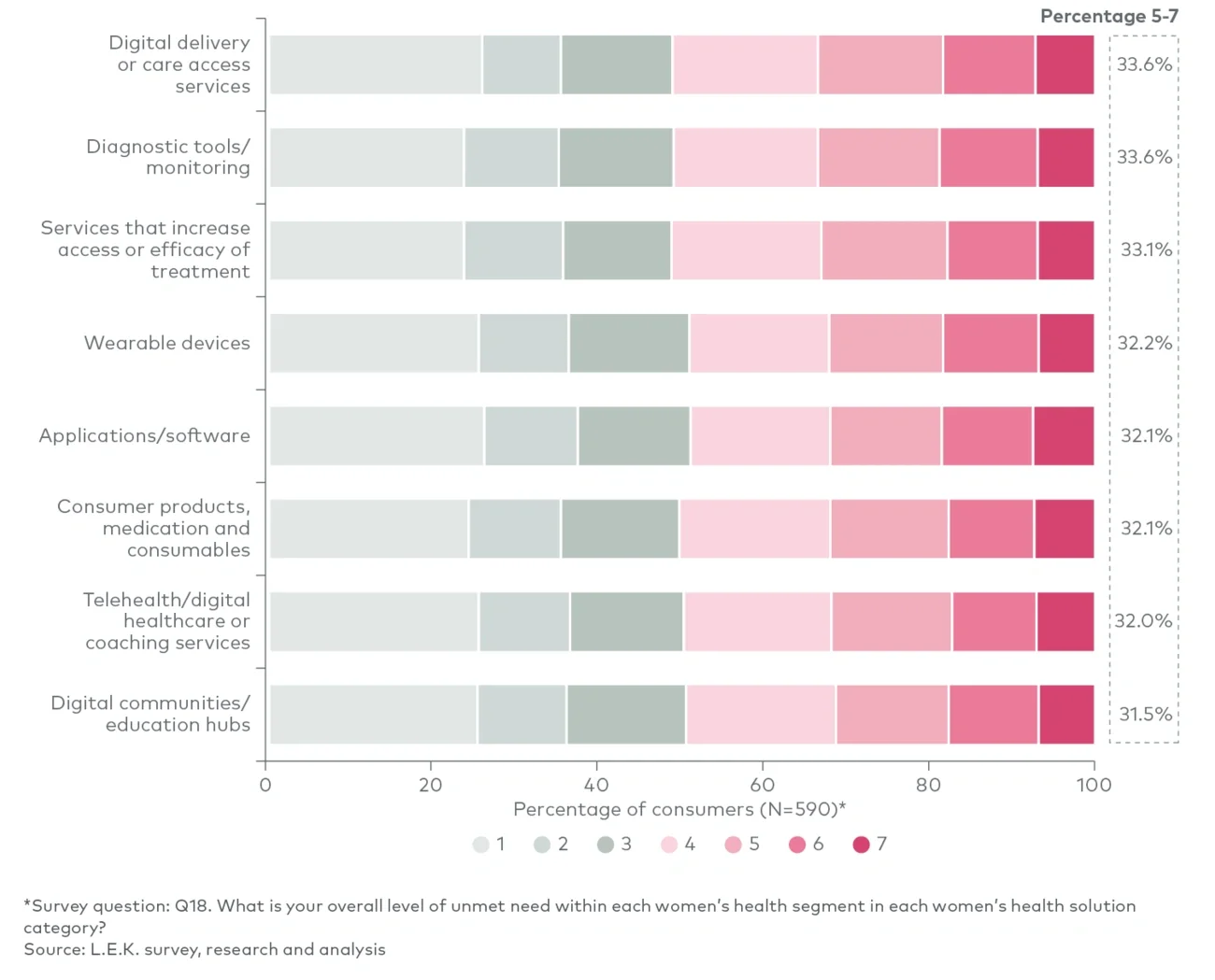

By solution type, consumers indicate the highest unmet need is for solutions that drive broader access to care, increase consumer knowledge about their health status and increase treatment efficacy, such as digital care delivery solutions and diagnostic tools/monitoring devices (see Figure 6).

Figure 6

Consumer feedback on key unmet needs across women’s health solutions

Image

Overall, approximately one-third to just under one-half of women’s health consumers state that they have a highly unmet need within a specific clinical area or for specific solution types, indicating high existing unmet needs within this core consumer group.

