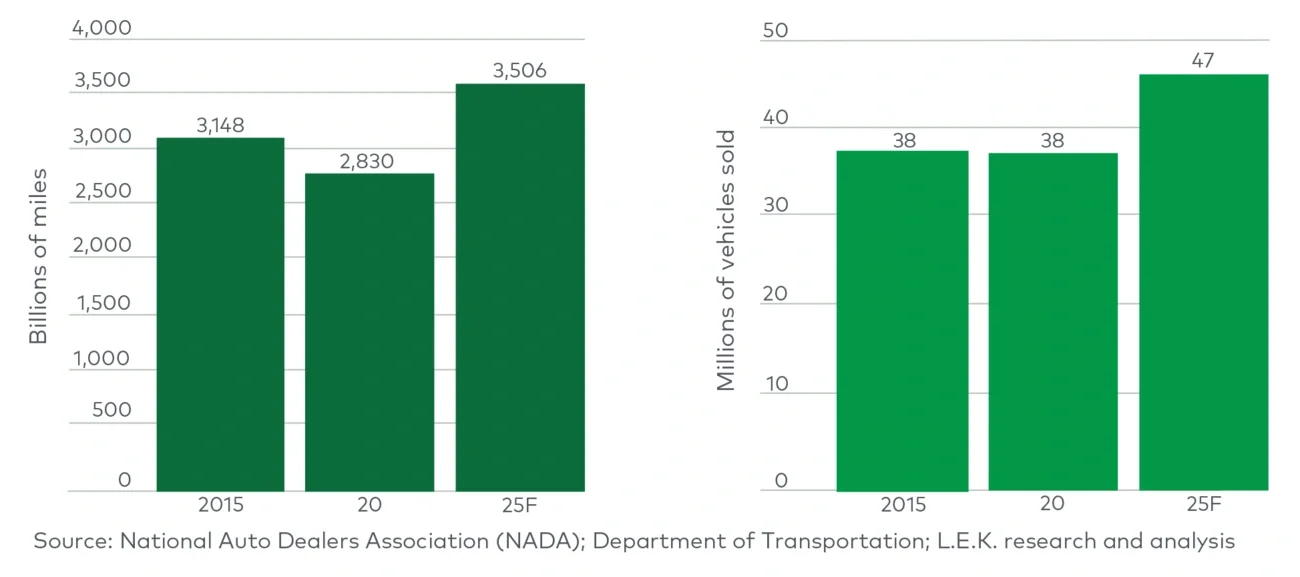

For operators and investors in auto service and repair, the tailwinds for the industry are clear. Following a mild slowdown in the first half of 2020 due to COVID-19, key underlying drivers of the sector have since recovered and are expected to continue growing robustly. The two most important contributors to this ongoing growth — increases in the number of annual miles driven and in the number of used car sales forecast to take place by 2025 — will lead to increased demand for service and repair (see Figure 1).

Executive Insights

Growth Opportunities in Auto Service and Repair: The Road Ahead

Growth Opportunities in Auto Service and Repair: The Road Ahead

February 23, 2022

Key takeaways

The outlook for auto service and repair is positive, powered by numerous tailwinds in combination with the sector’s historic insulation from economic turbulence.

The service length for vehicles on the road in the U.S. is increasing, and with it, consumers’ auto service and repair needs.

Transformational changes are coming to the market, driven by emerging technologies and step changes in consumer expectations, with consumers demonstrating a willingness to pay more and/or switch brands in exchange for a superior experience.

Truly disruptive innovation in the sector remains a long way off — providers are only scratching the surface, but there is an opportunity to lead the charge and drive defensible, sustainable differentiation as the automotive world evolves.

