Key takeaways

-

To be successful in the next decade, healthcare product and service suppliers need a more comprehensive understanding of their customers.

-

They must also adapt their commercial engagement models and offerings to the varying needs of provider segments.

-

L.E.K. Consulting has developed the Provider Pulse — an analytical tool delivering a robust, data-driven segmentation that reflects both behavioral and performance differences among providers.

-

In this Executive Insights, we explore the differences between these segments and the implications for suppliers as the healthcare landscape continues to evolve.

U.S. healthcare providers are evolving, and their suppliers must evolve with them. The provider landscape continues to be reshaped by economic pressures and technology developments. Simultaneously, the market ecosystem is becoming more crowded as nontraditional participants (e.g., Amazon, Apple) seek to take advantage of opportunities in healthcare. To be successful in the next decade, healthcare product and service suppliers need a more comprehensive understanding of their customers than they had in the past and must adapt their commercial engagement models and offerings to the varying needs of provider segments.

Empirical data shows that hospitals/health systems are increasingly stratifying into different segments based on “progressiveness” and scale. More progressive providers are proactively increasing their exposure to value-based payments and integrating more closely with nonacute care. Progressives tend to be much more interested in partnering with their suppliers to address broader needs, while nonprogressive providers are more transactional in their approach. Scale dictates the complexity and sophistication of supply chain needs with which suppliers must contend. Importantly, the provider landscape continues to consolidate and not all health systems are thriving. It is the larger, “scaled” progressive health systems that tend to be thriving and taking share in the market. These ~100 organizations control ~45% of total acute care spending, and their share continues to grow.

The new normal for healthcare suppliers

The structural and strategic transformation of U.S. healthcare providers continues apace, and is creating a new landscape populated by a very different set of provider customers for healthcare product and service suppliers to address. This evolution in the structure of the provider landscape is primarily a product of two forces:

- Policymakers, payers and employers are seeking to reduce growth in healthcare spending as the cost burden on society expands due to the aging of the baby boomer generation and unsustainable spending levels (largely driven by historically unconstrained fee-for-service (FFS) payment models)

- Developments in technology are creating disruptive opportunities for enhancing quality and efficiency of care provision as well as altering patient expectations

These forces are driving an unprecedented wave of innovation and interest from many nontraditional participants in the healthcare market (e.g., Amazon, Apple, IBM, Alphabet). They are also disrupting decades-old business models for healthcare product and service suppliers, creating both new challenges and new opportunities. As the U.S. provider landscape evolves, suppliers face:

- Higher sales concentration in fewer, larger customer accounts

- More sophisticated healthcare provider customers with more complex needs

- More centralized customer decision-making with greater influence from administrators

- Greater customer focus on value with a higher bar for clinical differentiation

- New competition and an increasingly crowded healthcare ecosystem

Suppliers must adapt what they offer and how they engage with their customers in order to thrive in this environment.

Segmenting for success with the Provider Pulse

The changes in U.S. healthcare delivery are most evident in the evolution of acute care. Acute care providers are responding in a variety of ways to the macro pressures they’re facing. Some are wholeheartedly embracing the shift to value-based care. Some are aggressively pursuing greater scale. Some are trying to do both. And others are just trying to do what they can to survive. The result is that hospitals and health systems are increasingly stratifying into behavioral segments with distinct needs and priorities. Inherently, these segments also have different preferences and expectations for how they interact with their suppliers and other external partners.

