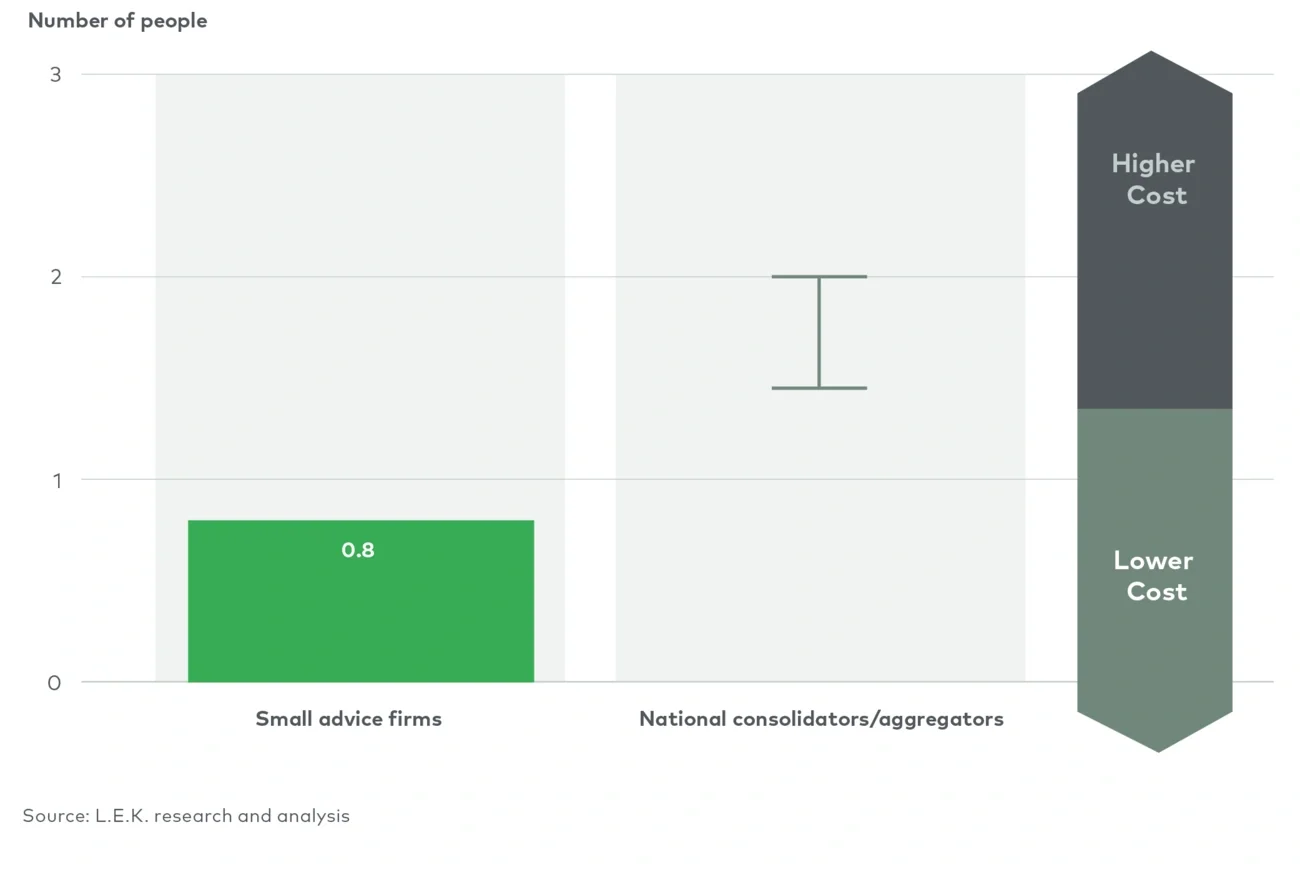

Some evidence does support the generous explanation that better specialisation frees up time for planners to service clients, and indeed planners in national advice firms on average handle 1.5x to 2x more assets under management (and therefore fee income) per person than smaller firms do. However, we argue that more is at play here — namely, that the industry has yet to fully harness the power of scale and efficiency and that much more can be done to improve the cost-to-income ratio for advice firms and their investors.

An opportunity for change

Many financial planners are shareholders of their business and thus should have a keen interest in its commercial success. Financial prudence and longevity are at the core of the advice profession, and thus the same philosophy naturally should extend to the running of an advisor’s own business.

Although opportunities for significant value creation still exist for advice firms and their investors, realising true cost efficiency requires commercial and management sophistication. In defence of large firms, many realise the cost-out opportunities but face a market that continues to be weighed down by its own legacy.

Common complaints from our conversations with CEOs and COOs include the following:

- “Advisors are set in their own ways, and [their approach is] difficult (though admittedly not impossible) to change.”

- “Advisors like the paraplanners and admins they have worked with [before], and disturbing this arrangement will ruffle feathers.”

- “Cost has been taken out in things like property and [professional indemnity] insurance, so we can stop there without having to rock the boat too much.”

- “The focus is on M&A. We will figure out the integration and operating models later.”