Figure 1

Annual miles driven in the US and US used car sales

Image

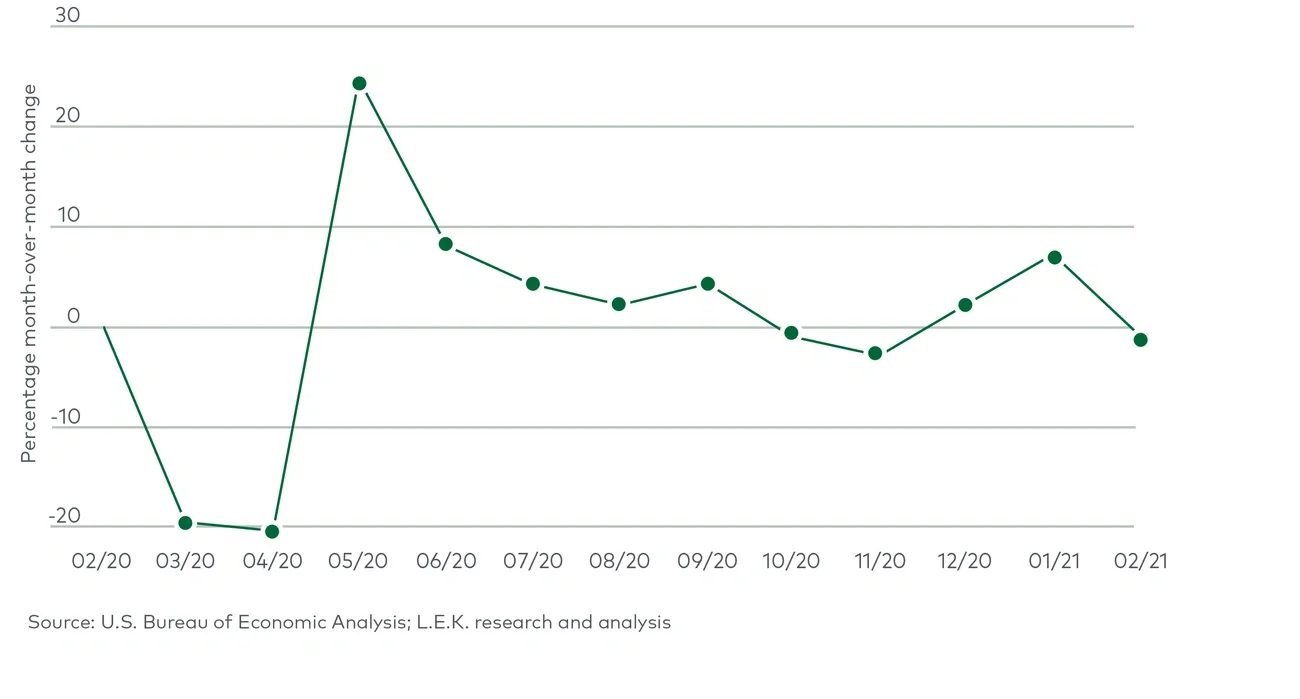

In many ways, COVID-19 demonstrated the relative resilience of automotive expenditures (see Figure 2). In fact, COVID-19 has actually accelerated underlying demand as the subsequent shift in consumers’ priorities toward light vehicle ownership is leading to a supply imbalance that is as great as it has ever been.