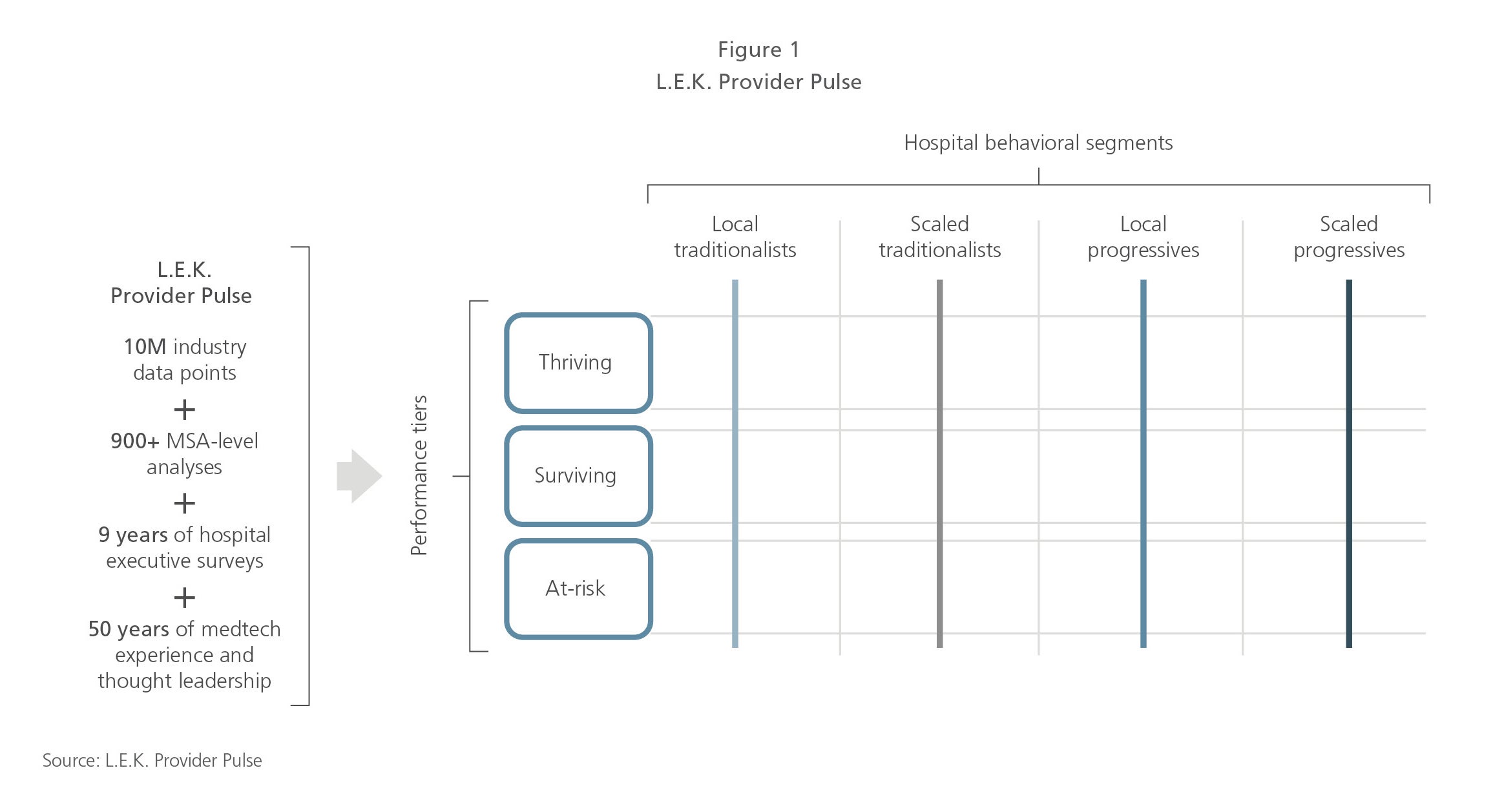

A decade of tracking the evolution of the healthcare landscape has led L.E.K. Consulting to develop the Provider Pulse (Figure 1) — an analytical tool delivering a robust, data-driven segmentation that reflects both behavioral and performance differences among providers. Health systems and hospitals are scored on two behavioral dimensions — progressiveness and scale — to determine in which behavioral segment they belong. These providers are also evaluated on a range of performance metrics at the local market level (i.e., growth, market share, financial stability) and accorded a performance tier (i.e., Thriving, Surviving, At-risk).

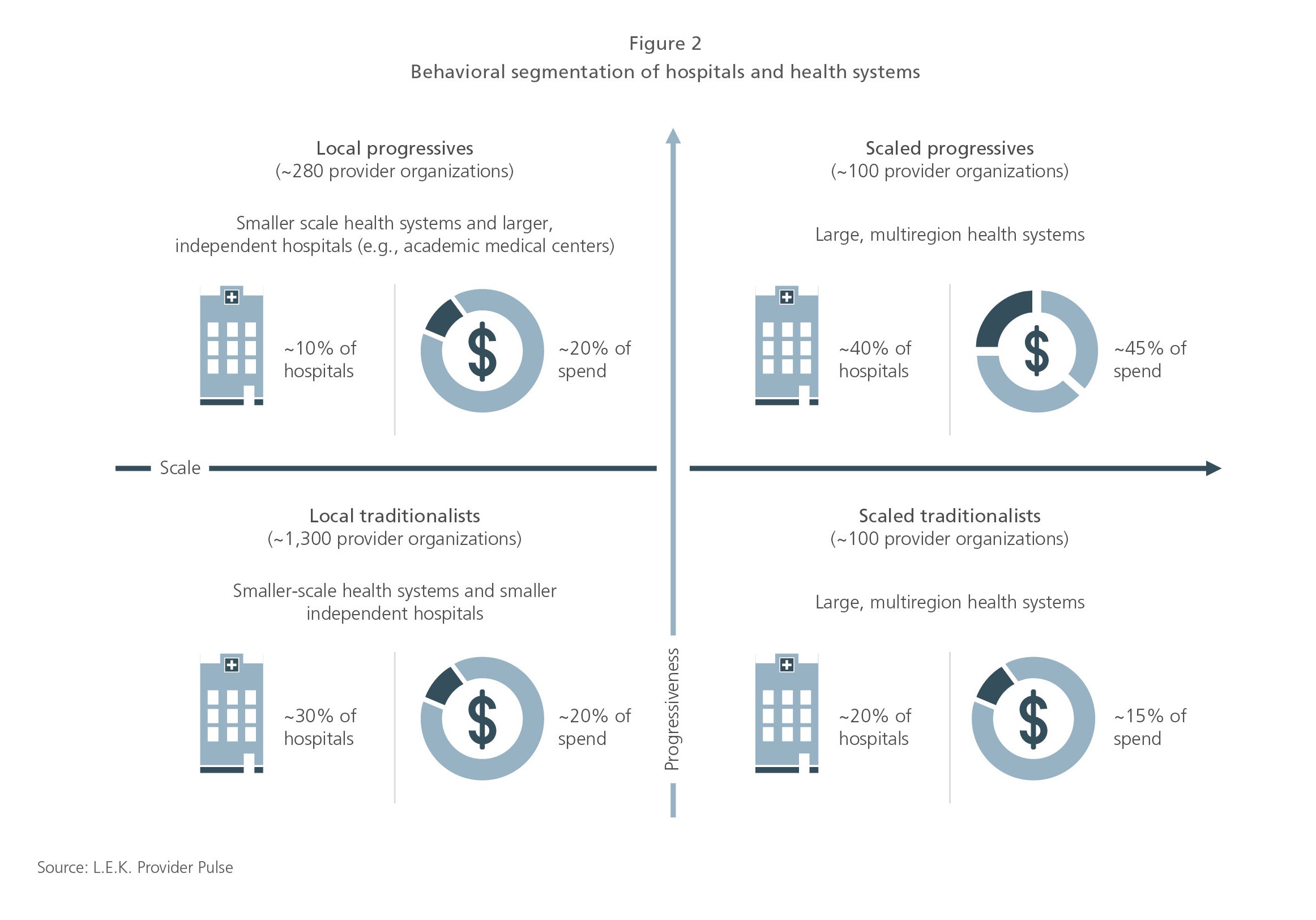

Progressiveness is a function of provider accountability (i.e., participation in value-based payment models/financial risk associated with clinical outcomes) and integration (i.e., degree of ownership and/or affiliation with nonacute sites of care). More progressive providers tend to be more likely to self-select into and have greater revenue exposure to value-based payment models. They also tend to integrate more closely with nonacute care sites. Conversely, less progressive providers have lower exposure to value-based payments and tend to engage in these models only when they are required to do so (e.g., mandatory Centers for Medicare & Medicaid Services (CMS) programs such as Comprehensive Care for Joint Replacement (CJR)). They are also less likely to own or affiliate with a broad set of nonacute sites. Importantly, progressiveness correlates with the extent to which providers prefer more partnership-oriented supplier relationships (versus more transactional relationships).

Scale is a function of a provider’s geographic reach and the number of acute care facilities it owns, and reflects ongoing consolidation of acute care. Larger, more scaled health systems tend to have greater supply chain sophistication, and the administration tends to exert more influence in these organizations. Scale tends to be an indicator of the complexity of a provider’s supply chain needs as well as the level of negotiating leverage and contracting complexity with which suppliers must contend.

