Key takeaways

-

With global revenue of more than $30 billion, healthcare packaging is expected to grow at a steady clip of 4% to 6% annually for the near term.

-

However, while underlying market fundamentals are attractive, winning in the healthcare packaging market is not without its hurdles.

-

Regardless of whether investors are already active in the global healthcare packaging space or are exploring the area, understanding market segmentation is step one.

-

Six major themes are critical to winning in healthcare packaging: end-market innovation, sales cycle length, customer stickiness, healthcare capability requirements and customer concentration/continued consolidation.

For both corporates and private investors looking to enter a lucrative market with long-term potential, healthcare packaging holds significant promise. With global revenue of more than $30 billion, healthcare packaging is expected to grow at a steady clip of 4% to 6% annually for the near term. Furthermore, it has proven highly resilient during economic downturns, largely due to the critical nature of the markets it serves — both pharmaceuticals and medical devices. Healthcare packaging offers investors an opportunity to benefit from both the high growth of its underlying sectors and the low-beta aspect of packaging. Consequently, recent transactions have generated high levels of investor interest.

While underlying market fundamentals are attractive, winning in the healthcare packaging market is not without its hurdles. It requires a detailed understanding of end-customer segmentation, as well as an understanding of how packaging manufacturers — or converters — can add value based on the needs of attractive customer segments.

Healthcare packaging has five key market segments:

- Prescription pharmaceuticals

- Over-the-counter pharmaceuticals

- Medical device original equipment manufacturers (OEMs)

- Drug delivery device manufacturers

- Diagnostic device manufacturers

With a few exceptions, there is relatively limited end-customer overlap across these segments, and the unique nature of customer needs, including packaging format, design support and commercial sales expertise, often lead converters to specialize in one or two segments, particularly if they are providing more complex and higher-value packaging solutions.

Regardless of whether investors are already active in the global healthcare packaging space, are looking to expand into the space from an adjacent category or are financial investors exploring the area, understanding market segmentation is step one. Beyond this there are six major themes that will impact the return investors can generate, their timeline to returns and the level of investment required. Understanding and navigating these themes is critical to winning in healthcare packaging.