Maternal and contraception mysteries: Unraveling unmet needs in maternal health and family building

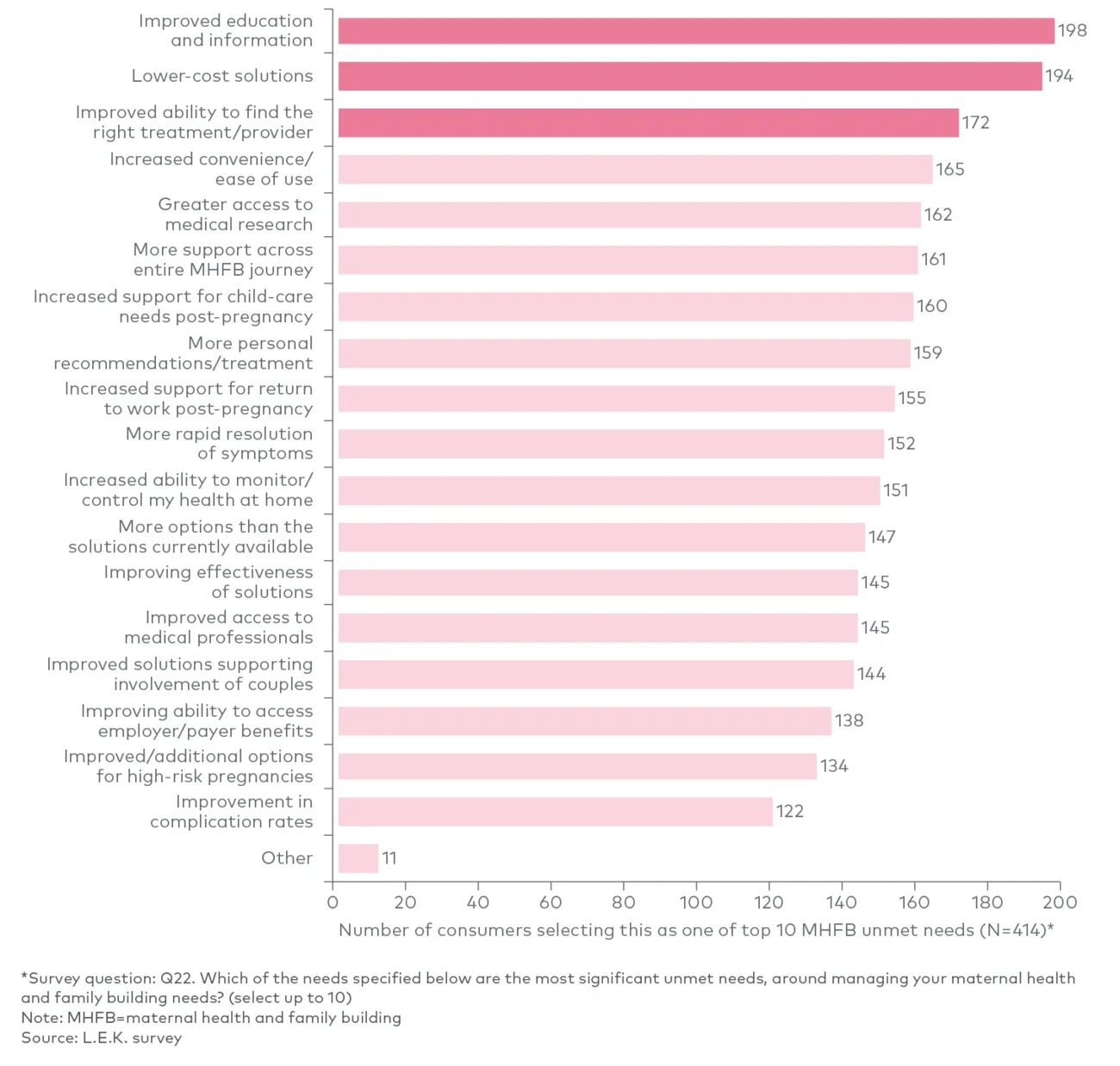

Although the area is relatively more mature in terms of investment, high unmet need still exists for MHFB consumers. These consumers indicated that improvement in consumer education and care access — through lower-cost solutions and improved ability to find the right treatment or provider for a consumer’s unique question, condition or symptom — is the most important area where needs are not currently met (see Figure 7).

