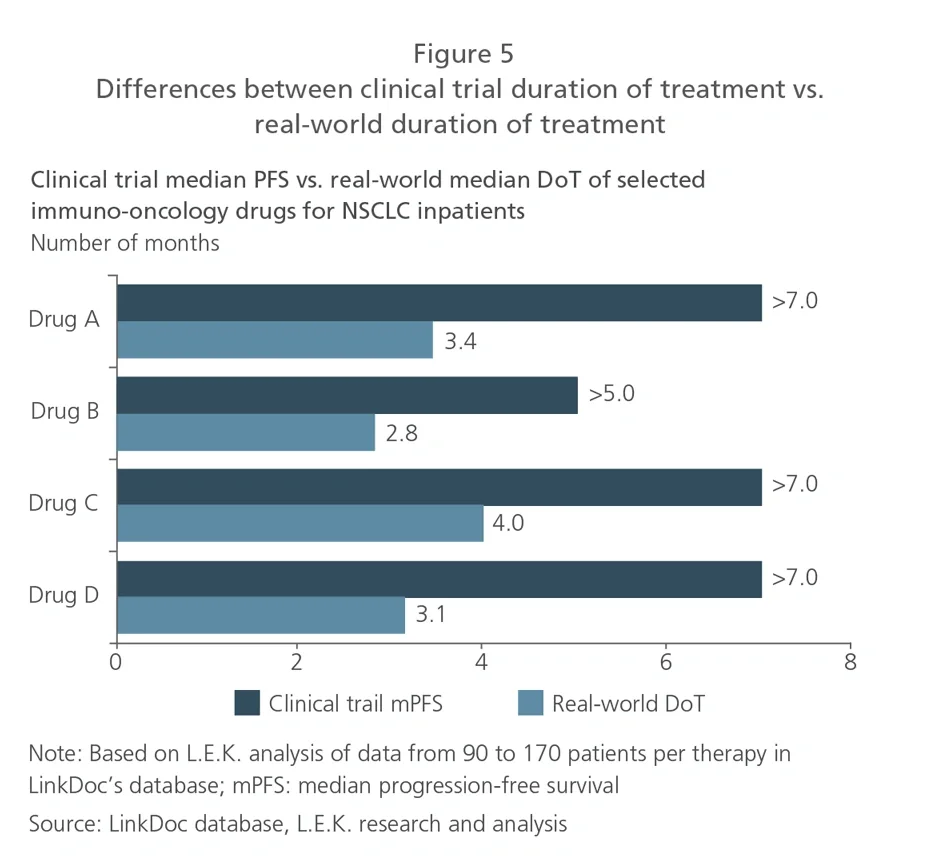

To drive better market access for patients, pharma companies often need to pursue reimbursement. Therefore, it is key to develop evidence that will support pricing through reimbursement negotiations, and ensure that the severe price cuts needed to enter the NRDL do indeed result in major volume upticks following listing to maximize revenue in the long run. For pharma companies participating in the Q4 2020 NRDL negotiations, RWD will also facilitate quick preparation for upcoming discussions.

Using RWD to optimize pricing strategy

To formulate their pricing strategy, pharma companies should account for several key considerations. Each product’s unique value proposition will influence the pricing and premium it could command in the market. Pharma companies are operating in increasingly competitive indications with an increasing number of therapeutic options available. Needless to say, having a good understanding of competitors' pricing strategies and market switching dynamics both at launch and through the life cycle as other competing products enter the market remain critical.

Pharma companies are under ever greater pressure to optimize returns, for which they need a complete understanding of volumes, revenue and profitability under a range of different price scenarios and strategies. RWD is fast developing as an additional source that can complement pharma’s internal and traditional datasets to assess potential outcomes under different market access strategies. There is an increased volume and variety of RWD in China, as China made healthcare big data a national priority in 2018, encouraging healthcare institutions to share and exchange big data.3

These policies enabling and encouraging use of RWD will continue to drive increased use and generation of data pools that pharma companies can use to improve a wide variety of business intelligence and planning processes. These include estimating their addressable patient base, adoption, patient volumes before and after reimbursement, and revenue per patient. These better estimations can then flow through into more confident and realistic resource allocations, market access and pricing strategies.