Theme No. 1 — End-market innovation

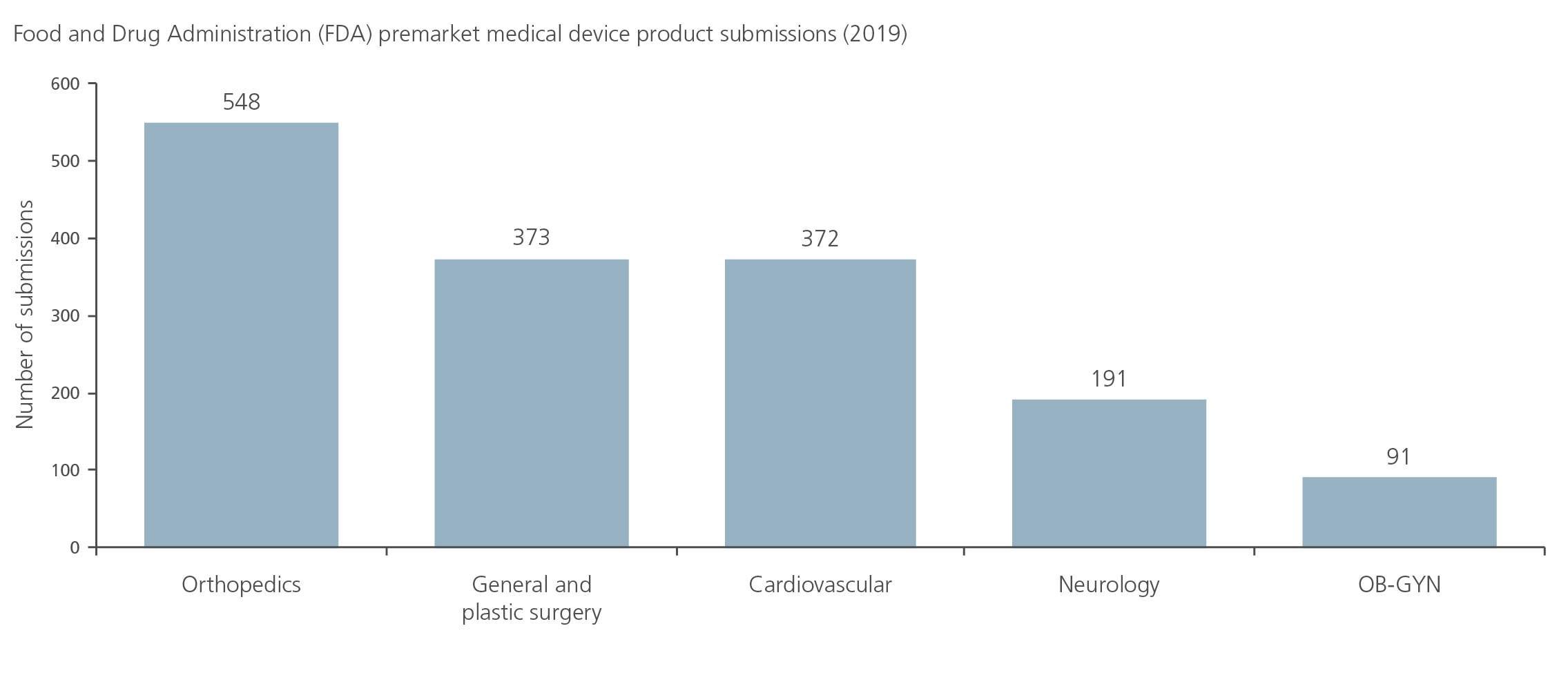

End-market innovation is the primary source of new project opportunities for converters. Innovation activity differs widely across healthcare segments and subsegments. For example, in the medical device segment, therapeutic areas such as orthopedics and cardiology are experiencing higher levels of product innovation across procedure types (see Figure 1). Specifically, minimally invasive procedures are experiencing greater innovation than traditional surgical procedures.

In diagnostics, point-of-care-based tests have captured market share from traditional lab-based tests, and within point-of-care, certain subsegments like fecal testing are growing faster than other parts of the market. Another promising area: Healthcare is evolving to make adherence easier for patients, resulting in opportunities for delivery mechanisms and packaging. In drug delivery, this has led to innovations like auto-injectors, and in pharma, it has created an opportunity for blow-fill-seal ampules for liquid oral over-the-counter products.

From the converter perspective, understanding where end-market innovation within therapeutic areas is coming from today — and where it is headed — can help shape commercial strategies and lead to above-market revenue growth. For investors, knowing which drugs or devices are likely to be winners or losers is central to choosing an attractive packaging target. By focusing on the end customer and end market, and by ensuring that target converters are serving those that are the most innovative, investors can increase their chances of realizing outsized returns.

