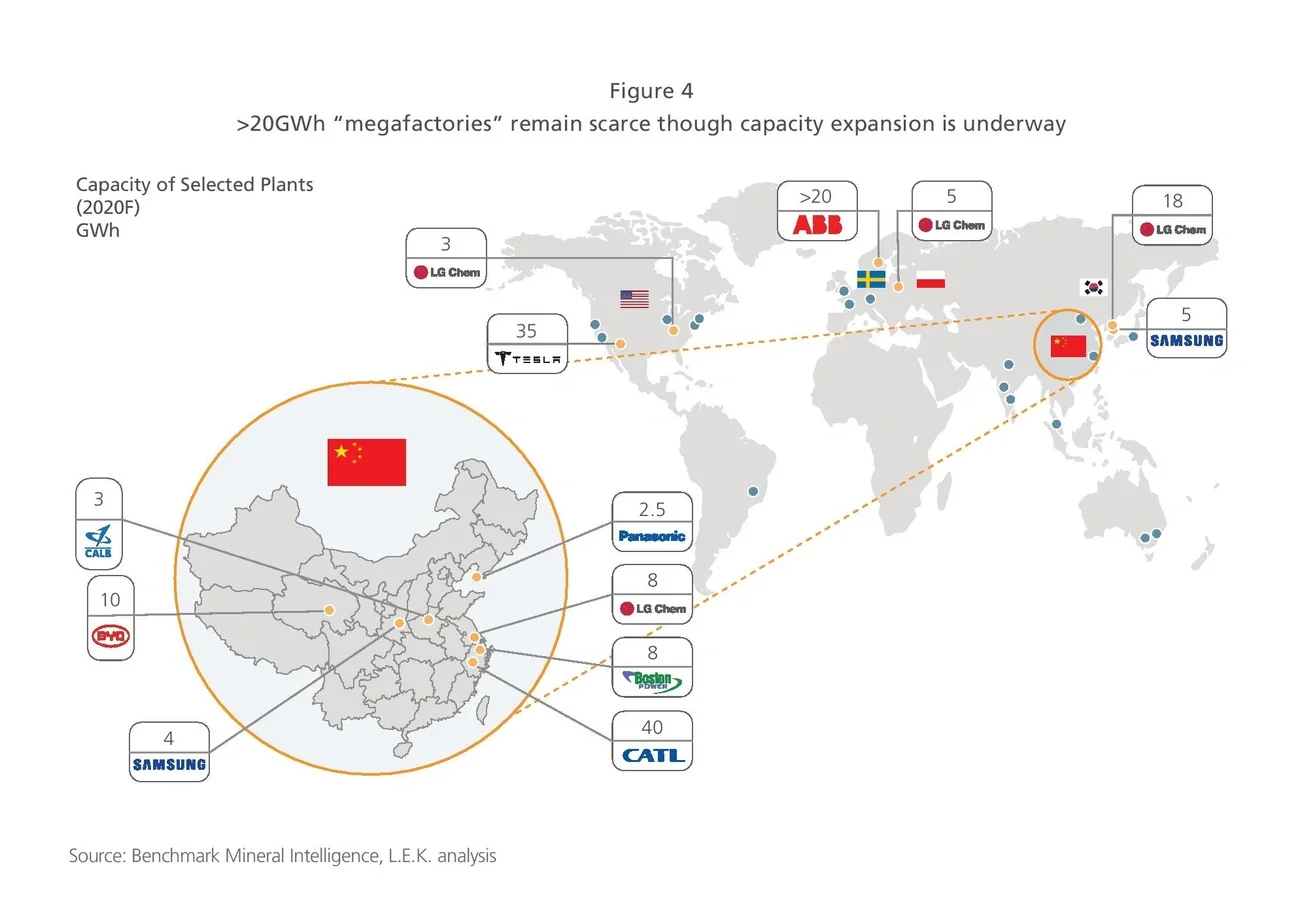

Capacity expansion results in a reduction in manufacturing costs. Tesla claims that its newly built megafactory will lead to a 30% drop in battery cost. CATL achieved a 15% decrease in battery cost in the past two years through technology upgrades and capacity expansion.

Rapid expansion of capacity will bring about financial risks. Therefore, strategic partnerships with downstream OEMs are vital to risk reduction. The $5 billion joint venture between Panasonic and Tesla is the most well-known example of how EV battery manufacturers cooperate with OEMs to deal with competition and risks. Similarly in China, SAIC and DF Motor invested in CATL, and BYD announced cooperation with Guoxuan High-Tech. These are all considered to be forward-looking strategies.