Assessing market potential

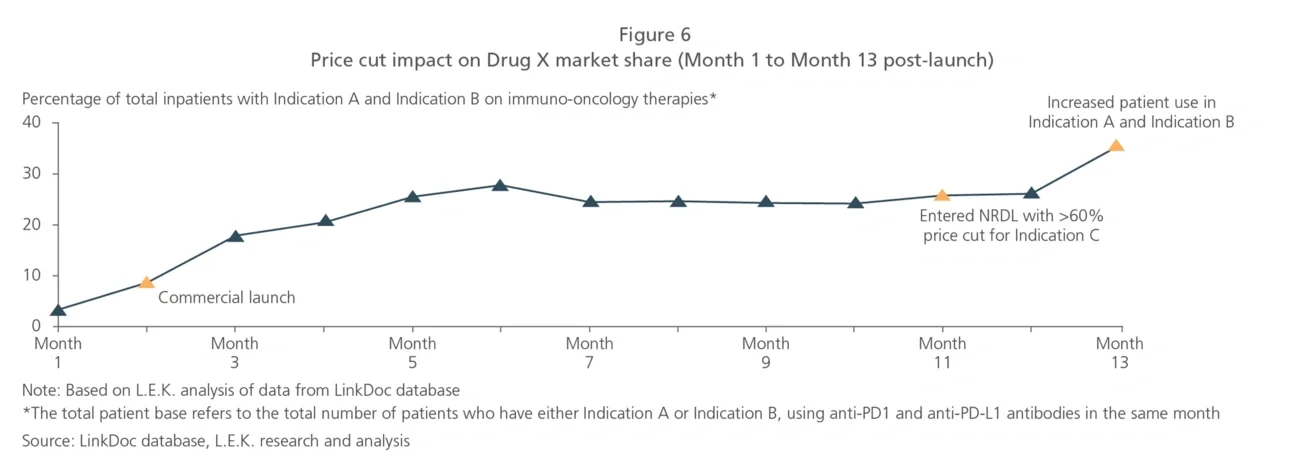

Using RWD, companies can develop a more precise view on the price-adoption relationship to decide on acceptable ranges for launch price and/or reimbursement price, as well as how hard they should be pursuing national reimbursement. Since reimbursement negotiations are now taking place shortly after drug approval (just a matter of weeks for some oncology therapeutics launched during 2020), pharma companies need to use up-to-the-moment RWD from their own products as well as reference drugs (for example, those in the same drug class) in the market.

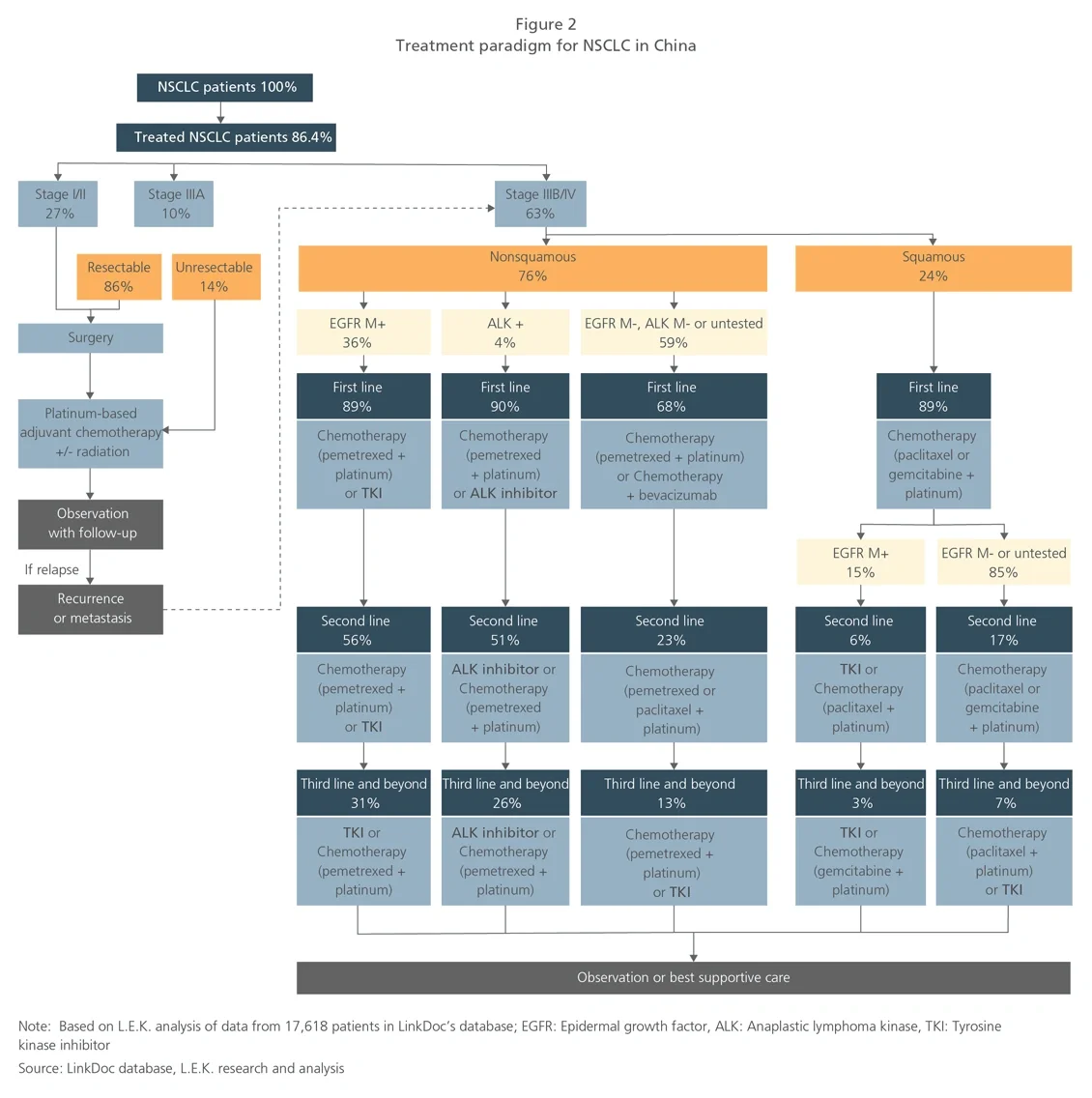

To assess the potential patient volume captured, pharma companies need to determine the addressable patient base. RWD exists in abundance for this analysis, including patient segmentation by disease stage, diagnostic testing rate, treatment rate and line of treatment. This will support precise quantification of the target patient base. For example, based on L.E.K. analysis of a sample in 2019 of over 17,000 NSCLC patients, 48% of all treated patients are nonsquamous, and 31% of epidermal growth factor receptor (EGFR) mutation-positive nonsquamous patients will progress to third-line treatment (see Figure 2).