However, these statements go a long way towards revealing structural issues that most advice firms have yet to tackle:

- Evidence suggests that the assumption ‘size = scale = operating leverage’ is often misguided and should not be considered inevitable.

- Advice firms too often fail to harness the potential of workflow simplification from vertical integration.

- Using too many platforms and tech systems ultimately drains time and increases the effort required to stay on top of things (e.g. dual keying problems).

- Technology adoption will falter without corresponding operating model changes.

- Enforcing the target operating model throughout the organisation, from top to bottom, requires dedication and follow-through.

Clearly, root-and-branch changes are required in order to transform an organisation’s target operating model and ultimately improve cost-to-income ratio. Yet many organisational leaders are products of the industry who may lack the tools to instigate an overhaul of the status quo. This need not be the case. COOs and chief technical officers who adopt the principles of good target operating model design can learn lessons that are essential for value creation in their advice firms.

Unfinished business in value creation

Advice firm leaders could start by recognising the distinction between a genuine, client- facing unique selling proposition and vital, behind-the-scenes functions. Consider Henry Ford, who is credited with popularising the first automobile but whose true innovation was the development of the groundbreaking assembly line, which enabled mass production of a complex but highly reliable product. Financial planning, in many respects, requires similar genius when it comes to operations.

Successful operating models follow several simple design principles:

- An operating model should reflect the cost of service. Because a firm’s advice services vary for different client segments, an effective operating model design should start with segmentation into at least three operating models within the business:

- One for telephony/remote clients

- One for standard face-to-face clients

- One for higher-value clients who might require more bespoke services

- Build for the future, not for today. Make sure the overall operating model is an accurate fit for the purpose of the organisation’s ambitions and plans for growth.

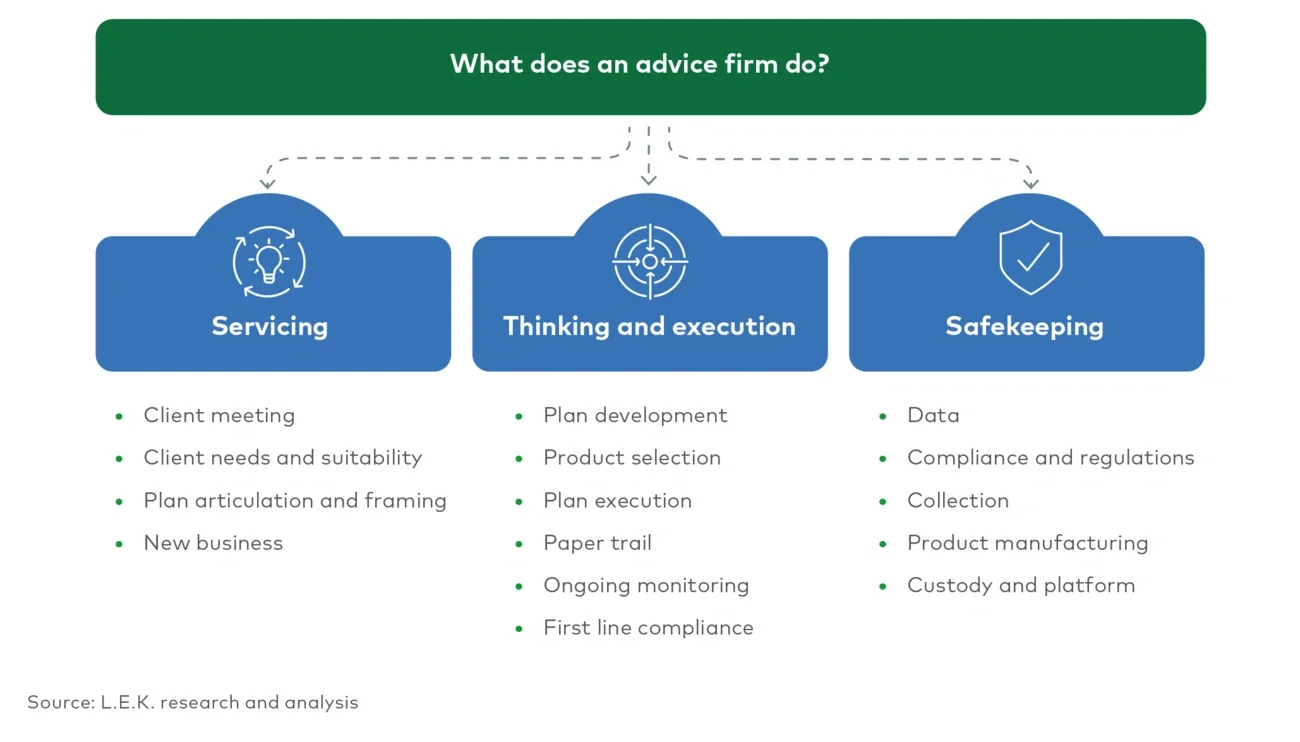

- Keep, reallocate, automate. Encourage a process where each function keeps any required tasks, reallocates tasks that can be performed in a cheaper role and automates as much as possible, e.g. an expensive planner should not be sourcing insurance quotes that an administrative team can provide (see Figure 3).