Figure 7

Consumer feedback on key unmet needs within MHFB

Image

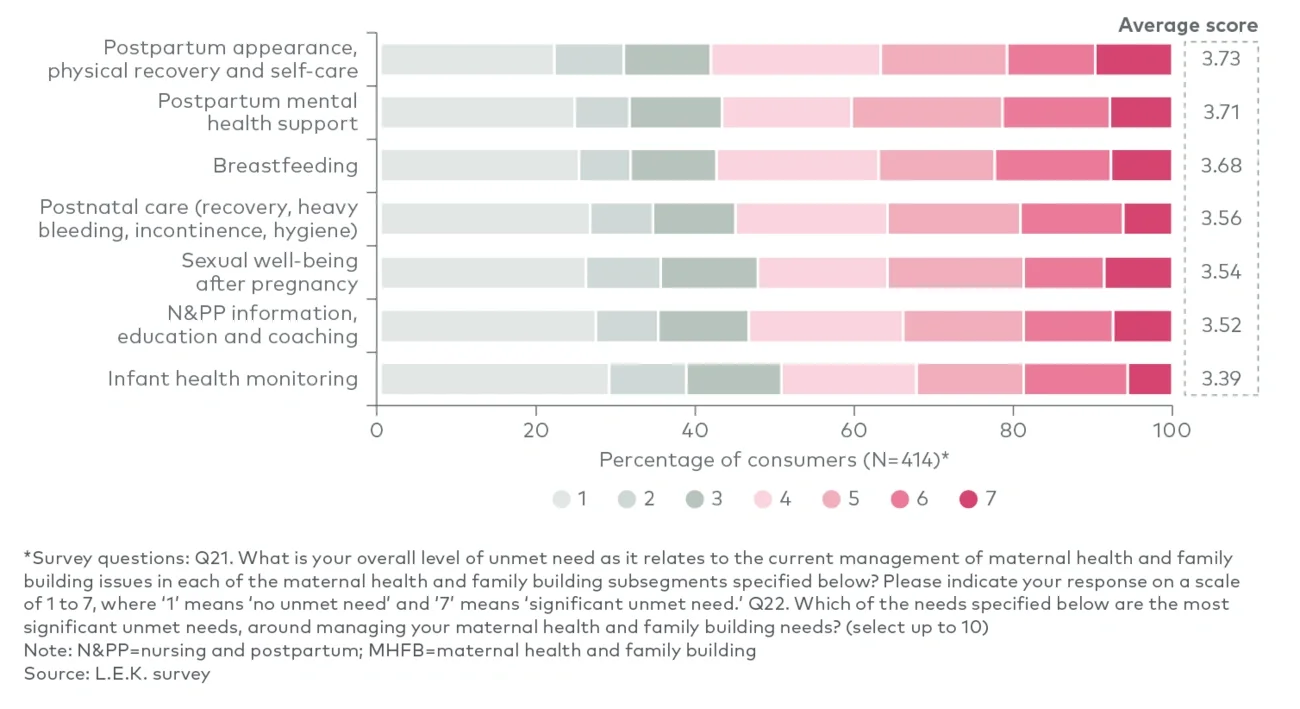

Unmet needs vary by each MHFB segment, dependent upon specific pain points each consumer faces within specific stages of the maternal health and family building journey. Unmet need is highest on average within nursing and postpartum care, specifically for solutions that support the new parent in their self-care or mental health (see Figure 8).

