Summary

Six Minutes With…

Wiley Bell, Managing Director in L.E.K. Consulting’s Healthcare Services Practices

Wiley Bell, a managing director in L.E.K. Consulting’s New York office, has built a career as an advisor to both fast-moving consumer goods companies and healthcare firms, and is currently working to help managed care organizations (MCOs) on key topics around healthcare cost. In a recent interview, he spoke about how the U.S. healthcare system is changing and how MCOs can help improve outcomes and control costs.

Why does the U.S. pay more for healthcare than the rest of the world?

Healthcare is nearly twice as expensive per person in the United States relative to other wealthy nations and our outcomes aren’t any better. The basic reason is that our system is set up in a way that conceals costs. Healthcare is a consumer product that the consumer doesn’t pay for directly. The complexity of the system keeps supply and demand from meeting directly to produce rational prices. Consumers have become passive. Americans pay for healthcare through taxes and payroll deductions, but we don’t see the real cost so have no reason to complain about, say, $4,000 for an MRI. Meanwhile employers think of healthcare as a recruiting tool or perk to be managed by their HR departments, not as a cost they should try to control.

How do you mobilize employees and convince them to shop around?

They’re starting to feel sticker shock. Recent polls say that nearly 80% of Americans now think that the cost of care is the most important issue facing the U.S. healthcare system. The threat of being channeled into the exchanges has helped bring the real cost of healthcare into the living rooms and kitchens of America. Just to put our costs into some perspective, a hip replacement here costs about $40,000. In Spain the same procedure is $8,000. A colonoscopy costs $1,200 in the U.S. and $655 in Switzerland. An MRI costs $1,100 in the U.S. and $320 in the Netherlands. These aren’t cherry-picked outliers.

Consumers can’t bring price sensitivity to healthcare by themselves, however. Employers and managed care partners are going to have to help. Employers who simply put employees on their own to start the crusade for reasonable prices are sending their workers unarmed into an established medical environment that has been very good at protecting its high pricing.

What can employers do to help their employees bring competition to the market?

Employers don’t buy healthcare directly either. They go through managed care organizations. MCOs negotiate contracts with providers, design plans, and monitor usage. This collaboration has not worked – not for cost control. There has been some movement recently, with leaner plans and the threat of being sent to exchanges. But it’s not enough.

This has been going on for a long time. Remember the HMO? This was an early response to out-of-control costs. By 1999 there were 80 million HMO members. We finally had control over costs, but when employees predictably complained about reduced choice, employers panicked. Instead of trying to fix the system, they abandoned it and fee-for-service preferred provider organizations (PPOs) took root. A president of a major hospital system told me, “Employers wimped out. They were spineless.” She’s right. This time around employers must remain committed and they must help empower their employees. Communication, as always, will be critical.

What have MCOs been doing to help?

MCOs have not lacked initiatives. They have continued efforts to promote health and wellness, experimented with exchanges, and negotiated narrower provider networks. Also, they have invested in image advertising to confront the perception that they don’t add much value. They have been moving toward a more consumer-centric approach and some have even gotten into retail sales (e.g. United Healthcare sells plans at Costco). They’ve invested tens of billions of dollars in providers, which gives them more direct insight into the supply side. They have invested in accountable care organizations (ACOs) to get providers to share the risk. And MCOs spend close to $10 billion every year on care management, which is primarily an effort to make sure that doctors adhere to the established protocols.

In short, the healthcare insurance industry has been very busy. But it isn’t working. The recent efforts by MCOs may bear fruit eventually, but for the foreseeable future they won’t make much of a dent in a system that is already $1.4 trillion too expensive.

So what should MCOs be doing?

I think MCOs need to make a public cause out of quality, low-cost healthcare. The largest MCOs have made proclamations about how much of their spending will be in some form of risk sharing with providers. But nobody has publically set a bold challenge, saying “We will be the Walmart of healthcare.”

