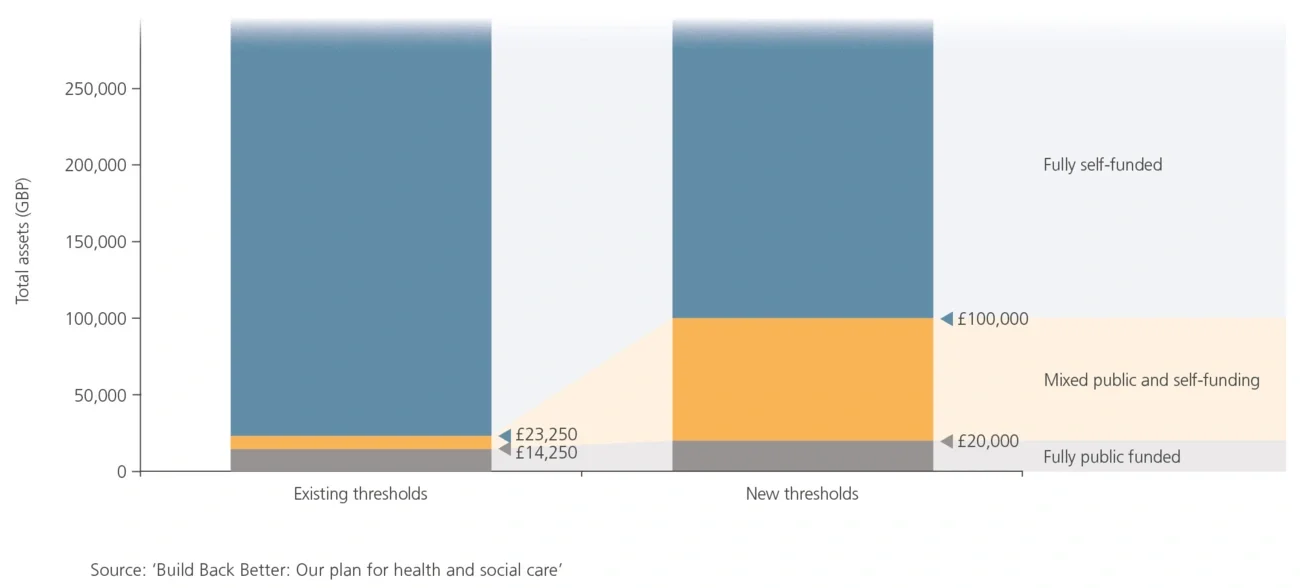

On 7th Sept., the Government published ‘Build Back Better: Our plan for health and social care’ (the Plan), outlining its intentions to introduce a cap on lifetime care costs and to increase the means-testing thresholds. A new national health and social care levy will fund these initiatives, along with other proposals in the Plan, e.g., tackling the NHS backlogs and improving the integration of health and social care. The Government published further details on 19th Nov. about the standard daily living costs and exclusion of means-tested council support from the cap. The House of Commons endorsed this on 23rd Nov., despite opposition from Labour and some Conservative MPs.

Whilst the concept of a care cap and an expansion of the means-testing criteria can look ‘seismic’ for most of the public, the initiatives will sound very familiar to seasoned market participants and observers, as they had been the centrepiece of the Dilnot funding reform, scheduled for implementation in April 2016 but postponed before its roll-out.

In this Executive Insights, L.E.K. Consulting will evaluate some of potential impact of the Plan on the social care sector, instead of repeating too many comments and speculations with regard to funding and how much money might actually end up being directed towards social care. We will especially consider the two main changes:

- The introduction of a lifetime care cap of £86,000, which is intended to limit the total amount self-funders need to contribute towards their personal care (it is important to note that it excludes accommodation and general living costs)

- Raising the means-testing threshold from £23,250 to £100,000, making more elderly consumers eligible for either partial or full public funding