Figure 2

US monthly percentage change in consumer expenditure on automotive

Image

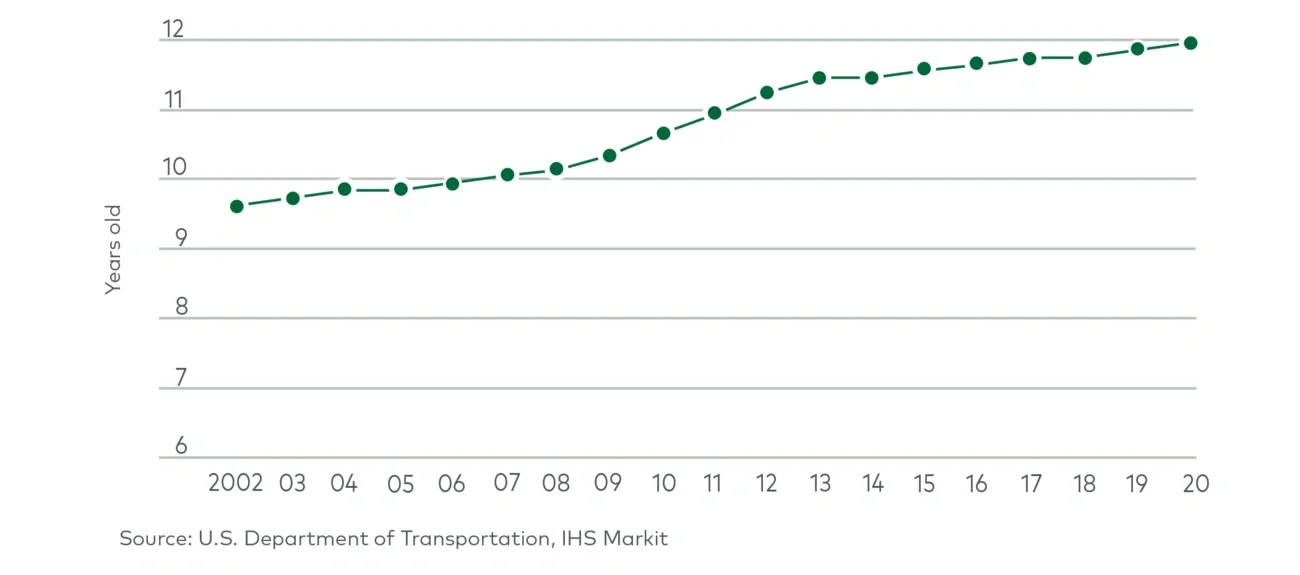

In parallel to these market developments, the service length for vehicles on U.S. roads is increasing, with the average age of vehicles in operation growing by more than 20% since 2002, from 9.6 years to 11.9 years. When combined with the growing size of the U.S. car parc, you have a recipe for continued growth in demand for preventive maintenance and repair, especially since many vehicles end up being on the road for 20 years or more (see Figure 3).

Figure 3

Average age of vehicles in the US car parc (2002-2020)

Image

Despite the favorable macro tailwinds for auto service and repair, however, the evolution of automobiles is also creating unprecedented challenges for providers going forward.

Technological shifts are beginning to occur. The growing penetration of battery electric vehicles (BEVs), rollouts of advanced driver-assistance systems (ADAS) and the increasing connectivity of vehicles are moving the market toward a transformative period for service and repair. The incorporation of greater technology is also expected to create significant expense in tools, systems and training. Meanwhile, OEMs are gaining the ability to “update” vehicles remotely and, in the process, to “lock out” independent providers through proprietary diagnostics, tools and software code.

These evolutions are prompting many questions in the industry about how the auto service and repair model will adapt, among them:

-

How soon will these technological changes have a meaningful impact on service and repair?

-

What will be the future role of independent auto service and repair?

-

What can differentiate and drive demand for independent auto service and repair providers, and how can they position themselves to win?

L.E.K. Consulting’s recent experience suggests that while technological shifts create challenges, they also provide an opportunity to bring truly disruptive innovation to the consumer experience. In parallel to changes in vehicles, changes are also taking place in the retail environment, and consumer expectations of the retail and service experience are on the rise. As digital retail environments for research, purchase and service become the norm, delivering on consumer expectations can help service providers develop an edge.

Disruptive forces are coming but will not result in immediate change

Several trends related to BEVs, ADAS and OEM control of service and repair will have a major impact in the long run.