The intersection of these dimensions — progressiveness and scale — creates the basis of an effective behavioral segmentation of hospitals and health systems (see Figure 2).

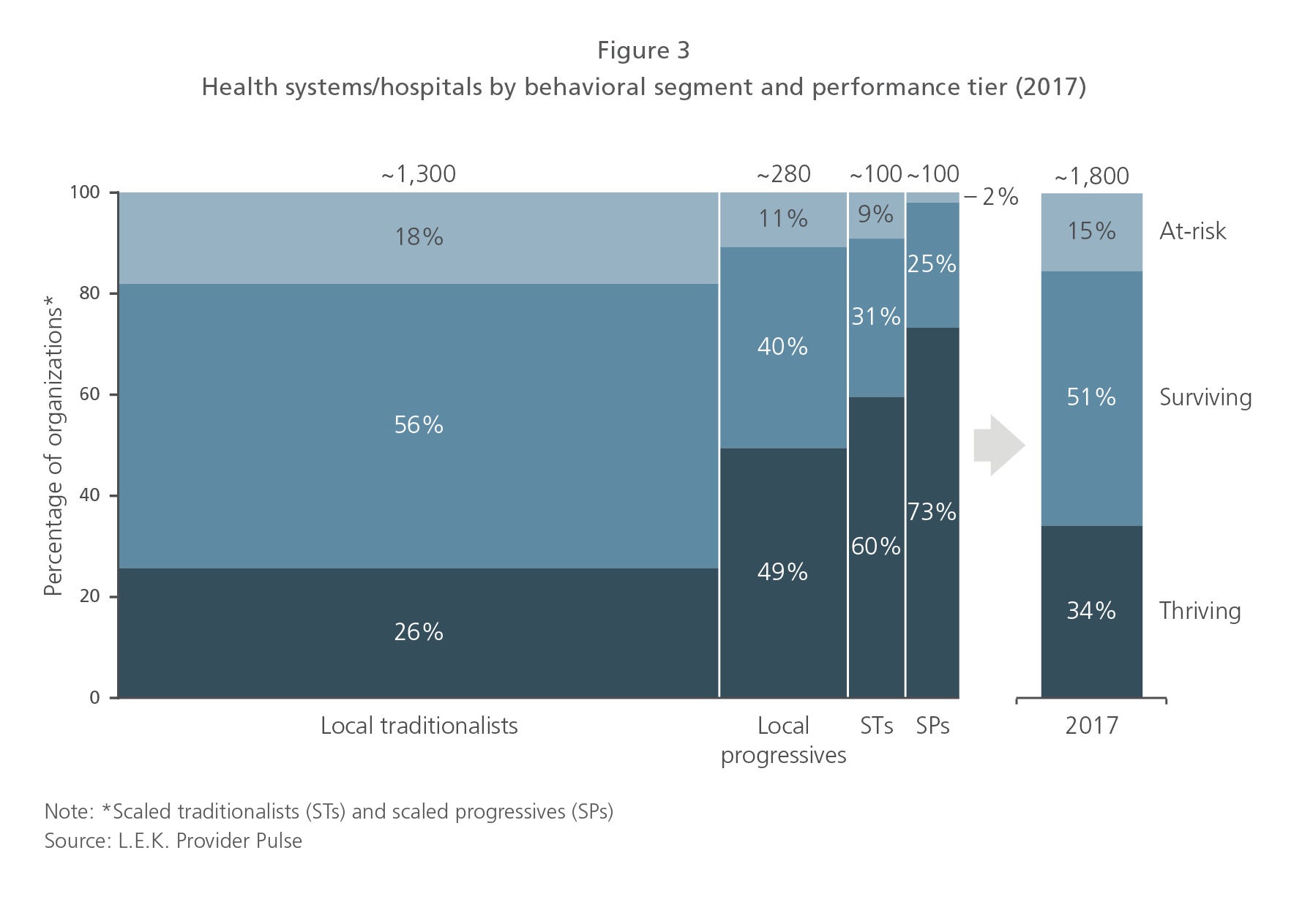

All in all, while there are only ~100 scaled progressive organizations (~5% of total), they account for a highly disproportionate share of hospitals and spending. Furthermore, these organizations are much more likely to be thriving and are continuing to take share in the market (see Figure 3).

This segmentation is particularly important for healthcare product and service suppliers for two reasons:

- Some segments are growing while others are shrinking

- Strategies for success can be substantially different between segments

Consequently, it has become imperative for suppliers to understand their customers more thoroughly than ever before. The following sections explore the differences between these segments and the implications for suppliers.

