Most industrial manufacturers want more aftermarket sales. Why wouldn’t they? The aftermarket is a source of highly profitable recurring revenue. It also strengthens relationships with end customers, and — because the aftermarket attracts new customers as well — it is a way to capture incremental market share.

We’ve also heard from many end customers who say they prefer buying aftermarket parts from the original equipment manufacturer (OEM) or approved original equipment suppliers. This feedback has been fairly consistent across industrial end markets, indicating manufacturers have a significant opportunity in the aftermarket.

So why is this opportunity so challenging to unlock?

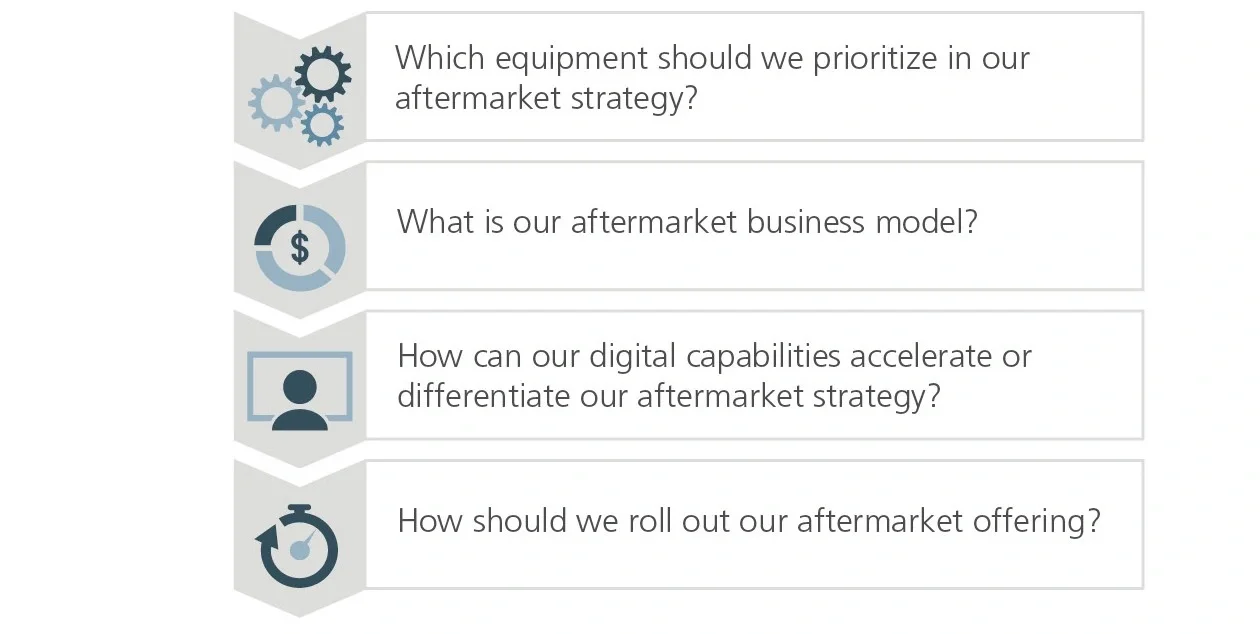

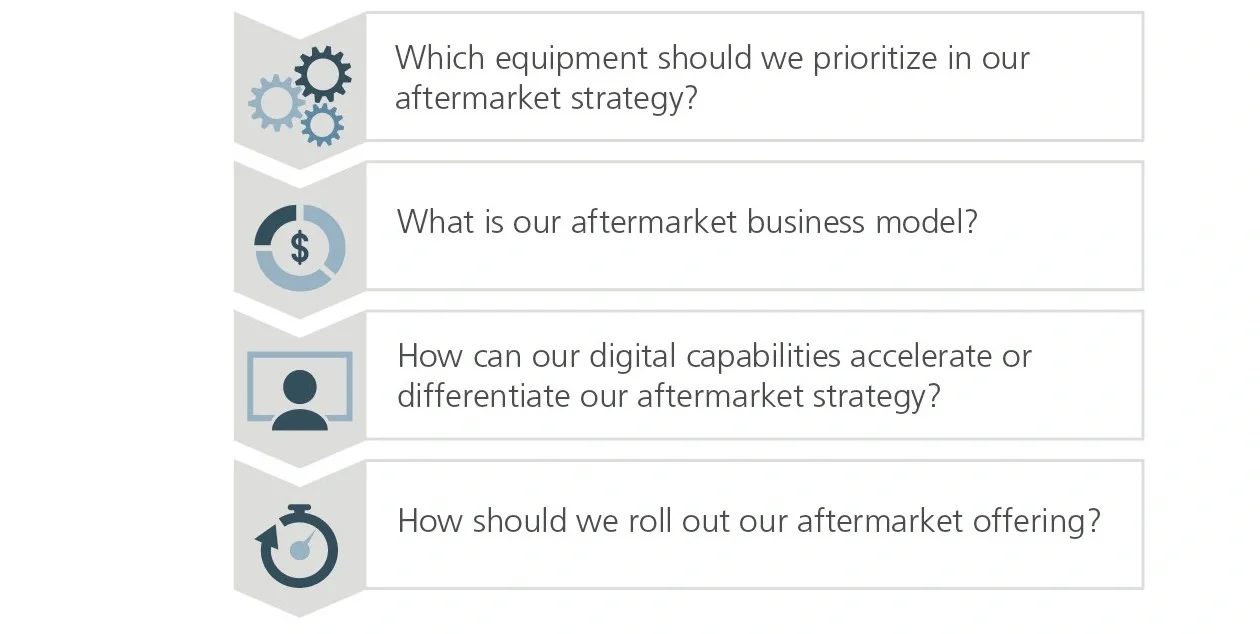

At L.E.K. Consulting, we’ve developed a framework for putting an aftermarket strategy together (see Figure 1). It’s based on four questions aimed at helping manufacturers unlock the financial and strategic value of aftermarket sales while minimizing potential disruptions to the core business. In future Executive Insights, we’ll explore each of those questions in greater detail. For now, let’s take a brief look at what they’re all about.