Battery electric vehicles

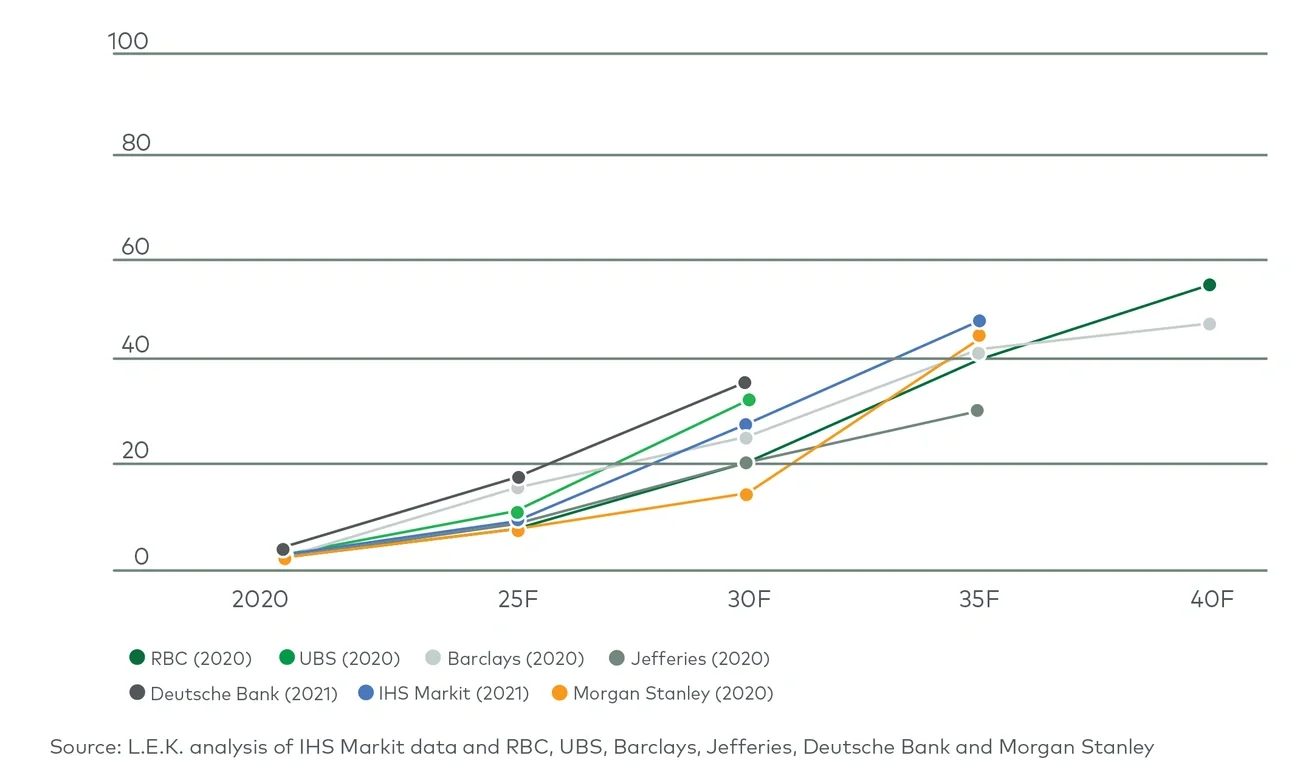

The pace of BEV sales is accelerating (see Figure 4), and the service and repair needs for these vehicles are quite different from those of internal combustion engine vehicles (ICEVs).