Accountability: The train has left the station

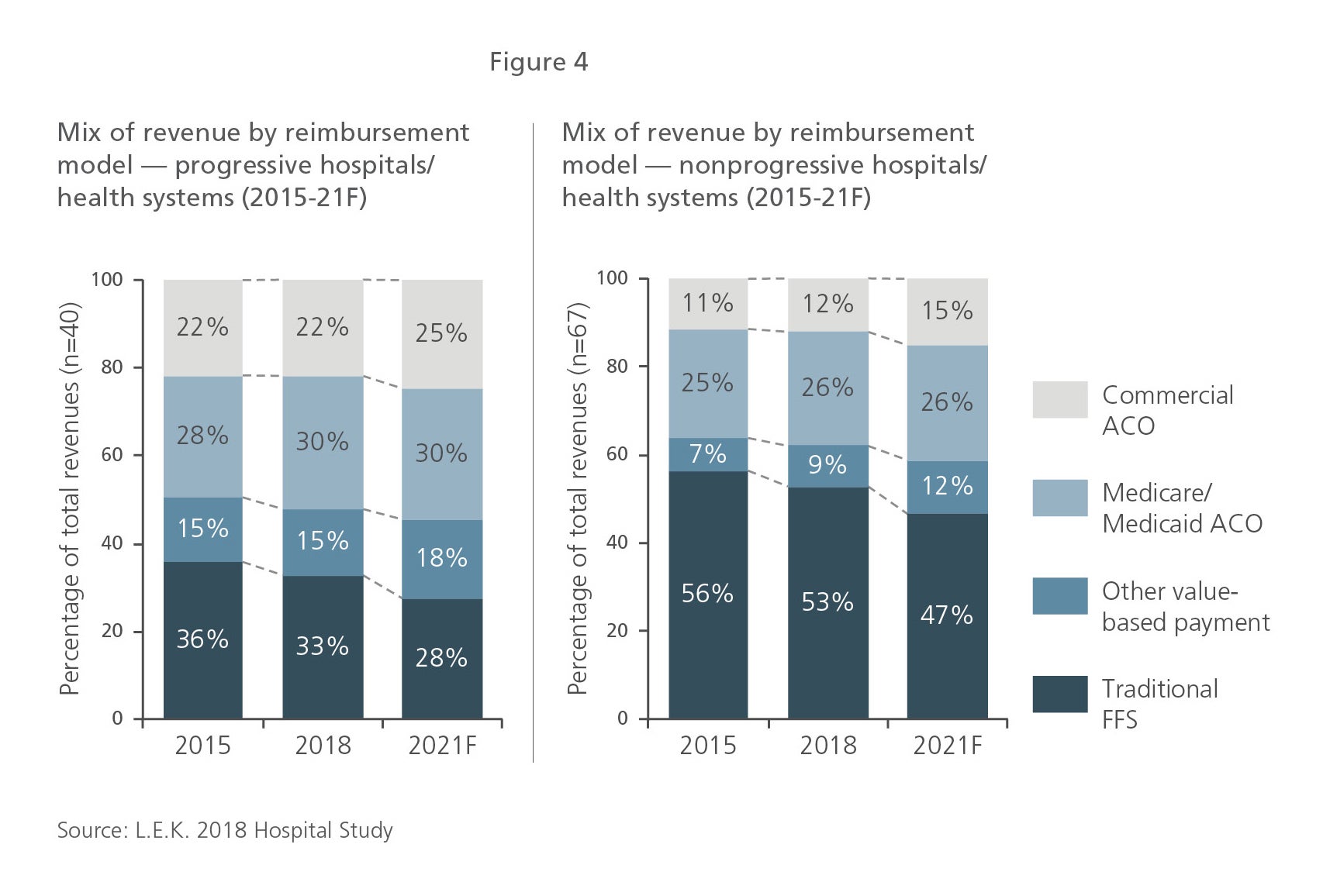

Since the Patient Protection and Affordable Care Act was passed in 2010, U.S. reimbursement has increasingly shifted from a focus on fee-for-service payments to alternative payment models encouraging or requiring providers to accept greater financial accountability for clinical outcomes. CMS, which accounts for ~40% of U.S. healthcare spend, has led this shift, and commercial payers have followed suit. In fact, CMS and commercial payers have made significant and relatively rapid strides in recent years to shift risk to providers with a range of value-based models. The L.E.K. Consulting 2018 Hospital Study (including a survey of ~170 hospital executives) reflects this trend, as depicted in Figure 4, highlighting how hospitals themselves, including both progressives and nonprogressives, are moving away from FFS payment models toward value-based payment models.

Although CMS’ focus on innovating and rolling out value-based payment models has slowed under the Trump administration (e.g., paused expansion of CJR), the market shift has continued. Commercial payers have continued to move away from traditional FFS contracts, and employers have continued to contract directly with providers for selected episodes of care (e.g., total knee replacement, spine fusion). There has been a mental and cultural shift in the healthcare system toward value-based care — leaders recognize that this is the future of the industry.

Importantly, the impact of greater accountability on acute care providers is palpable. All providers have had to participate in CMS’ mandatory programs (e.g., the Hospital Readmissions Reduction Program, which penalizes hospitals for a range of unnecessary hospital readmissions). While all acute care providers have had to navigate the challenges and opportunities of some mandatory programs, some have proactively sought accountability — participating in accountable care organizations (ACOs) and CMS’ Bundled Payments for Care Improvement initiative, securing at-risk contracts with commercial payers, directly contracting with employers, developing their own health plans, and, in general, investing in resources (e.g., post-acute care coordinators) and infrastructure (e.g., IT capabilities) to enable greater accountability. While a minority of the most progressive health systems have “jumped into the deep end” (and some, like Kaiser and Geisinger, were already there), most progressives have at least been moving toward value-based care with significant experimentation and an overall “dip the toe” approach. Local and scaled traditionalists have largely shied away from taking on any more accountability than required by payers.

For suppliers, the implications of increasing provider accountability are not always obvious. Some suppliers have responded directly with new offerings (e.g., digital health apps to support patients during bundled care episodes such as knee replacement); however, most supplier efforts to make their offerings relevant to the accountability goals of their customers have gained relatively little traction. While the value of linking and ability to link supplier products and services directly to accountability are still uncertain, this underlying theme will likely remain important for customers, especially progressives, going forward.