Moving up the value chain: Control key technologies and resources through vertical integration

EV battery manufacturers (and some EV manufacturers) consider vertical integration as key to lowering costs, extracting more value through synergies both upstream and downstream, and avoiding commodity price/supply fluctuations.

Electrode materials

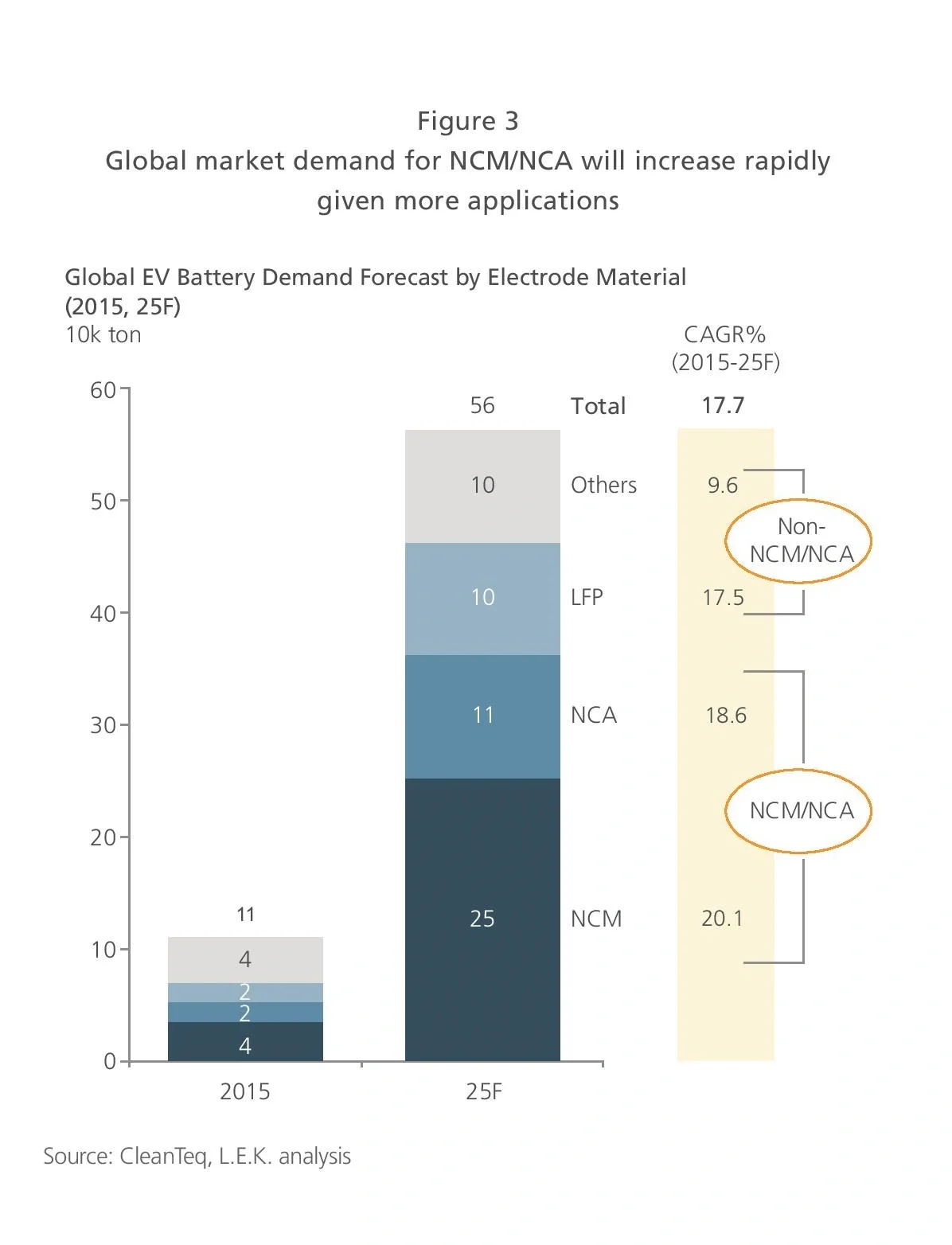

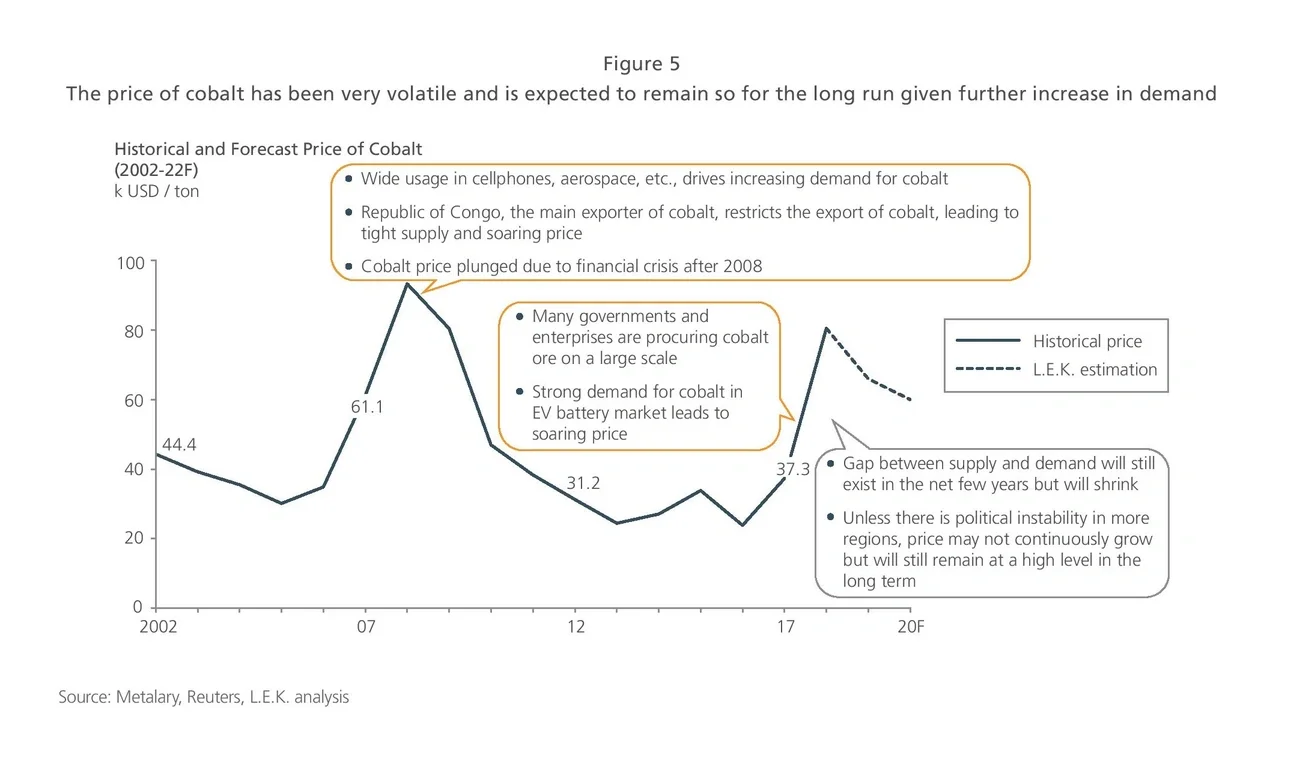

Given the growth in battery sales, demand for raw materials will increase rapidly, especially for nonferrous metals such as lithium, nickel and cobalt. Steady cobalt and nickel supplies are of critical importance.

- Cobalt: Further promotion of NCM/NCA batteries will drive demand for cobalt, pushing up its price

- Nickel: The trend toward “high nickel” will drive increasing demand for nickel sulfate; however, domestic pressure about environmental protection concerns may limit the supply capacity of nickel sulfate

- Lithium: The demand for lithium carbonate is rapidly increasing, but capacity is lagging, leading to a short-run gap between supply and demand

Lithium battery manufacturers can invest in the upstream and strengthen control of raw material supply. With the increase in cobalt prices, competition between tech companies and EV battery manufacturers/OEMs for cobalt resources has intensified. Apple is negotiating on the long-term purchase of metallic cobalt from mining companies, seeking five-year or even longer stable contracts. Tesla and BMW have announced negotiations with mining companies to ensure raw material supply. In China, CATL and BYD have strengthened their supply chain and control of upstream battery materials in 2017.

Further promotion of NCM/NCA batteries will drive demand for raw materials even while new capacity is limited in the short run. The market is concerned that prices of raw materials will soar over the next three to five years. However, with increases in capacity or emergence of substitute materials, we project that pricing will become stable within two to three years.

Take the case of cobalt for analysis. Increase in capacity of existing projects and the launch of new cobalt mine projects (there are approximately 400 active cobalt mine projects in the world) will gradually increase overall capacity. Hence, we project that the price of cobalt will stabilize after 2019 unless affected by special factors (such as political instability in Republic of Congo, the main supplier of cobalt).