Figure 4

Forecast BEV penetration of US new light vehicle sales

Image

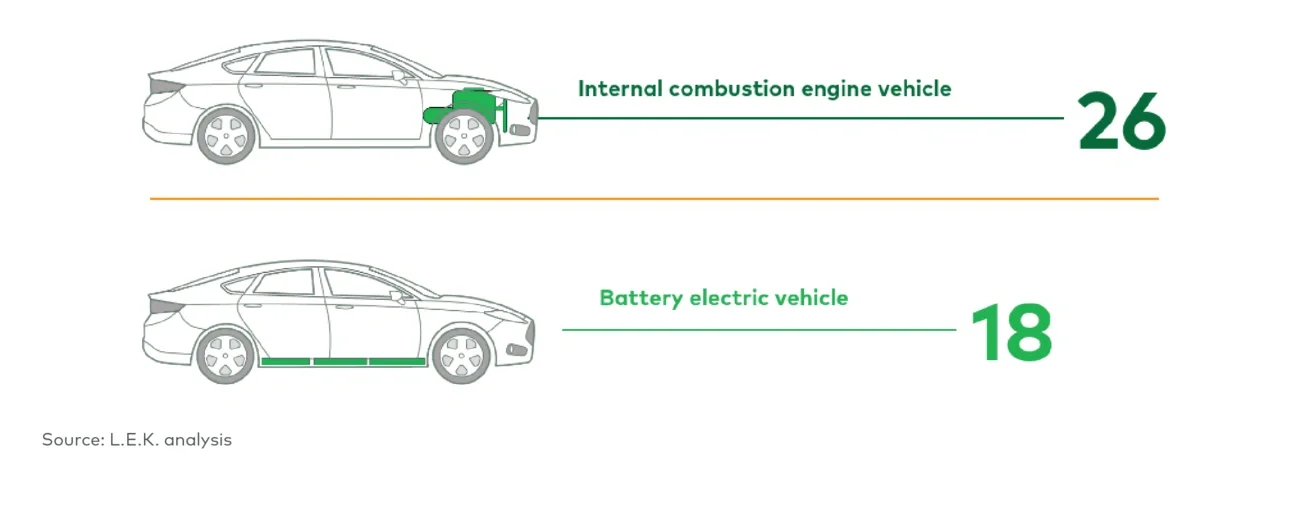

BEVs differ not only in their powertrain architecture, but in systems ranging from suspension to braking, thermal management, electricals and control units, each of which demands new skills and capabilities for service and repair. But perhaps more important, while BEVs will require maintenance, the magnitude of needs may be materially lower as they have less complexity and fewer moving parts that are likely to require service or repair; consumables like brakes and lubrication also experience significantly less wear. Based on average recommended service intervals, BEVs may require some 30% fewer maintenance visits, with lower levels of maintenance needed for each service (see Figure 5).

Figure 5

Average number of recommended service visits in the first 150,000 miles

Image

Nevertheless, L.E.K.’s recent work suggests that a material auto aftermarket will continue to persist as BEVs roll out. With respect to maintenance and repair, consumers indicate a similar willingness to consider aftermarket brands whether their vehicle is an ICEV or a BEV. In addition, while drivetrain maintenance and repair may be less extensive in BEVs (vs. ICEVs), case studies of real-world BEV use to date suggest that overall maintenance and repair costs may not be as significant. Perhaps more interesting, we have also found material subsegments of enthusiast communities to be open not only to adopting BEVs, but also to upgrading their BEVs in ways similar to how ICEVs are upgraded today.