Integration: Blurring the lines between acute and nonacute care

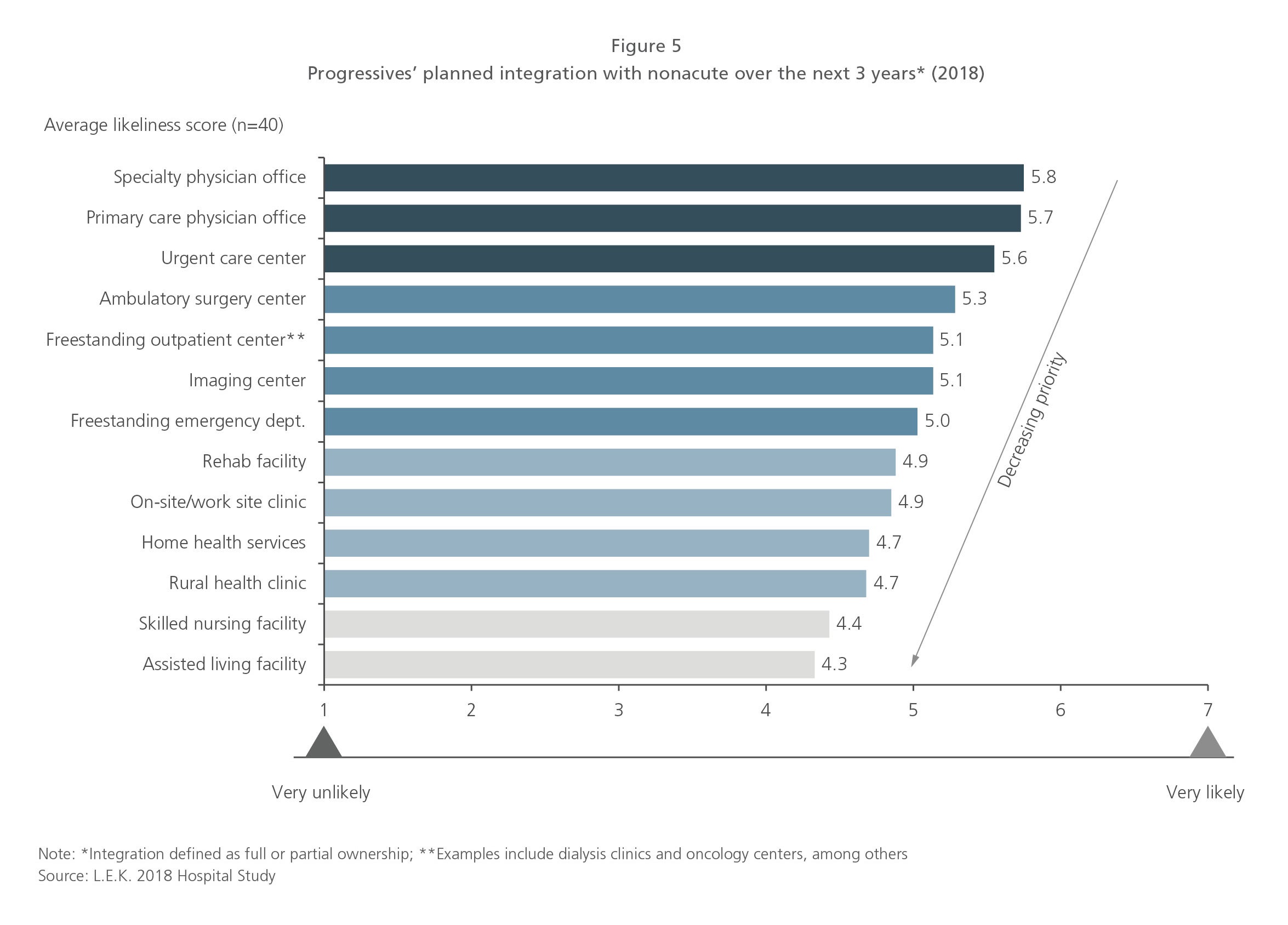

Health systems — scaled progressives in particular — are making significant investments in acquiring or building nonacute care sites. This is driven primarily by local competition for patients (e.g., expanding catchment areas, especially in areas with a favorable payer mix), along with these health systems’ commitment to greater accountability (i.e., control of risk across the care continuum, access to lower-cost settings). Physician offices, urgent care centers, ambulatory surgical centers and other outpatient facilities have been the focus of integration for progressives (see Figure 5) due to the patient referrals and downstream revenues they generate.

Other sites of care such as long-term care facilities are also being integrated, but more commonly through coordination mechanisms rather than ownership. The economics of some of these care sites are less attractive, and health systems are able to effectively identify the right facilities with which to partner via internal resources or external conveners (e.g., naviHealth, Remedy Partners). Whether through vertical integration or coordination, progressive health systems are expected to continue to integrate and to shift a greater proportion of their care into nonacute settings. In addition, this integration is expected to deepen over time. While the only impact of integration for some nonacute sites to date has been a change in signage or access to a group purchasing organization (GPO), progressive health systems are generally seeking to unify IT systems and drive increased coordination with their nonacute sites over time (e.g., standardization of supply and drug purchasing, clinical protocols).

For suppliers, this convergence of acute and nonacute customers is creating both new opportunities and new challenges. Suppliers have the potential (at least in time) to more easily access nonacute customers, who have historically been more difficult and costly to service. On the other hand, suppliers are exposed to greater pricing pressures as health systems harmonize prices across sites, face operational challenges in servicing a broader range of site types with different needs, and are potentially open to competition from other settings. Net net, integration likely presents more opportunities than challenges for suppliers, but its importance varies by provider segment. Suppliers need to be attuned to customers’ nonacute strategies and navigate customer-specific needs thoughtfully.

Consolidation: Scale begets scale

The most obvious trend in the evolution of the acute care provider landscape is consolidation. Health systems are becoming larger in scale, and independent hospitals are becoming fewer in number. U.S. hospital consolidation continues, driven by pressure on reimbursement, competition and a “race to scale” in local markets.

Hospital margins remain uninspiring, hovering near or slightly below 0% for most providers. Scale is one of many factors impacting an acute care provider’s financial performance. Generally speaking, health systems tend to have higher margins than do independent hospitals. While small changes in reimbursement from CMS (e.g., performance penalties) may appear to have only a modest impact on net patient revenue, this can be the difference between a positive and a negative margin for the year.

Furthermore, share within a local healthcare market enables providers to improve their bargaining power vis-à-vis payers and to drive economies of scale (e.g., acquire patient referrals, attract and retain physician talent, enhance returns on marketing investments). Growing local market share also inadvertently creates a race to scale. As hospitals consolidate, they induce other players in the local market to follow suit in order to remain competitive. It is easy to see how smaller acute care providers struggle to compete for patients, given their lack of funds to invest in new facilities, new equipment, physician talent and even the IT infrastructure needed to meet increasingly onerous compliance requirements.