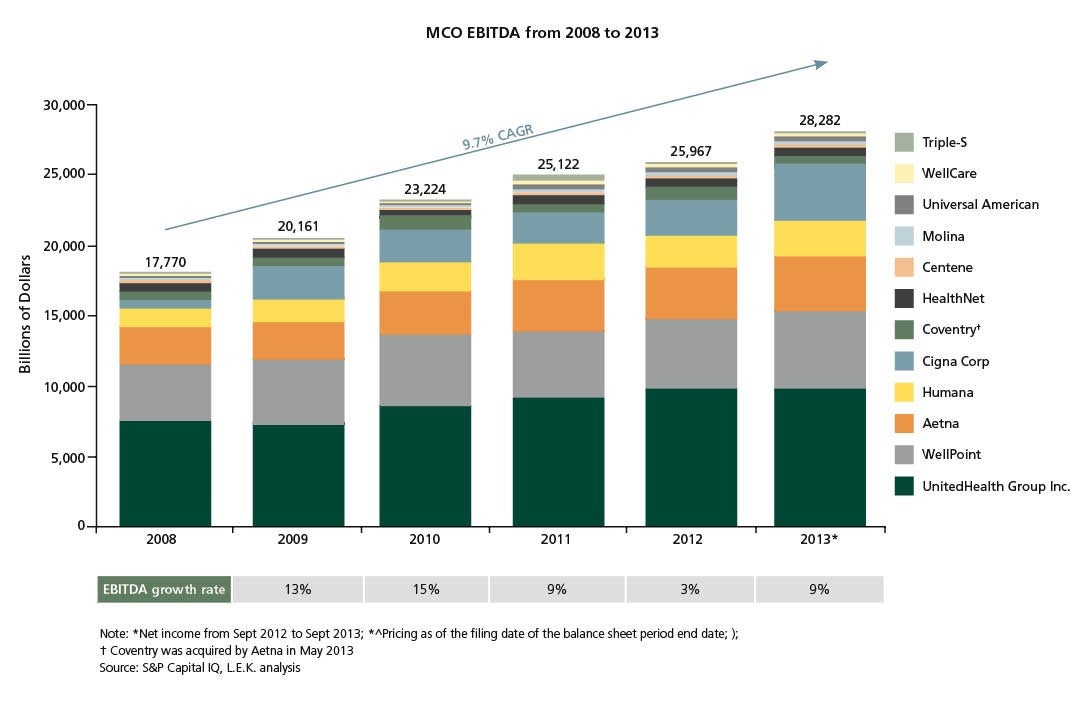

There is ample reason why MCOs have hesitated to initiate an all-out assault on healthcare cost. First, profit growth for publicly traded MCOs has been strong (see Figure 1). Second, payers across the board have shifted their attention to the growing pool of potential government members, often placing their commercial book on the back burner. Third, there remains significant uncertainty around key areas such as how many employers will push their employees onto the exchanges. Finally, MCOs have been complicit in the high prices charged by providers, many prospering on the back of a cost-plus environment.

As in the past, the high-priced providers that often form the backbone of any given network will not take price reductions without a fight. L.E.K. has done an analysis of which local markets are most likely to spawn risk-taking providers. There aren’t many.

How can MCOs change this imbalance?

It starts with branding. I believe MCOs have a compelling story to tell. The MCO is best-positioned to be the ultimate advocate for the employer and ultimately the consumer. They should be viewed like the general contractor when it comes time to build your home – as a knowledgeable mediator who can manage for outcomes and cost on your behalf. This is not their current image.

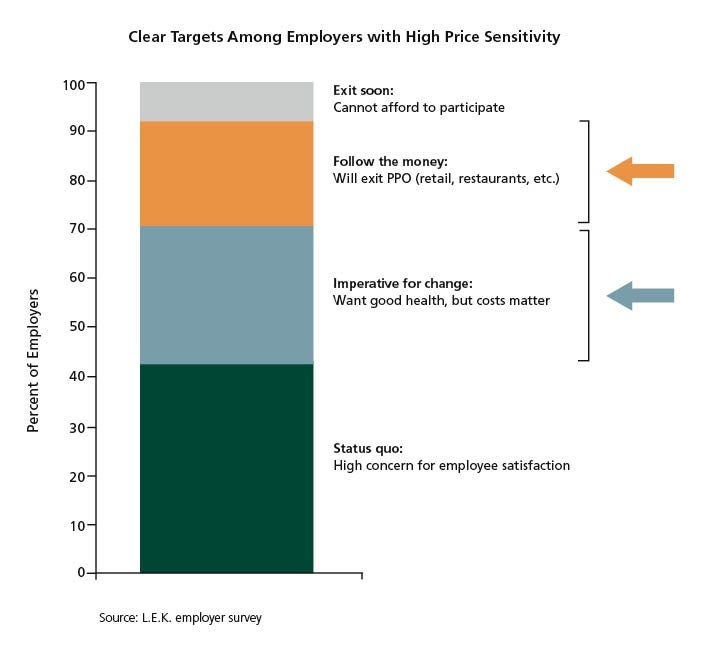

For consumer companies, segmentation and marketing is the art and the science of the business – consumer insight is what separates good companies from great companies. An MCO needs a more actionable segmentation of employers, and the associated pool of 150 million members (that is, the employees). Roughly speaking, companies representing approximately 10% of these employees can be categorized as “cannot afford healthcare.” This segment will push their employees onto the exchanges. At the other end of the spectrum, about 40% of employees work for companies that will continue to absorb the high cost of healthcare since competition for their employees demands they don’t take a risk on this front. The remaining 40% (the “messy middle”) are very much up for grabs for a low cost product (see Figure 2).

With employer segmentation in hand, MCOs need to connect with the employee. The instinctive reaction of the employee will be that something is being taken away – easy access and low out-of-pocket costs – with no quid pro quo. The emphasis to date has been on creating incentives for the provider in risk-bearing relationships. There needs to be at least the same effort targeted at the consumer (that is, the member). Historically, the incentive has been around better health behaviors. There need to be incentives for choosing low-cost plans and low-cost options.

What does the future hold for MCOs?

If employers actually take control of purchasing themselves – through co-ops or alternative supply relationships – MCOs are going to become what some business people already think they are: unnecessary overhead. MCOs need not let this happen – employers currently don’t have the power to control costs on their own. For the time being they need MCOs for MCOs' scale and bargaining power – but they need effective MCOs.

If they fall short, other players may step into the vacuum, for instance companies such as CVS Caremark, whose CEO has hailed a “rise of consumerism” in healthcare. On a strategic level, MCOs need to rethink their commitment to making employer-sponsored healthcare not just a little less bad, but truly competitive on the world market. American healthcare would lose if it were an international business. Unfortunately, we cannot buy healthcare from more efficient countries. It is a local business by nature.

MCOs were invented to aggregate and negotiate for employers. For the time being, employers need MCOs for this reason. But they need effective MCOs. There’s the rub.

Sample Visuals

02282025100226