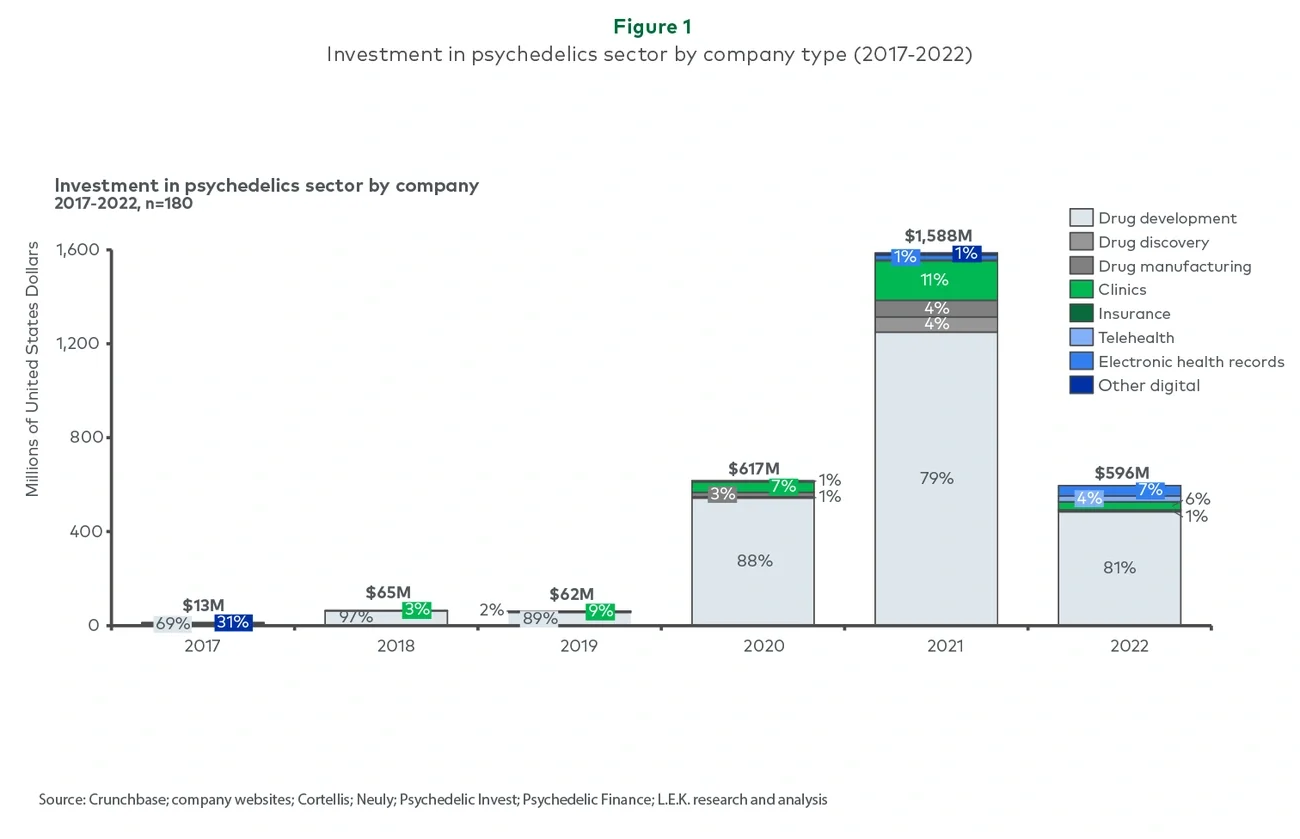

2022 saw continued funding directed to new drug development companies in the second half of the year, with Lusarius Therapetuics and Sensorium Therapeutics recording $60 million and $30 million in their respective Series A funding rounds. These investments, as well as continued private placements and venture capital fundraising, demonstrate continued investor confidence, in even the earliest-stage psychedelics companies. Drug development continues to account for the majority of funding, with around 80% of funding in both 2021 and 2022.

Companies supporting psychedelic drug development activities, including clinics and digital health have raised around $370 million since 2017. For example, during 2022, $2 million in seed funding was invested in Enthea, an employee benefit plan administrator focused on psychedelics-assisted therapy, and Revitalist, a ketamine clinic network, raised $5 million.

Looking forward, the level of funding in the psychedelics industry is likely to mirror the stormy biotech and macro economy — with potential to outperform once more. As trial results trickle in and confidence in assets increases, funding levels are likely to tick steadily upwards. Notably, there is unlikely to be a single trial result that dictates the future of the market, given the wide variety of combinations of compounds and indications trialled.

Capital is likely to become harder to come by, leading to consolidation of psychedelics companies and programmes and mergers and acquisitions shifting the landscape of market players. These trends could already be seen in 2023 with the acquisition of Eleusis by Beckley Psytech and the narrowing of pipelines across multiple companies.

2023 should prove to be another resilient year for the psychedelics sector, based on the enduring potential for psychedelics to transform mental health care and beyond. As the market begins to realise the scale and specifics of this ambition and companies step into launch planning, funding is likely to shift into the various forms of infrastructure required to realise this goal.

To find out more, contact Adrienne Rivlin, Partner.