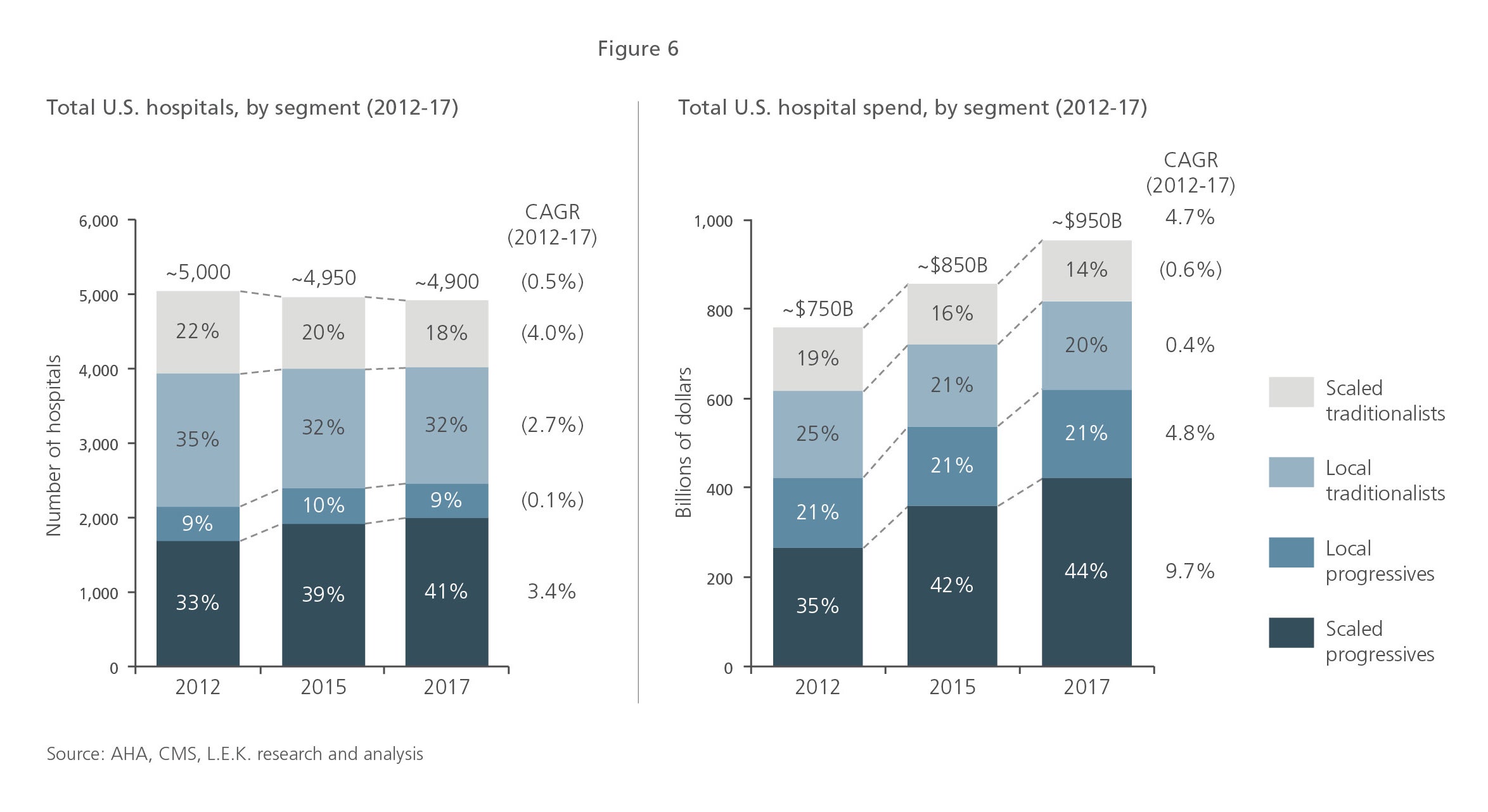

Hospital consolidation has been ongoing over the past five to 10 years. Scaled progressive systems are the driving force behind consolidation and are capturing a growing share of acute care spending (see Figure 6).

While hospital consolidation is expected to continue, it is likely to be somewhat more gradual over the next five years than in the previous five years. A shrinking pool of attractive acquisition targets, antitrust scrutiny, the need to integrate existing acquisitions, examples of consolidation gone awry and diminishing returns on scale may limit and/or slow future consolidation.

Nonetheless, the number of unique acute care provider organizations will be fewer in five years, and the progressives will continue to grow their share of spending (whether through acquisition or the gradual evolution of nonprogressives into progressives). Effectively targeting and developing compelling offerings for these progressives is paramount to the long-term success of healthcare suppliers.

Segmentation implications on supplier relationships

As acute care providers are changing in size and scope, their supply chain activities and relationships with suppliers are also changing. While these changes are most evident for more progressive health systems, all hospitals have experienced some level of change. Understanding these dynamics is critical for the continued market success of healthcare suppliers.