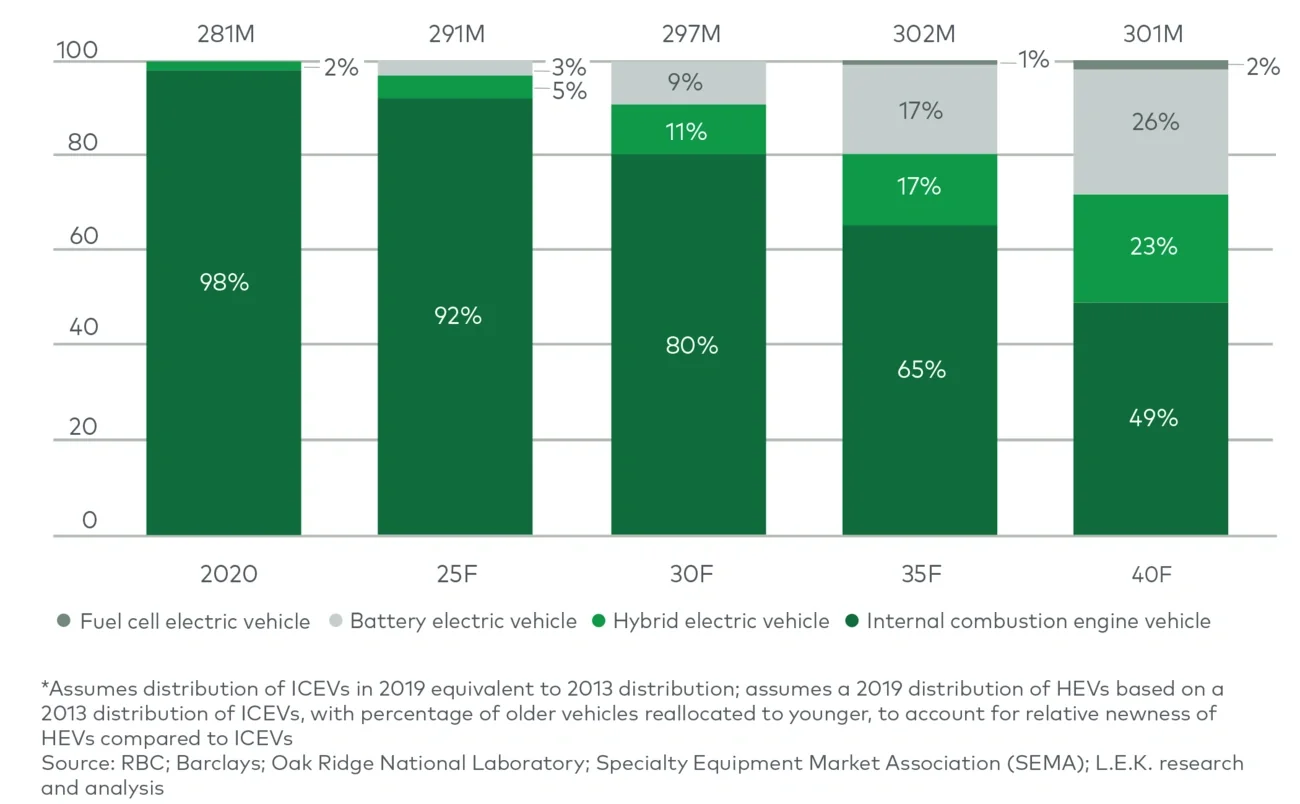

While BEVs are coming, the need for service and repair of ICEVs is likely to persist for many years. At current rates, it is expected to take up to approximately 20 years for BEVs to comprise a quarter of the vehicles in operation. Simply stated, the increasing length of time that vehicles are staying on the road means that it will take a while before new BEV sales start to penetrate the overall car parc (see Figure 6).

