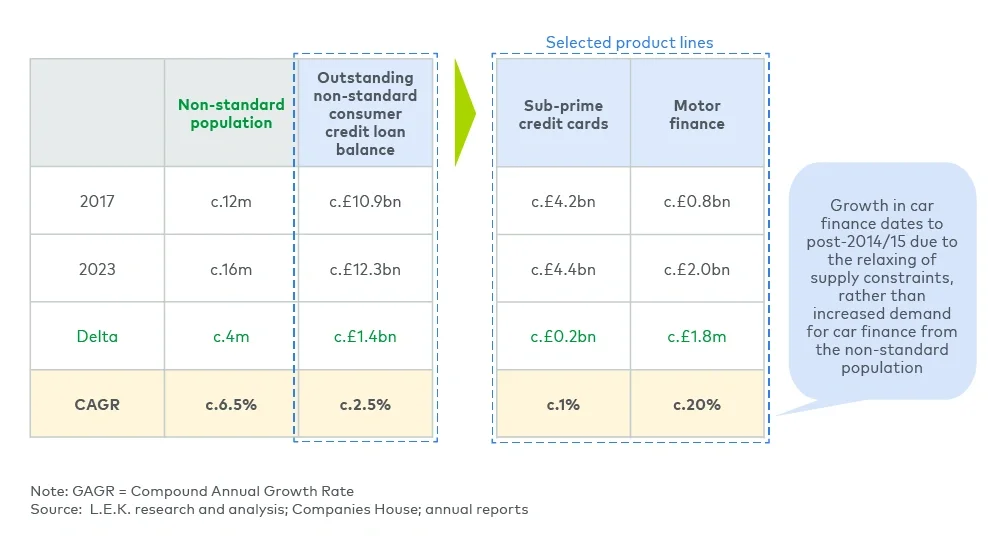

The Woolard Review, published in 2021, was a far-reaching review across both the demand and supply of credit in the UK. One of its major findings — at times overlooked by some, given the more prominent coverage of buy-now-pay-later regulation — is a call for the industry to do more to improve availability of credit amongst the UK population. We at L.E.K. Consulting fully subscribe to the Woolard Review’s conclusion that more needs to be done to improve credit access. Our work regarding the financially underserved population, who typically have credit history that falls outside mainstream underwriting criteria, reveals that this population is significant in size (16 million to 17 million consumers, or c.30% of all adults, up from c.12 million to 13 million in 2018) with unmet but potential commercially viable credit needs (£2 billion in balance).

In particular, our research finds that these households are facing material economic headwinds, and access to affordable credit is of crucial importance to 1) ensure their near-term economic well-being and 2) ensure that near-term economic conditions do not become entrenched so as to affect the long-term viability of these households as credible borrowers. Unfortunately, our market conversations also reveal that the supply of credit to these households will likely become more challenging in the near-to-medium term, as lenders become more conservative in their lending approach in times of economic uncertainty. In short, a perfect storm is brewing that requires urgent action.

In this Executive Insights, we summarise our latest research on this population (more conventionally known as the ‘non-standard population’ in the industry), covering both credit-demand and credit-supply dynamics.

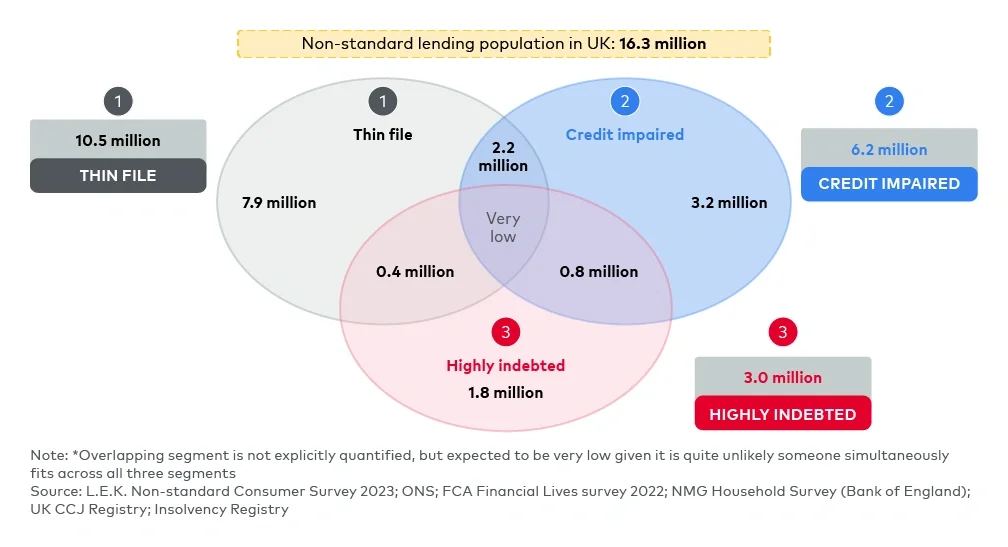

Large non-standard population with growing need for credit

We estimate that the population with non-standard credit needs comprises approximately 16 million to 17 million people, who fall into one or more of three categories (see Figure 1):

-

Thin file: low or no credit history (e.g. recent immigrants to the country or students who have not been able to build up credit); these households have a viable path to establishing a longer credit history

-

Credit impaired: poor credit rating, often linked to (temporary) disruptive life events (e.g. divorce, loss of job, health problems) leading to missed repayments

-

Highly indebted: individuals who have taken on too much debt and cannot afford to repay