Figure 8

Consumer feedback on key unmet needs within pregnancy

Image

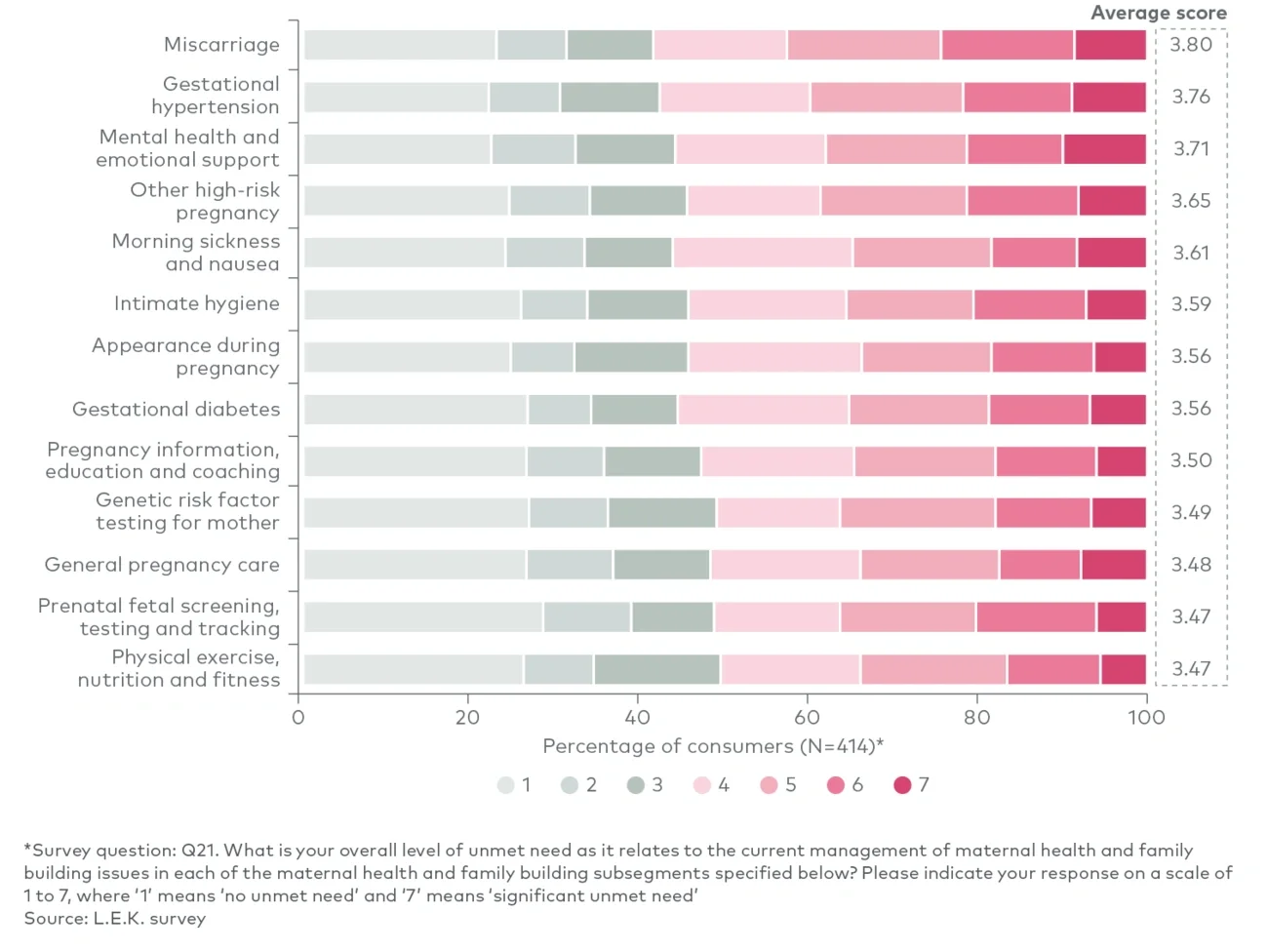

Within pregnancy, consumers indicate having a need for support for traditionally stigmatized conditions such as miscarriage and for high-risk pregnancy support surrounding symptoms such as gestational hypertension and mental health (see Figure 9).