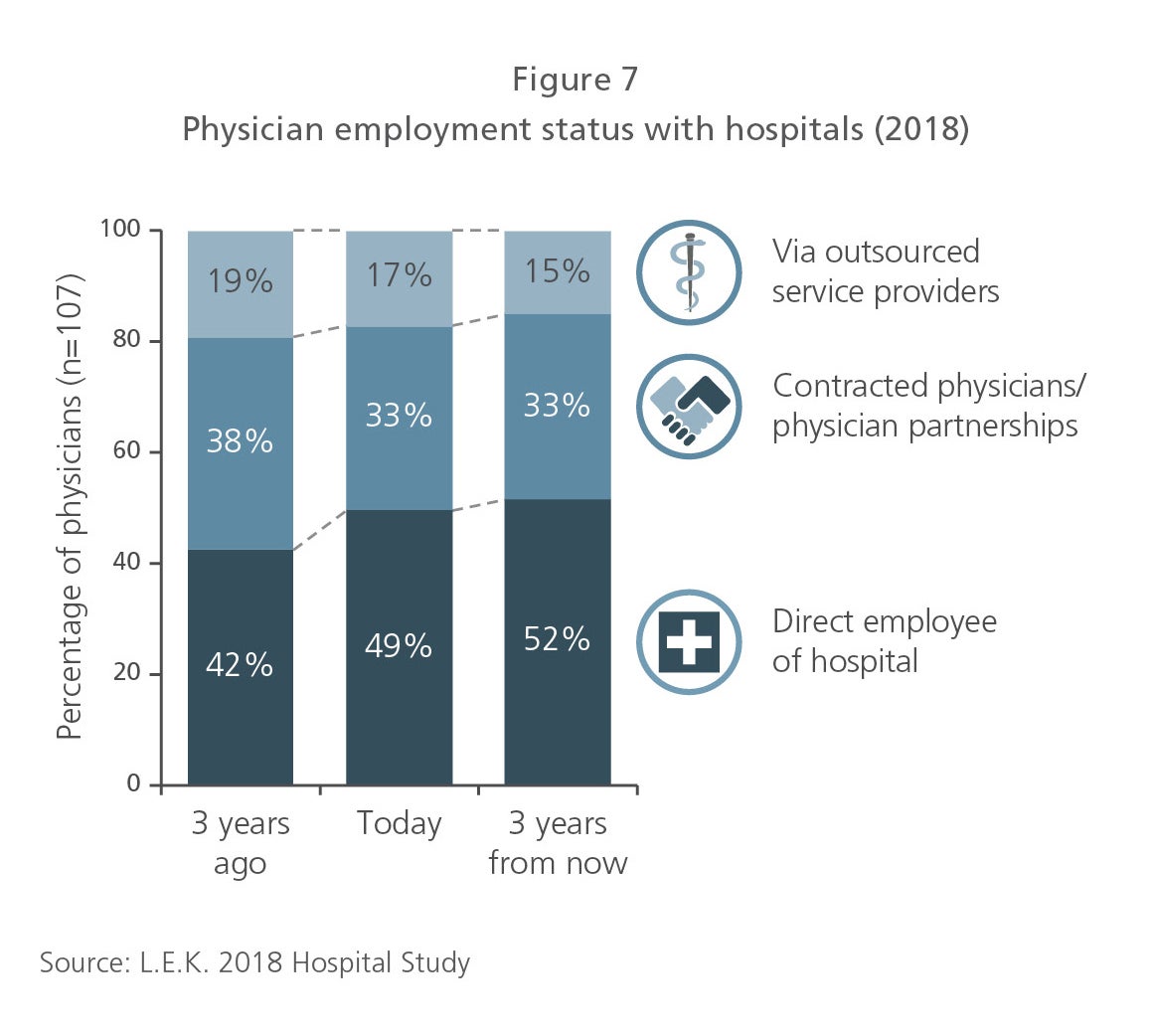

All providers face some level of economic pressure from reimbursement and competition that has elevated cost-saving goals. While this is more dramatic for some (e.g., local traditionalists) than others (e.g., local progressive academic medical centers), it is hard to find a hospital in the U.S. that has not undergone a cost-cutting initiative in the past several years. To drive these cost savings, most providers are increasingly centralizing their purchasing decisions and trying to standardize the products and services they buy. For a wide range of products and services, decision-making has continued to shift away from clinicians to administrators. While administrators have long held sway with respect to more commodity items, they are increasingly having greater say over physician preference items as well. Clinicians still retain strong influence over some product categories and are certainly represented on the value analysis committees employed by most providers, but the impact of physician influence is substantially diminished in many categories and in many provider organizations. This has been enabled, in part, by increasing hospital employment of physicians (see Figure 7), which inherently gives the administration more influence and helps it drive standardization initiatives.

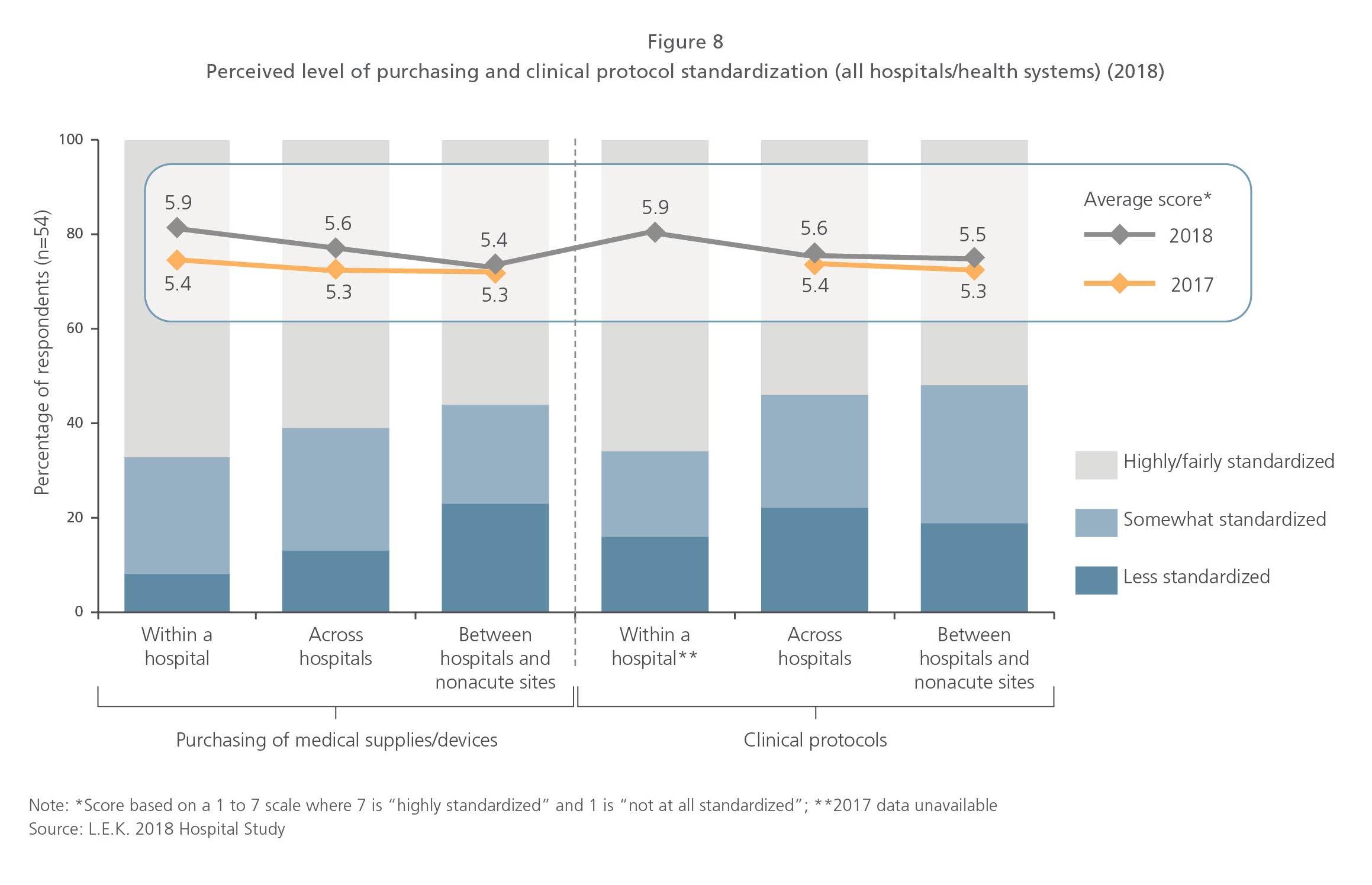

In line with this shift in decision-making is a strong interest in standardization (see Figure 8) — not only of products, but also of processes and protocols. While the primary goal of standardization tends to be cost savings, secondary goals include improved efficiency and consistency in training staff and reduced variability in procedures, which helps control outcome variability in a value-based care environment. As providers seek to standardize, they often attempt to rationalize their supplier base and try to offer suppliers a higher share of business in exchange for lower pricing. Notably, provider organizations differ substantially in their ability to drive actual compliance with standardization targets, which limits the effectiveness of these tactics today. Nonetheless, providers are expected to be able to improve their ability to drive standardization/compliance, which will give an advantage to suppliers with broader portfolios and more compelling bundles going forward. Smaller suppliers can certainly compete successfully, but the playing field for winning based on differentiated offerings is narrowing. While success in driving standardization varies across provider organizations, efforts in this direction are expected to continue.