Figure 6

US vehicles in operation (VIO) by drivetrain type (2020-2040F)*

Image

Advanced driver-assistance systems

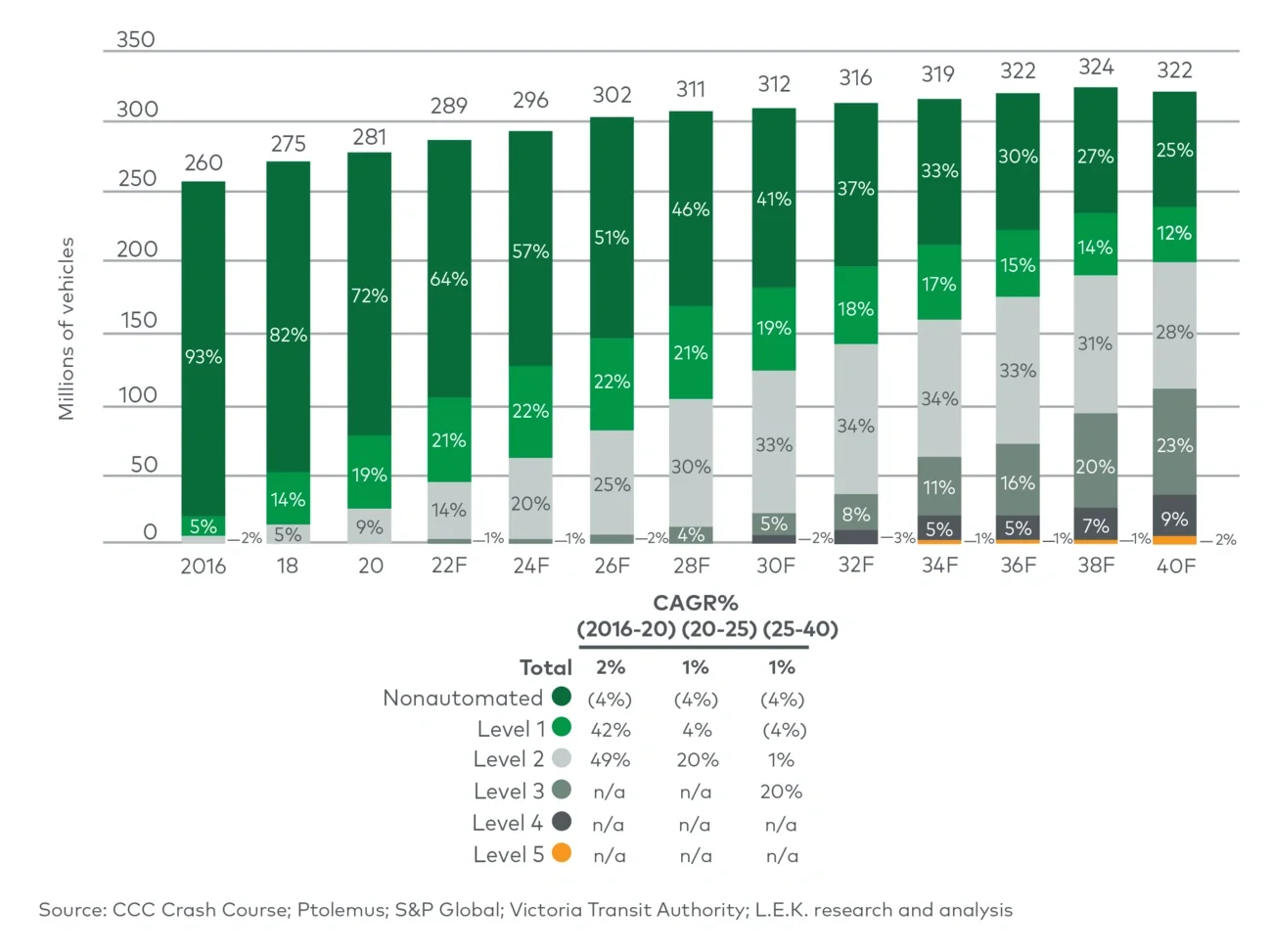

ADAS penetration in vehicles is similar to that of BEV penetration. True Level 5 autonomy, where cars can drive themselves anywhere, under any conditions, without any human supervision, is expected to change the nature of service and repair needs (given new, complex ADAS components) and simultaneously suppress demand for collision repair (given lower incident rates). While advancements are being made at rapid speed, true autonomy faces significant adoption, regulatory and infrastructure barriers. For now, Levels 2 and 3 autonomy represent less than 15% of the number of vehicles on the road today. True adoption of autonomous vehicles (AVs) — and the impact they will have on mobility more broadly — is not expected in the next 10 years (see Figure 7).

Figure 7

Automated vehicle penetration of US car parc by AV level (2016-2040F)

Image

OEM control of service and repair

As vehicles become increasingly more connected and controlled by software, a common question is how the role of the independent service and repair provider will persist. The increasing complexity of vehicles is raising the bar for providers, requiring more sophisticated technology and the integration of hardware and software that is costly for non-OEM providers to support (costs for diagnostic tools, training, certifications, etc.). If they want to play a role going forward, access to these systems will remain critical. There is also concern that independent providers may find a decreasing number of service and repair areas where they are able to participate in the face of remote updates and/or inaccessible diagnostic information or software. From a regulatory point of view, the recent passing of right-to-repair laws in Massachusetts suggests a protected path forward, but strategic challenges remain for market participants to navigate.

A superior consumer experience can be a key differentiator

Given the challenges that auto service and repair providers will need to navigate in the years ahead, an important consideration is what they can do now to differentiate and position themselves to win in both an ICEV present and a BEV/ADAS future. L.E.K.’s consumer research suggests that one solution is to offer a superior consumer experience.

Consumer expectations around interactions with service providers have risen significantly as a result of how offerings from winning providers in retail, foodservice, media/entertainment, fitness and healthcare have evolved to address pain points. Younger consumers in particular are coming to expect seamless omnichannel service, on-demand delivery, exceptional convenience and near bespoke customization and flexibility.

Generally speaking, the experience offered in auto service and repair has remained stagnant relative to other consumer industries. Examples of pain points that could be addressed in auto service and repair include:

-

Digital access: Integrated mobile and digital tools for research, diagnosis, scheduling, purchase and progress status

-

Rapid and/or scheduled timing: Opportunities for express and/or prioritized opt-ins; more precise timing expectations paired with the optimization of workflows and queues

-

Location convenience: At-home, mobile and remote services

-

Bespoke service: Concierge-level service for all aspects of vehicle ownership, including financing and insurance, detailing, and service and repair

-

One-stop convenience: Holistic capabilities across all potential needs instead of just for specialized offerings