Theme No. 2 — Sales cycle length

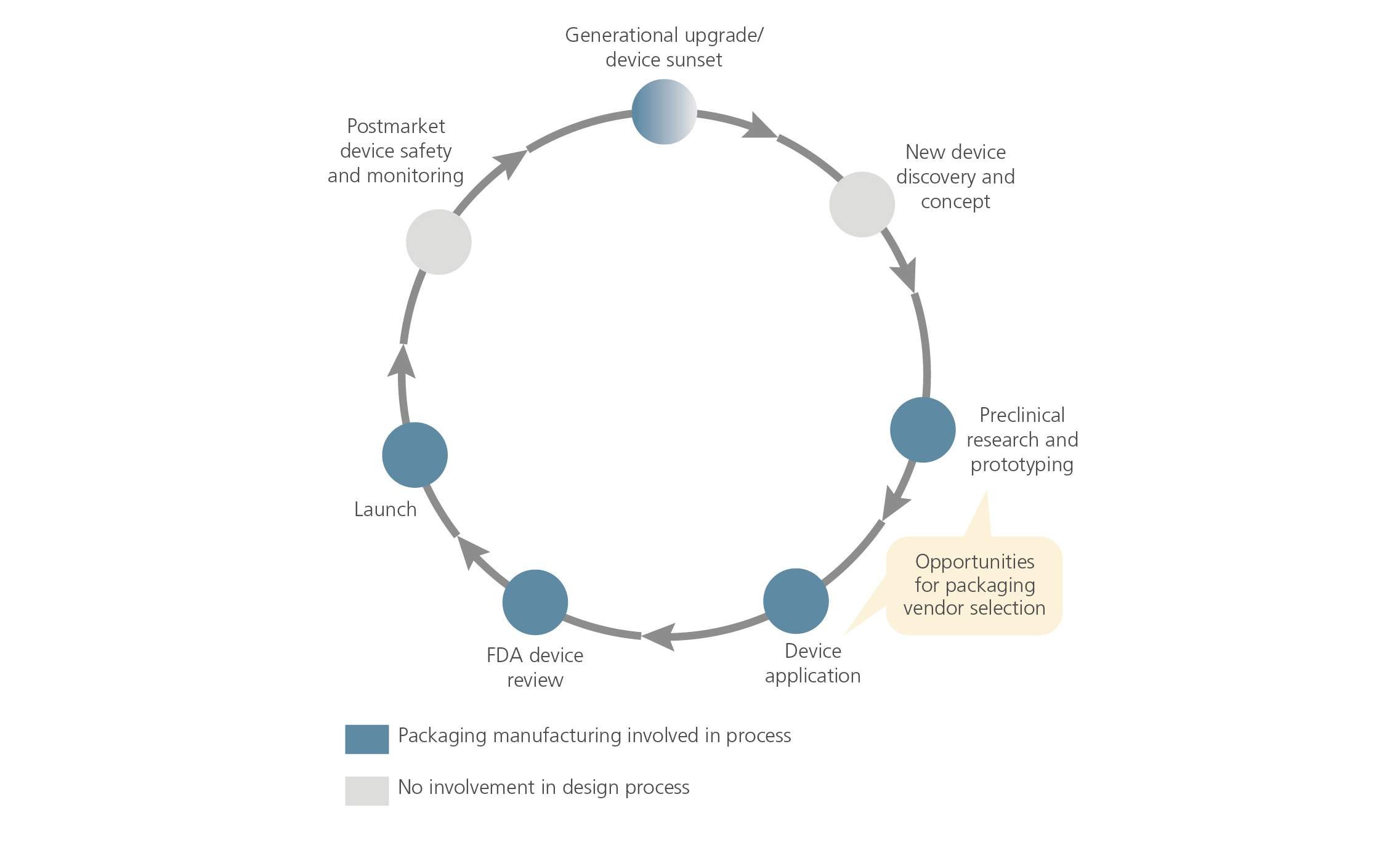

Healthcare packaging has a unique sales cycle that is closely tied to that of pharma and medtech companies’ products. Pharma companies and medical device OEMs typically make packaging decisions early in the product or drug development cycle — usually when a device moves into the prototyping phase or prior to being submitted to the FDA for approval (see Figure 2). Consequently, the elapsed time from winning a new packaging project to realizing revenue from it can be quite long, ranging from just under a year for simpler Class II medical devices to as long as three to five years for novel pharmaceutical products.

For investors, this dynamic can lead to deferred returns and delayed cash flows, but once products are in the market, they represent highly steady and long-term revenue opportunities. Nevertheless, there is sales cycle variation across categories. For example, certain medical devices in a mature category might have shorter development times and approval periods. Or one category might be succeeding a prior generation, making replacement of the legacy product relatively straightforward. Although the sales cycle may be shorter in these more mature categories, margins may be lower and it may be harder to differentiate products. Categories characterized by more innovation generally have longer payback horizons, but greater margin and revenue opportunities. These examples illustrate the risk-reward trade-offs that investors need to consider in evaluating target assets.

While long product life cycles may require patience on the part of investors, it is difficult to fully appreciate the revenue-generating potential of a target without a close examination of its pipeline. There is a world of difference between an asset with a five-year lead from signed contract to production for a particular project but an otherwise empty pipeline, and an asset with a similar contract but a full pipeline of other projects coming online in the interim. Building a successful business in healthcare packaging requires a robust pipeline — a factor that also impacts the next theme we will discuss, customer stickiness.

Theme No. 3 — Customer stickiness

Despite the lengthy payback period, healthcare packaging contracts can yield reliable revenue for five to 10 years or more, depending on the remaining patent life of the drug or device. This is because across segments, end customers generally avoid switching packaging providers, so revenue streams are essentially locked in.