Centralization of decision-making, standardization and supplier rationalization are themes evident to different degrees among all providers, but most particularly among progressive health systems. Progressives have been the most aggressive in tightening control over decision-making within their systems and have been the most sophisticated in driving standardization and rationalization initiatives. This is a reflection of progressives’ generally higher engagement in the operations of their supply chains. Scaled progressives, in particular, have brought in supply chain talent from outside healthcare and have sought to take control of their supply chains to reduce variability and costs throughout their systems. These efforts have manifested themselves in many ways, including self-distribution of products, establishment of consolidated services centers, and less reliance on national GPOs via regional purchasing groups or direct integration (e.g., Mercy Health’s ROi, Intermountain’s Intalere). This range of supply chain changes, often highly specific to a health system, creates some challenges for suppliers (e.g., potentially higher cost to serve), but creates opportunities as well (e.g., interest in new service offerings to support supply chain activities). While progressives continue to refine how their end-state supply chains will look, suppliers will need to remain nimble and adapt to the new roles they may need to play.

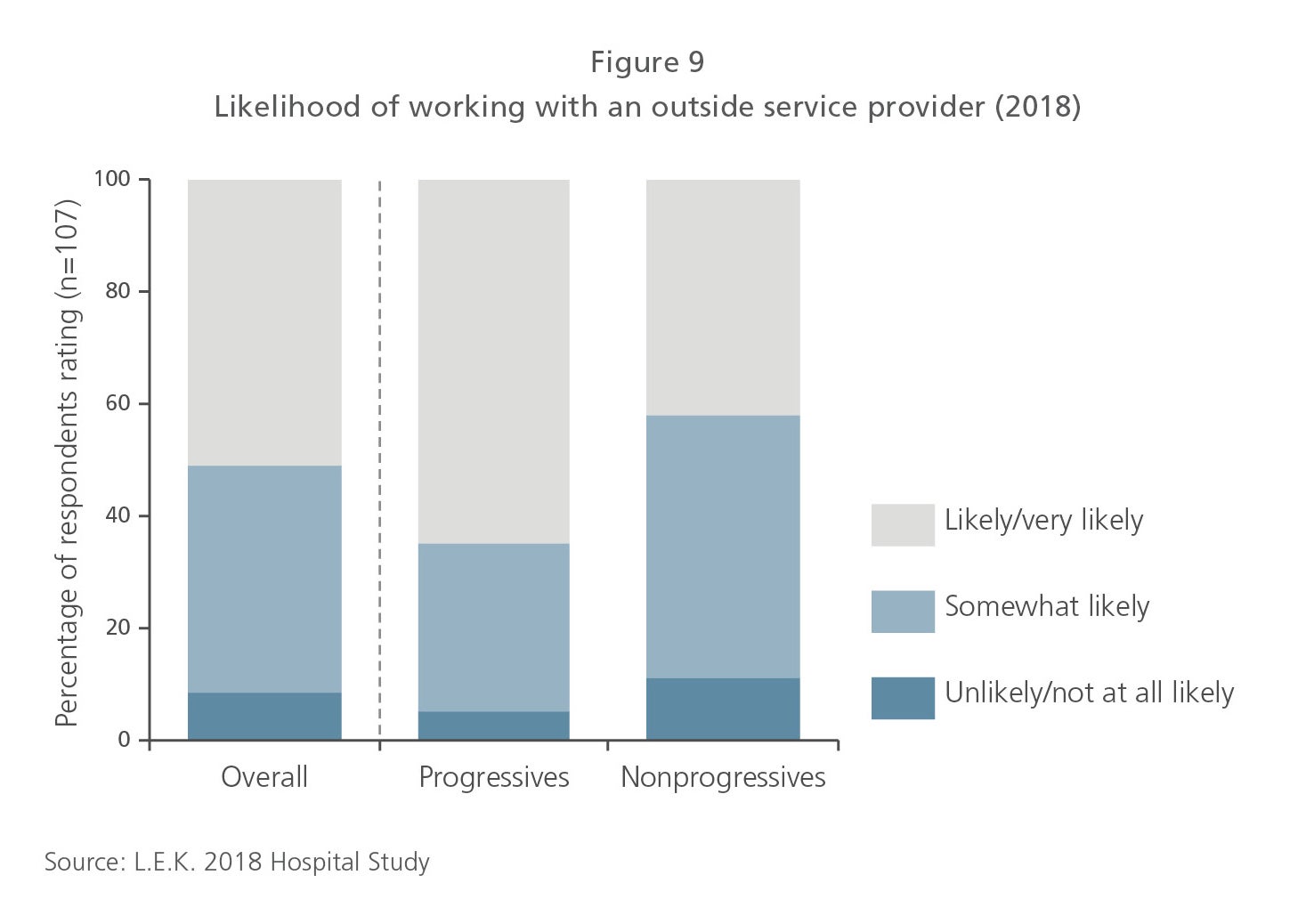

Finally, it is worth noting that progressive health systems generally exhibit a very different approach to supplier relationships than do other segments. Progressives are actively seeking outside partnerships as a way to gain expertise and expand their capabilities. They are increasingly open to working more closely with suppliers in general and are seeking deeper relationships with a narrower set of preferred partners in particular (see Figure 9). As a general rule of thumb, local traditionalists and scaled traditionalists tend to be more transactional in their supplier relationships, while progressives tend to be more partnership-oriented. A thorough understanding of these segments can help suppliers engage customers in the ways in which those customers want to be engaged and ensure that suppliers take advantage of opportunities to engage more closely with their customers.

The future for healthcare product and service suppliers

The evolution of the U.S. provider landscape is far from over. Suppliers have begun to change commercial engagement models and offerings in response, but they must continue to adapt or be left behind. Leading suppliers are tailoring provider segmentation to their business, benchmarking their performance with different segments, and adjusting their targeting, resourcing and service offerings to align with the priorities and needs of different customers. These suppliers are recognizing that alignment with thriving progressive health systems will be the difference between success and failure in the next decade.

01272020130155