Figure 9

Consumer feedback on key unmet needs within N&PP and MHFB

Image

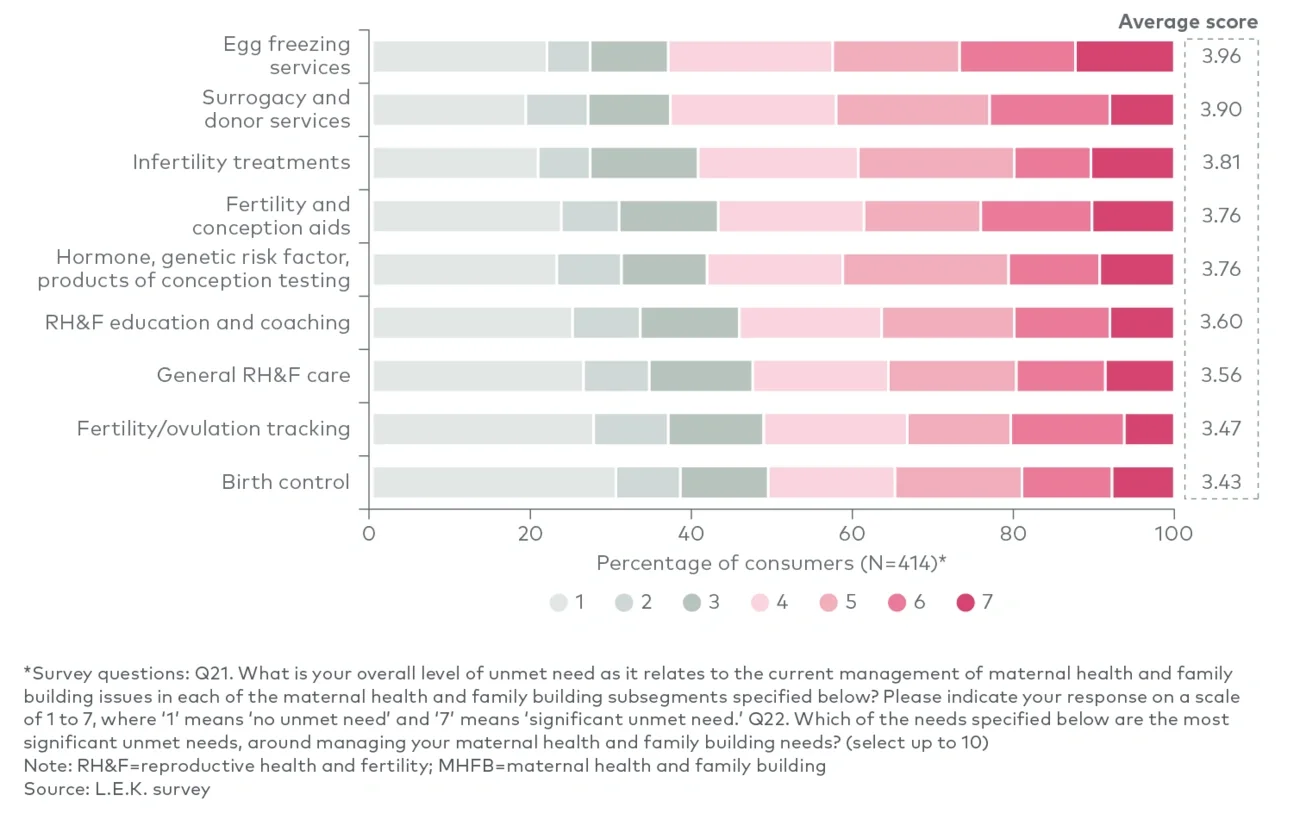

Finally, within reproductive health and fertility, consumers indicate the highest unmet needs for access to specific services that are becoming increasingly common as the age at which women give birth to their first child continues to increase, such as egg freezing, surrogacy and donor services, and infertility treatments. Fertility conception aids and diagnostic testing for genetic risk factors and fertility hormones also rate as unmet needs for MHFB consumers (see Figure 10).

Figure 10

Consumer feedback on key unmet needs within RH&F and MHFB

Image

The maternal and reproductive health spectrum: Segmenting consumers for tailored solution development