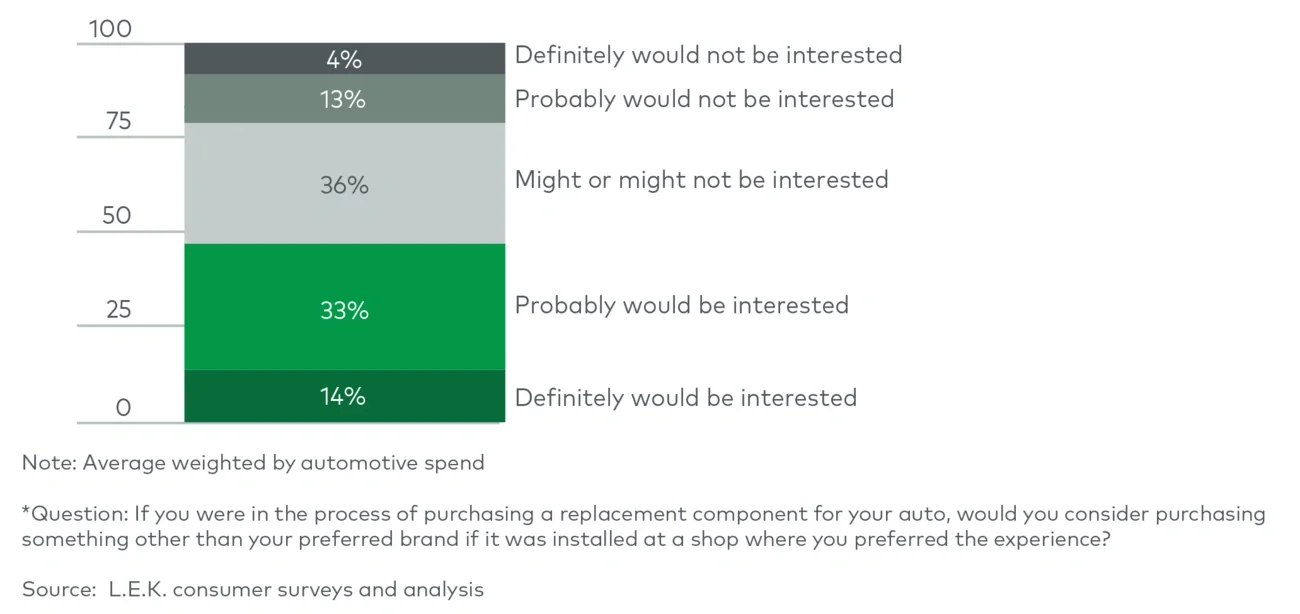

Importantly, the work L.E.K. has done in the automotive aftermarket space has found that consumers have a higher willingness to pay for, and a willingness to switch preferred providers for, a superior experience. Nearly 50% of consumers indicated an interest in switching away from preferred brands for a superior experience (see Figure 8). Notably, those willing to switch were willing to spend up to 25% more for that superior experience.

Figure 8

Impact of a superior shopping experience on choice of auto part brand

Image

Some early examples of companies attempting to deliver a unique consumer experience in auto include:

-

Digital access: Digitally native marketplaces such as Carvana and Vroom; omnichannel-oriented dealerships such as CarMax; digital aftermarket retailers such as Tire Rack

-

Rapid and/or scheduled timing: Dealership management software that may integrate one or more functions between shop workflow, diagnostics and consumer outreach via SMS and/or email

-

Location convenience: Safelite mobile glass repair; Tire Rack at home/work installation; mobile mechanic services such as Your Mechanic, Wrench and JET Mobile Service

-

Bespoke service: Specialty service providers such as Auto Concierge and Autotopia serve the high-end market, but few providers have a mass offering

Shifting dynamics present an unprecedented opportunity

Macro trends in light vehicles clearly point to tailwinds for auto service and repair, but also point to the prospect of increasing competitive pressures among providers. While there is still a long runway for these dynamics to play out, there are near-term implications for operators and investors alike.

For operators to remain in the pole position and be one of the winners as the industry transitions, it is critical to invest in the consumer experience. Based on our research, there is a compelling case for consumer experience to be a pillar in the future, but currently it remains an untapped opportunity where operators can differentiate.

For investors, there remains not only a material runway to support the existing ICEV car parc, but also certainty that the opportunity to service emerging forms of mobility will remain significant. To that end, there are compelling opportunities for service providers and enablers that can assist in the transition while delivering a superior experience.

Related insights

You might also be interested in these insights.

English