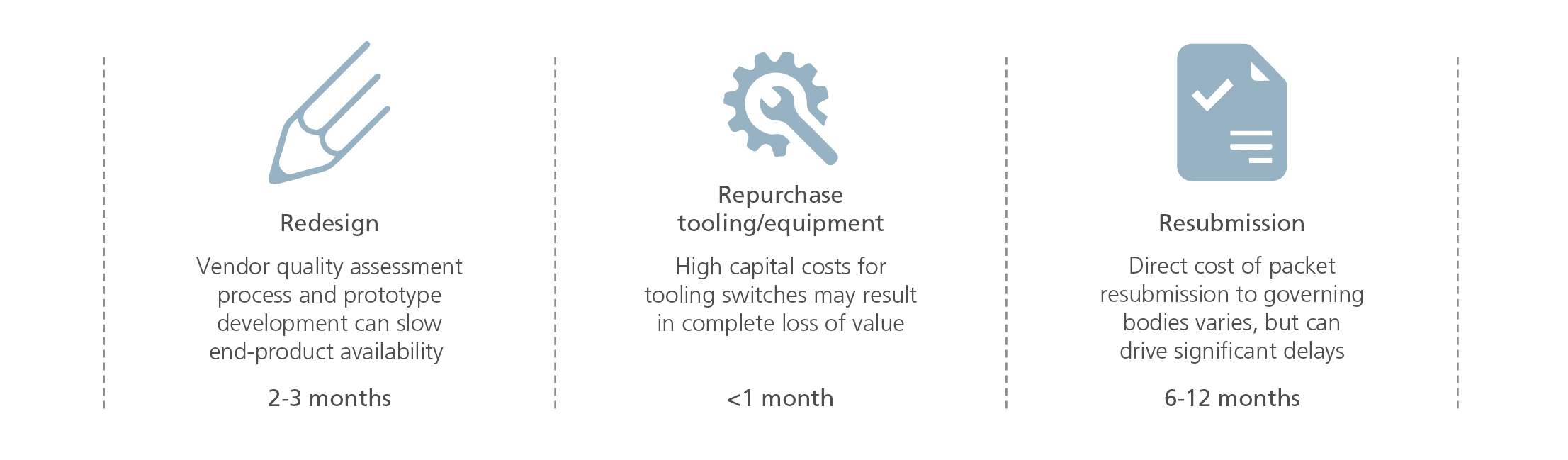

There are two primary reasons for this customer stickiness. First, packaging for pharmaceutical products and many devices requires FDA approval, meaning any change in provider will need to be submitted to the agency for what is usually a lengthy review (see Figure 3). Both the application process and the resulting delay lead to very high switching costs.

Second, there are a number of indirect costs associated with changing packaging suppliers, including supply disruptions and performance issues while a new converter is getting up to speed. Because these costs can be quite high, OEMs and pharmaceutical manufacturers are generally reluctant to switch, except in cases of significant underperformance — for example, packaging failures or extreme delivery delays.

Customer stickiness is far more characteristic of healthcare packaging than it is of packaging in other end markets, where contracts are often put out to bid more frequently. This is certainly attractive for investors in this space, but it also emphasizes the importance of examining the pipeline of any target company. The extent of customer stickiness — and therefore the relative security of revenue streams — depends on both the end-customer market and the details of customer contracts.

The average life of the contracts in a converter’s portfolio can be an indicator of its potential. If the target company has 10 projects underway and all are reaching the end of 10-year contracts, then the stickiness benefit of these contracts has largely played out. On the other hand, if all 10 projects are in their first year, then the commercial outlook for that business is far more positive. Understanding where projects are in the life cycle of the product is an important consideration when thinking about an organic growth opportunity.

Theme No. 4 — Packaging innovation

Due to high switching costs and customer stickiness, packaging manufacturers have limited ability to generate growth by taking over projects when there is an incumbent. They therefore need to focus business development efforts on winning new projects — and winning new projects often hinges on a converter’s ability to offer new packaging solutions to end customers. Today, packaging-specific innovations are enabling manufacturers to meet a broader cross-section of end-customer applications and realize higher margins. There are numerous examples of this type of innovation:

- Thermoplastic polyurethane (TPU) is an abrasion-resistant material that is softer than traditional rigid plastic packaging. It is used in high-value packaging for products like replacement prostheses that need to be unboxed in the operating room. Because TPU protects the device better than traditional packaging does, it can command a price that is up to three times higher.