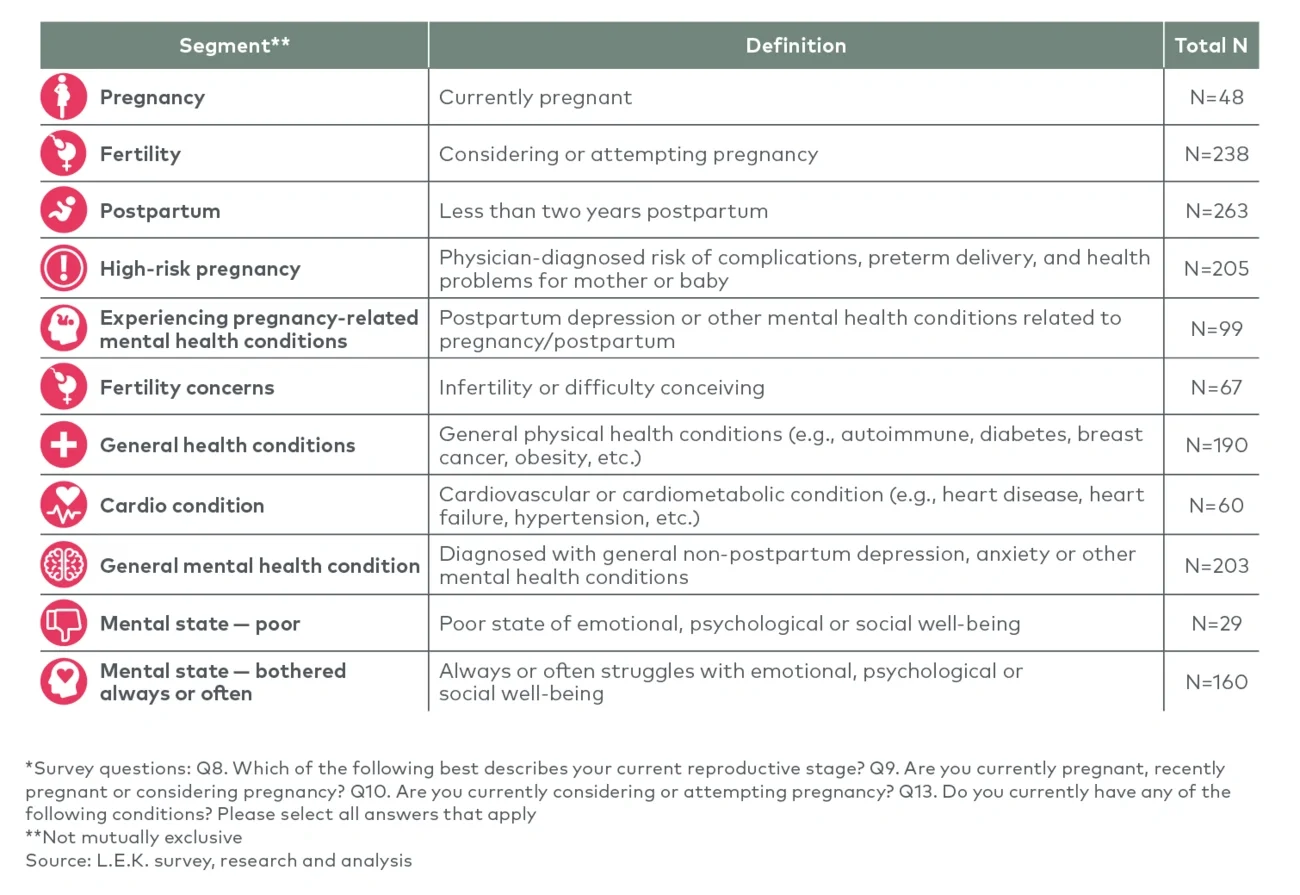

To better understand MHFB consumers and to tactically guide marketing within the femtech space, we next undertook statistical cluster analysis to group women’s health consumers into personas by key behavioral and demographic criteria (see Figure 11), including:

-

Current life stage: Segmenting consumers by currently pregnant, considering or attempting pregnancy, or less than two years postpartum

-

Experience of mental health or general health conditions: Experience of conditions such as postpartum depression, other mental health conditions, high-risk pregnancy, infertility or specific chronic conditions

-

Self-reported mental state: Self-reported state of emotional, psychological or social well- being when taking the survey and degree to which respondents self-reportedly struggle with their mental state