- Tyvek, a DuPont product most commonly used in building products, is a breathable, durable, tear-resistant medical-grade material that serves as a sterile barrier to protect drugs and medical devices. Given its properties, it is often more easily sterilized than other solutions. Additionally, DuPont has granted a limited number of Tyvek licenses (10 in the U.S.), providing a competitive advantage to converters holding these licenses.

- Blow-fill-seal technology, which is a type of aseptic manufacturing, results in a drug delivery vessel that is formed, filled and sealed in one continuous, automated system, thereby reducing human involvement and the corresponding risk of contamination. This technology is now applicable to injectables like vaccines and biologics.

In evaluating potential healthcare packaging opportunities, corporate and private equity investors should seek to understand their relative degree of packaging innovation, including access to differentiated technology or licenses.

Theme No. 5 — Healthcare capability requirements

When healthcare end customers are considering packaging providers, they are often looking for converters that are focused solely on healthcare clients — or at least focused on healthcare products within the facility where a new healthcare packaging job would be converted. There are several reasons for this. First, healthcare packaging — particularly packaging for higher-value end products like implantables — must be manufactured in clean rooms that have been certified by the International Organization for Standardization and overseen by individuals with healthcare-specific manufacturing, engineering and regulatory experience. If a packaging provider does manufacture packaging for clients in other industries, OEMs expect packaging production for their products to be located in healthcare-focused facilities.

Due to the importance of the converter’s physical plant, end customers almost always tour facilities as part of the contract-awarding process. Investors would do well to conduct similar tours because the existence of dedicated facilities increases an asset’s attractiveness to end customers.

Finally, winning new projects requires healthcare-specific commercial capabilities. End customers are often looking for packaging suppliers with experience in their primary segment (e.g., medical devices) and focus subsegment (e.g., orthopedics), as well as those with a working knowledge of their end products (e.g., orthopedic implantables). For investors, these capabilities can serve to further de-risk investments by creating high barriers to entry among players outside of healthcare.

Gaining traction in the healthcare packaging space is still possible without healthcare-specific capabilities, but companies need to be proactive about building or acquiring them — and the timeline for realizing returns may be longer.