Figure 11

Grouping consumers into personas, by key behavioral and demographic criteria*

Image

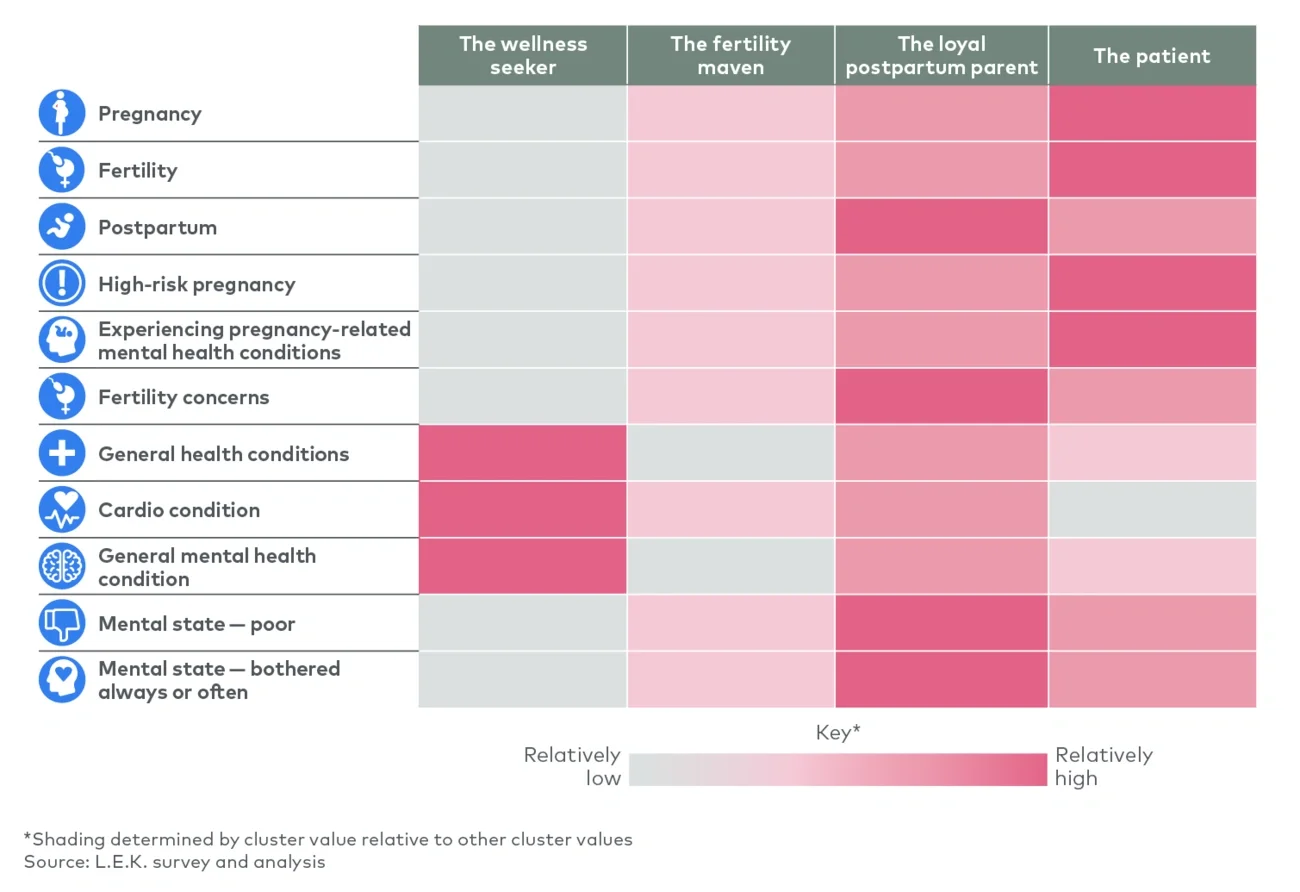

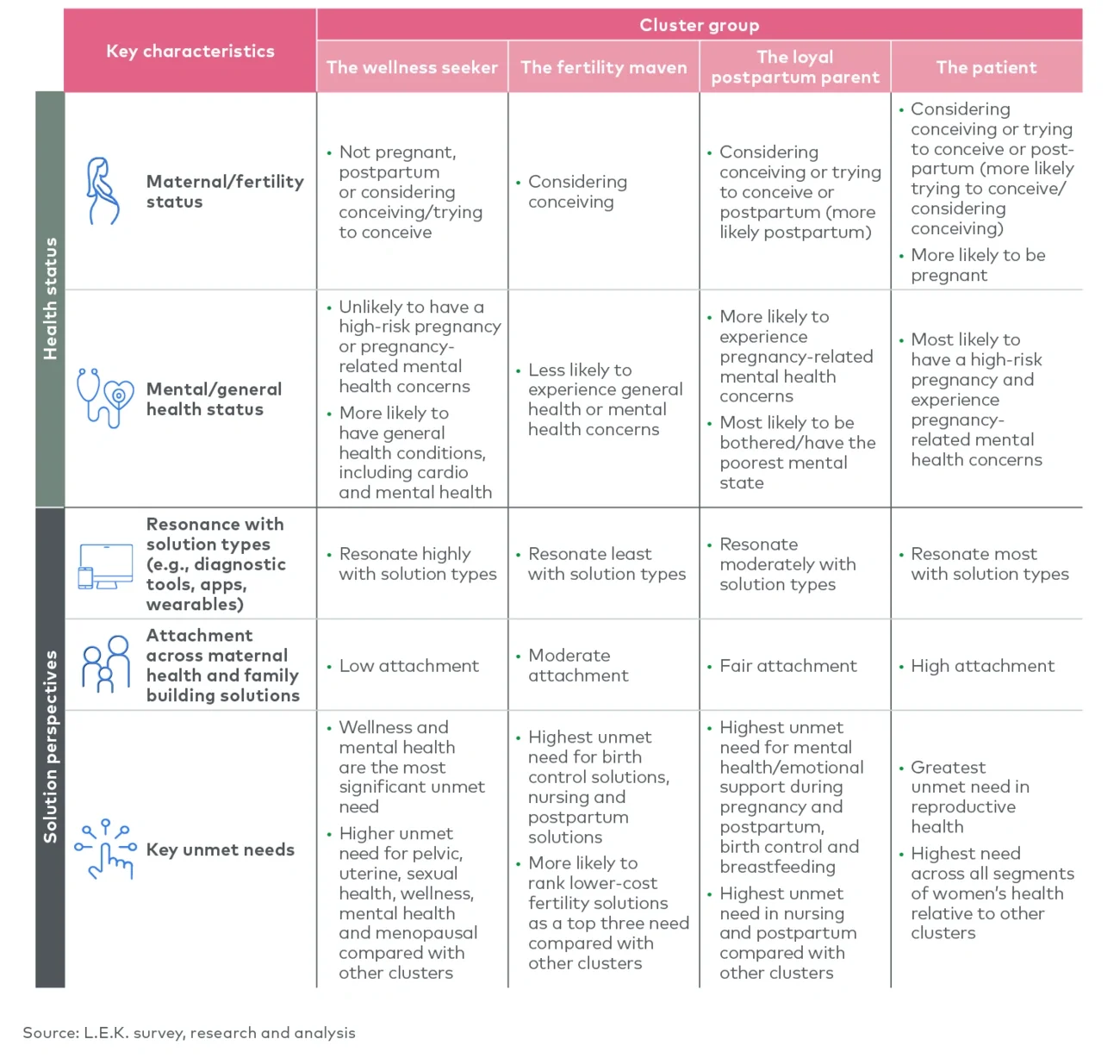

This technique yielded four key personas of women’s health consumers with unique behavioral and demographic profiles (see Figure 12), detailed below:

-

The wellness seeker: Consumer who has a distinct need for wellness and mental health solutions, with high resonance in the need for specific solution types

-

The fertility maven: Consumer who is considering conceiving and currently evaluating a variety of products to use across the MHFB journey, with a specific need for low-cost fertility solutions

-

The loyal postpartum parent: Consumer who is most likely postpartum with specific needs for postpartum mental health and personal support

-

The patient: Consumer who is facing or undergoing a high-risk pregnancy (including likely experience of pregnancy-related mental health concerns) with the greatest need across all segments of women’s health

Figure 12

Top 4 key personas of women’s health consumers

Image

Each women’s health persona experiences a unique set of unmet needs, based on their specific life experience and perceptions, and resonates with and attaches to solutions differently. Attachment here refers to the likelihood to reutilize preferred solution brands that they have utilized in the past and can be directly mapped to customer lifetime value (see Figure 13).

Figure 13

Likelihood of top 4 personas to reutilize preferred solution brands that they have utilized in the past

Image

The wellness seeker: Requires specific solution types to meet wellness and mental health needs, with type depending on individual needs of each consumer. Wellness seekers also have higher unmet needs across various non-MHFB healthcare clinical areas, including pelvic/uterine health, sexual health and menopausal conditions. These consumers typically have the lowest attachment to solution brands — they are the most fickle and have a desire to try new brands even if they are highly satisfied with solutions they’ve used in the past.

The fertility maven: Requires solutions for current and future life stages including birth control, low-cost fertility solutions, and nursing and postpartum solutions, but is flexible across solution types to meet these needs. These consumers have higher brand loyalty and attachment than wellness seekers.

The loyal postpartum parent: Requires solutions specifically for mental health/emotional support in the pregnancy and postpartum periods, as well as solutions across postpartum and nursing. These consumers are likely to be the most bothered by their mental state/ have the poorest mental state, and as a result are fairly loyal to solution brands that have met their needs in the past. This correlation between mental state and solution attachment is hypothesized by the maternal health psychiatrists we spoke with to be due to human psychology; in times of hardship, consumers typically latch on to stability — in this case, solutions that have helped them.

The patient: Requires solutions to meet needs for a high-risk pregnancy, with additional high unmet needs across all segments of women’s health. These consumers are discerning in their solution preferences and are the most likely to reutilize brands they are satisfied with, implying the highest potential for customer lifetime value opportunity.

From gaps to solutions: Key tenets to guide innovative solution design and targeting in women’s health

Unmet need levels in women’s health imply a significant need for innovation. Although women’s health conditions typically have a higher burden-to-funding ratio compared with conditions that disproportionately affect men, women’s health unmet needs — felt by around 35%-45% of the addressable population, based on our work — compare with analogs in other gender-specific areas of healthcare, such as prostate cancer and erectile dysfunction (reported at about 42%-48%). Therefore, although levels of unmet need are commensurate with male-specific conditions, women’s health is not getting its fair share of funding. To drive impact in the evolving femtech and women’s health space, innovators should focus on developing solutions and investing in spaces that deeply address consumers’ unmet needs and consider the following calls to action:

- Target solutions to the appropriate customer persona to maximize uptake

Each consumer persona implies a unique set of clinical and solution-specific needs within MHFB. As the femtech space continues to evolve, it will become increasingly important for solutions to differentiate themselves with a clear value proposition and clear customer targeting strategy. Companies offering specialized or individualized care or solutions, such as Plume (transgender care), Oula (maternity care) and Adyn (personalized contraception), have delivered on their targeting and value proposition strategies toward specific consumer groups. - Meet consumers where they are in their need and psychological profiles — empathy goes a long way

For example, the loyal postpartum parent is the most likely to have the poorest mental state and to need a sense of trust with brands they utilize. Solutions can utilize empathetic techniques in messaging and solution design to become a trusted partner to consumers and drive eventual repeat use of brands. This principle is brought to life in solutions redesigning traditionally painful procedures, such as intrauterine device insertion. - Draw connections between groups of unmet needs based on consumer behaviors and personas to maximize impact within a care episode

Although unmet needs are often specific to a single clinical area or condition, solutions can be considered “end to end” across a variety of unmet needs in a care episode. For example, Clue offers consumers menstrual cycle tracking, fertility window tracking and fertility-specific consumer educational content on a single platform. Similarly, Betty’s Co. offers gynecological and wellness care as well as consumer sexual health products on its ecommerce platform. - Target innovation in one area to prime end-to-end platform growth adjacencies within associated clinical areas, given customer overlap across segments

For example, there is significant overlap between managing pelvic/uterine health conditions and falling within the MHFB segments (clinical research reports up to 45%-55% of pregnant and postpartum women experience a pelvic floor disorder). A brand like Elvie showcases this well with its dual postpartum and pelvic floor therapy offering.

Decoding women’s health consumers is complex, and involves examination of the behaviors, preferences and lens through which women and those with a uterus view their care and solution choices. Ultimately, all it takes to decode a women’s health consumer is offering a solution that incorporates that person’s voice into the design and care delivery process.

For more information, please contact medtech@lekinsights.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC

Questions about our latest thinking?

Questions about our latest thinking?

Related insights

You might also be interested in these insights.

English