Theme No. 6 — Customer concentration and continued consolidation

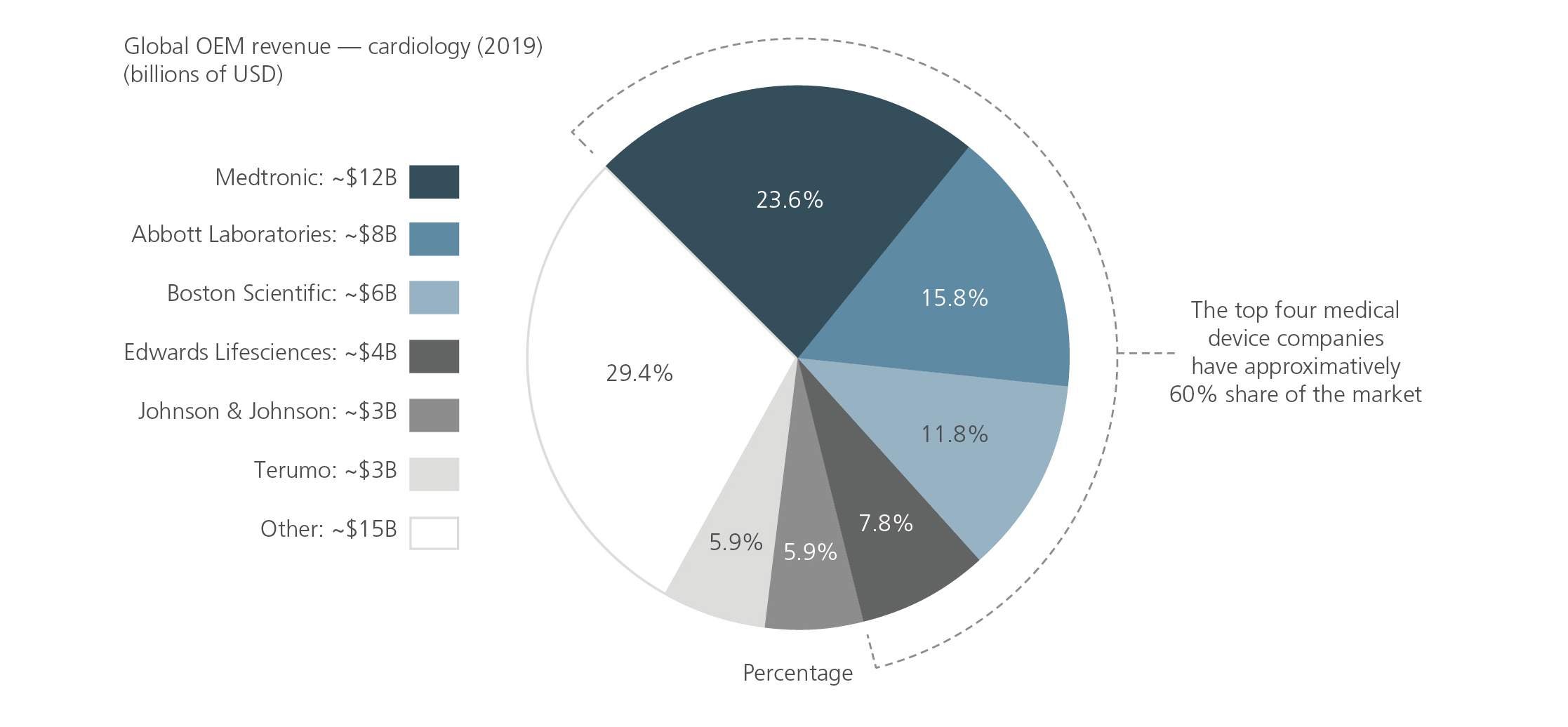

Compared with other industries that converters typically serve, healthcare is fairly concentrated across segments. On a segment-specific basis, the market can be quite consolidated: For instance, in the high-value cardiology segment, the top four OEMs represent some 60% of the market (see Figure 4). Many of these large OEMs have a global footprint, and as a result, larger healthcare packaging converters that can meet global OEM needs often have a competitive advantage when bidding on new projects.

Despite industry concentration, consolidation is ongoing as larger OEMs acquire smaller players. As a result of their acquisitions, these OEMs tend to have a fragmented set of packaging suppliers. While switching challenges preclude them from eliminating converters, OEMs are rationalizing their supply bases for new projects, often leveraging a small subset of one to three strategic providers that are distinguished by their scale and ability to provide design support.

Nevertheless, opportunities remain for smaller converters. These companies are often best positioned to serve smaller OEMs looking for higher-touch solutions or those that lack sufficient scale and resources to be served by larger packaging providers. From an investor perspective, converters that serve — or have the potential to serve — these smaller OEMs can be especially attractive. First, these end customers tend to be the most innovative, so winning projects with them gives converters high visibility within the industry. Second, given the consolidation in the healthcare sector, small, innovative OEMs are attractive acquisition targets for larger players. If a converter’s end customer is acquired, this gives the converter an opportunity to be pulled into the supplier base of the larger OEM and to win business from it over the long term.

Understanding the overall industry landscape will alert investors to the most promising assets in the healthcare packaging space. For buyers already in the industry, this is an important lens for identifying converters that may have more traction in winning new projects that are innovative but too small to serve larger OEMs, making them attractive targets for a bolt-on strategy.

Securing a path to success

To both corporates and private equity firms, the healthcare packaging space is highly attractive, providing investors with access to a large and stable market that is well positioned to benefit from long-term trends. Successfully participating in this market requires an understanding of not only the players but the end-customer segments they serve. Access to deep expertise in forecasting drugs/devices, drug/device volumes and, consequently, packaging formats can increase the likelihood that investments in packaging are successful. Furthermore, investors need to be willing to defer returns, given the high correlation between lengthy drug and device development cycles and new project opportunities. By deferring these returns, however, investors can gain access to highly sticky and long-term revenue streams, as well as a highly attractive and stable platform for growth.

01032023160137